Recommended Weekend Reads

China’s Determined Latin America Strategy, How Mexico Is Winning The Tariff Wars, How Will China Rightsize Its Economy?, and How The Ukraine War is Fraying Russia’s Society

January 2 - 4, 2026

Americas

China’s Third Policy Paper on Latin America and the Caribbean: Expanding Influence and Ambitions Ryan Berg/Center for Strategic and International Studies

China’s Foreign Ministry recently released its third policy paper on Latin America and the Caribbean (LAC). The paper is wide-ranging, encompassing topics from diplomacy to security cooperation and cultural exchange. The document reflects China’s growing engagement with the Western Hemisphere and its increasingly comprehensive approach.

Erasing the Verdict: The Ongoing Shock of Trump’s Cocaine Kingpin Pardon Bloomberg/Businessweek

Bloomberg takes a deep dive into President Trump’s recent surprise pardon of former Honduran President Juan Orlando Hernández, arguing that it “toppled the capstone of one of the most ambitious narcotics investigations in the history of the Department of Justice.”

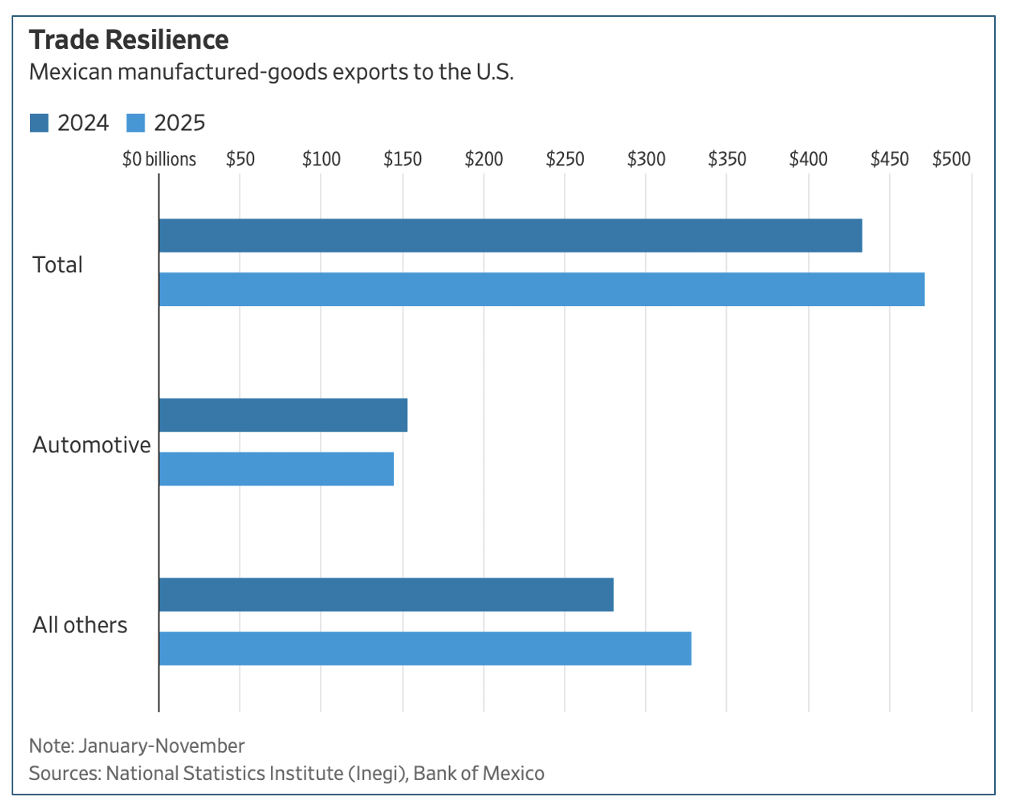

The Unexpected Winner of Rising American Tariffs Is Mexico Wall Street Journal

When President Trump began raising tariffs earlier this year, government officials and economists feared Mexico’s export-led economy would take a devastating hit. Instead, Mexican exports to the U.S. have grown. Because Mexico’s ultimate tariff rate ended up lower than for most other countries, the disparity has helped Mexican exports fill some of the gap left by Chinese products subject to higher levies. Even with steep tariffs on autos, steel, and aluminum bound for America, Mexican manufacturing exports to the U.S. rose almost 9% from January to November, compared with the first 11 months of 2024, according to Mexican government data. Auto-industry exports to the U.S. fell close to 6% during the period, but exports of other manufactured goods surged 17%. Trade in goods between the U.S. and Mexico is on track to reach a record of nearly $900 billion this year.

LatAm Outlook 2026 Canning House

The Canning House (the UK’s leading Latin American-focused think tank) has just published its 2026 LatAm Outlook. It is done in conjunction with Bloomberg, the International Institute for Strategic Studies, SEI, Ipsos, Control Risks, and the UK’s Department for Business & Trade and was first launched their annual outlook in March 2020, offering a look ahead at the next five years and beyond across key trends in Latin America through the lens of the region's six largest economies - Argentina, Brazil, Chile, Colombia, Mexico and Peru.

