Recommended Weekend Reads

States and Products Most at Risk if USMCA Ends, Four Scenarios for Cuba’s Endgame, Quantum Computing’s Massive National Security Risk, and How to Save Europe

June 26 - 28, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them of interest and useful as well. Have a great weekend.

The Americas

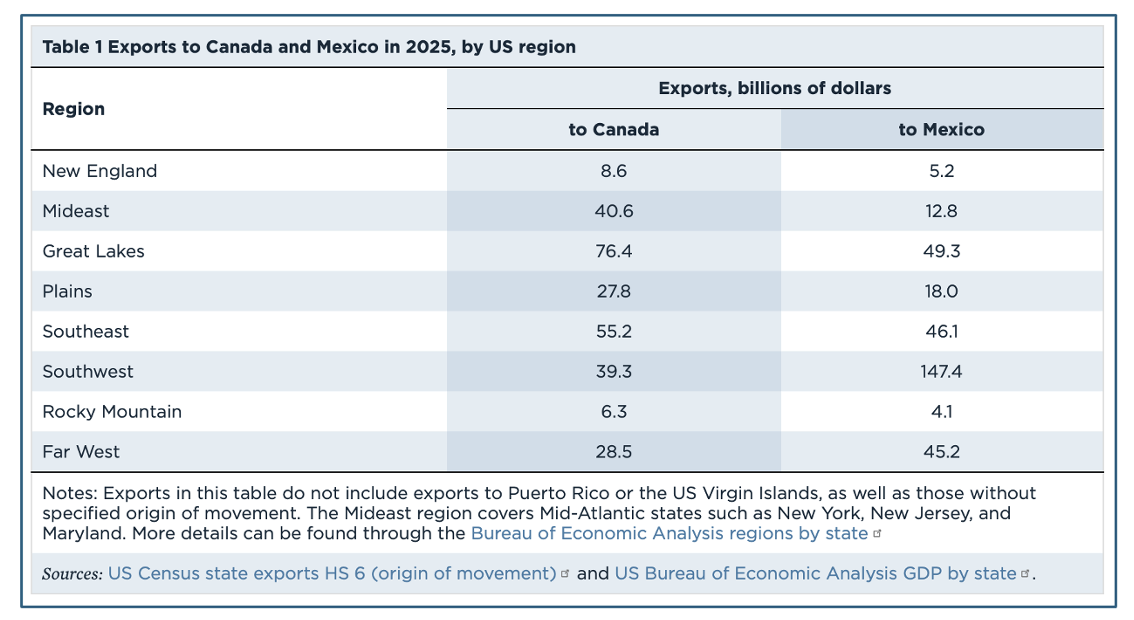

Which States and Products Risk the Greatest Losses if the USMCA is Terminated? Gary Clyde Hufbauer & Ye Zhang/Peterson Institute for International Economics

The United States-Mexico-Canada (USMCA) trade agreement, negotiated in the last year of President Donald Trump’s first term in 2020, called for the parties to decide whether to renew its terms by July 1. That deadline will no doubt be missed. Fitful negotiations started earlier this year, indicating fierce disagreements over many issues. Outright termination of the USMCA in the course of the current 6-year review is highly unlikely. But the risk is not zero for the simple reason that Trump is making heavy demands on Canada and Mexico while offering no concessions on US trade barriers. The purpose of this blog post is to highlight the risk that the third termination scenario poses to the most exposed US states and product categories. If termination looms on the political horizon in the course of the 6-year review, these states and producers (along with others) can be expected to voice strong opposition.

Cuba’s Crisis: Four Near-Term Scenarios Americas Quarterly

Senior Trump Administration officials have increasingly framed developments on the island as a direct threat to U.S. national security. Secretary of State Marco Rubio has cited Cuba’s humanitarian crisis, foreign intelligence facilities, alleged ties to terrorist organizations, and growing drone capabilities as threats to the U.S. homeland. Whether Washington is pursuing a defined objective or deliberately preserving strategic flexibility remains unclear. What is evident is that the administration is expanding its options. Four scenarios seem increasingly likely: 1) Humanitarian intervention, 2) Limited coercive action, 3) Internal regime fracture, or 4) Negotiated concessions.