China

China Manufacturing Overcapacity Boosts Output, Stagnation Fears J. Scott Davis and Brendan Kelly Federal Reserve Bank of Dallas

China’s economy has experienced rapidly growing indebtedness and fixed asset investment since the 2008 Global Financial Crisis. Overinvestment initially showed up in a booming real estate sector, but more recently has taken hold in the industrial sector. Ultimately, it has produced overcapacity and the current phenomenon of involution—disorderly price competition that damages industry health—with producer price deflation and increasing losses among domestic firms. Such overcapacity is made possible in part by the phenomenon of zombie lending, characterized by banks unwilling to realize losses and instead rolling over the debt of unprofitable firms. This inefficient allocation of capital is enabling unprofitable firms to survive, forcing the government to engage in an anti-involution campaign to curb the resulting overcapacity.

China’s Economy: Rightsizing 2025, Looking Ahead to 2026 Daniel Rosen, Logan Wright, Oliver Melton, and Jeremy Smith Rhodium Group

According to Rhodium’s analysis, China's actual 2025 GDP growth fell short of 3%. For domestic demand to lift China above 2% GDP growth in 2026, Beijing must reverse the systemic causes of household and business malaise or pile on costly demand subsidies. China’s statistics show real GDP growth of 5.2% year to date through the third quarter of 2025, an acceleration from 2024. They will almost certainly claim 5% growth or better for the full year. A year ago, we said China could perform better in 2025, hitting 3 to 4.5% if Beijing prioritized growth after a poor 2024 performance in the mid-2s. With late-2025 growth sputtering around 1% and a charm offensive aiming to encourage American hopes for a great power deal, Beijing is talking loudly about supporting domestic growth in 2026. But domestic growth hasn’t stalled for want of talk: Pledges have been abundant, yet China remains dependent on a trillion-dollar (and growing) trade surplus that steals growth from others. For domestic demand to lift China above 2% GDP growth in 2026, Beijing must reverse the systemic causes of household and business malaise or pile on costly demand subsidies.

Seatbelts for Speeders: Why Beijing Ignores Washington’s Red Phone Carla Freeman and Alison McFarland/War on the Rocks

In early November, after meeting China’s defense minister, U.S. Secretary of Defense Pete Hegseth performed a longstanding ritual in military relations between the United States and China: He announced that the two countries would “set up military-to-military channels to deconflict and de-escalate” problems between them. Like most rituals, this one is unlikely to have any practical effect. The pursuit of effective crisis communications channels between the American and Chinese militaries to mitigate the risk of crisis escalation has been a work in progress since President Bill Clinton was in office. Progress, however, has been halting and largely unproductive. Washington and Beijing, it is true, have managed to negotiate multiple agreements on crisis communications mechanisms, but when actual crises erupt, Beijing rarely uses these links.

Implications of Russia’s War on Ukraine

As Russia’s war grinds on, its society is fraying Washington Post

There is no outlet for public frustration and no relief from the mounting national exhaustion with a nearly four-year-long war that is corroding the country from within and making society more dysfunctional, broken, and paranoid, according to observers and those interviewed for this article. Over the past year, the Russian economy has lurched from spectacular growth to near stagnation. Russia’s digital repression and isolation are deepening as more apps and platforms are banned. According to Western intelligence, more than a million Russian fighters have been killed or wounded — many in battles for marginal gains. And as Moscow’s search for internal enemies intensifies, its machine of repression is turning on its own children and patriots.

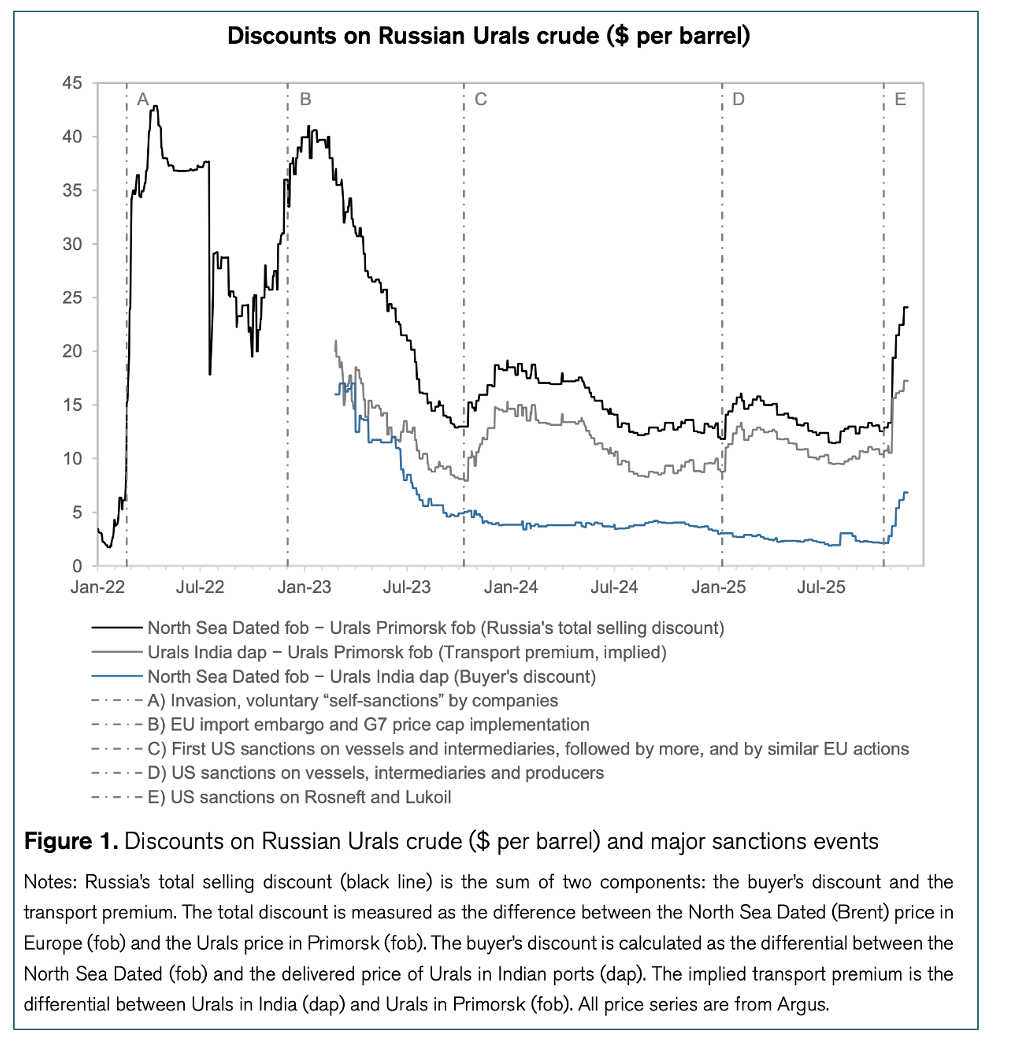

Sanctions on Rosneft and Lukoil: Initial impacts and policy implications Stockholm Centre for Eastern European Studies

Initial market impacts have been substantial. Russian export volumes have fallen, and the Urals discount has widened to its highest level since early 2023 (–$24 per barrel, or 37 percent). Rosneft’s and Lukoil’s international assets have experienced significant operational disruptions and forced divestment processes. US enforcement will be the key determinant of impacts going forward. Importers and intermediaries are likely assessing the strength of the US commitment before deciding whether to comply with, defy, or attempt to evade the sanctions. Weak enforcement would likely allow export volumes to rebound and discounts to narrow. European policymakers should support US sanctions while also considering additional measures that do not rely heavily on US coordination or commitment.

Geoeconomics

Global Working Hours Amory Gethin and Emmanuel Saez National Bureau of Economic Research

Abstract: This paper uses labor force surveys from 160 countries to build a new microdatabase on hours worked covering 97% of the world population in cross section. We also construct time series spanning over 20 years in 87 countries. Hours worked per adult are slightly bell-shaped with GDP per capita but weakly correlated with development overall. Hours worked by the young (aged 15-19) and elderly (aged 60+) decline with development, driven by growing school attendance and public pension coverage. Hours worked among prime-age adults (aged 20-59) are mildly bell-shaped with development for men while they are increasing for women. The fall in male hours in middle-to-higher income countries is driven by reduced hours per worker and is offset by increases in female labor force participation. These two forces have exactly compensated each other in many countries, leading to a remarkable long-run stability of prime-age hours worked.

The effects of commuting and working from home arrangements on mental health Journal of Social Science & Medicine

Abstract: In this study, we quantify the effects of commuting time and working from home (WFH) arrangements on the mental health of Australian men and women. Leveraging rich panel-data models together with home-job-spell fixed effects, we first show that the adverse effects of commuting time are modest in magnitude and manifest only among men with poor levels of mental health (0.01 SD decrease per 10-minute increase of commuting time). Second, we show that WFH arrangements have large positive effects on women’s mental health, provided that the WFH component is large enough. The effects are once again concentrated among individuals with poor levels of mental health (0.2 SD increase corresponding to working from home 50–75 % of the time). This uncovered contingency of effect sizes on the reported levels of mental health is novel and extends beyond Australia: we show that it also underlies the adverse effects of commuting time on the mental health of British women. Our findings highlight the importance of targeted interventions and support for individuals who are dealing with mental health problems.