A Way Out of Cuba’s Dead End The Crisis Group

The U.S. has long employed coercion to produce political change in Cuba, but little compares to its present campaign. With Cubans suffering tremendous hardship, the standoff cannot continue indefinitely. Havana’s best bet is to pursue meaningful reform while impressing the dangers of intervention upon Washington.

Latin America’s Slow But Steady Pivot Toward Africa Americas Quarterly

Africa feels distant from a Latin American and Caribbean perspective. Media coverage is sporadic, diplomatic channels are frail, and transportation connectivity is almost non-existent. Africa, however, is steadily increasing its presence and political clout, a trend that demands our attention. Together, the regions have more than two billion people, more than a third of the world’s freshwater resources, and the rainforests on Earth. They also hold significant reserves of the critical minerals on which the global energy transition depends. Latin America and the Caribbean’s exports to Africa have increased by more than 60% in the last decade. The main types of exports are agricultural products and consumer goods, economic areas that hold significant growth potential for the region. The Development Bank of Latin America and the Caribbean, CAF, has highlighted the region’s role in providing agricultural products to Africa, a net food importer whose population is forecasted to grow to 2.5 billion by 2050. CAF recently co-published its first joint report with the African Union, which reads like a business plan for a relationship that has waited too long to be taken seriously.

Latin America has turned Trumpy. That creates opportunities The Economist

In little more than a year, seven Latin American countries have held presidential elections—and right-wingers have won them all. Never has the regional pendulum swung so fast. Barring Brazil and Mexico, nearly every sizeable Latin country now has a leader who either courts Donald Trump or sounds like him. The latest is Abelardo de la Espriella, who was formally declared president-elect of Colombia on June 24th after a tight race. He calls himself El Tigre and promises to “hunt down” gangsters “in their burrows”. This Trumpian “Orange Wave” has risen because voters are sick of gangs and illegal migrants. Centrists and leftists have failed to calm their fears. Populists on the right offer tough-sounding solutions. If Mr. Trump can mass-deport migrants, they reason, why can’t we? If he can blow up drug boats, why shouldn’t we be ruthless? Such messages have proved popular. In economic matters warm ties with the White House are clearly helpful. The region relies on trade with the United States. Chums may be spared the stiffest tariffs, and sometimes receive direct help. Argentina’s painful but necessary economic reforms might have failed, had they not been led by a pro-Trump president, Javier Milei. The US Treasury extended him a $20bn credit line to avert a currency crisis.

Europe

How European NATO allies are stepping up, by the numbers The Atlantic Council

This year’s NATO Summit takes place at a critical time for the Alliance. Political churn across the Atlantic is high, magnified by the recent US conflict with Iran, a country that shares a border with summit-host Turkey, and by US President Donald Trump’s frustrations that European allies did not do enough to back the US campaign in the region. This is the latest flashpoint in a broader pattern of transatlantic friction that includes territorial provocations over Greenland and public spats with European leaders such as German Chancellor Friedrich Merz. All of it threatens to overshadow a gathering that should, by the numbers, be a moment to show genuine progress. With no marquee deliverable like last year’s 5 percent defense spending target for the Alliance to boast, NATO leadership will point to progress from European allies on three key issues: defense spending, defense industrial production, and aid to Ukraine. Expect the message from NATO Secretary General Mark Rutte to be that European allies are stepping up in meaningful ways. By almost every quantitative measure, Europe is doing more now than ever before.

The Only Way to Save Europe Foreign Affairs Magazine

The European Union today faces a set of external challenges that threaten its very existence. In December 2025, Pentagon officials told European diplomats that the continent must assume leadership of NATO by 2027, suggesting that the transatlantic alliance may be coming to an end. Meanwhile, Washington’s decision to go to war with Iran, made without serious consultation with its European allies, has produced a global energy crisis and raised further doubts about U.S. reliability. Europeans have only one option for responding effectively to these dual threats: they must complete the project of European integration. The way forward is to connect the reform proposals of Mario Draghi, the former Italian prime minister and former president of the European Central Bank, with German leadership. Draghi argues for accelerating integration by crafting a common EU policy on artificial intelligence, defense, and energy. Germany is the only country with the political strength to push the bloc in such a direction, and its leaders understand the urgency of the moment: at the World Economic Forum in Davos in January, German Chancellor Friedrich Merz acknowledged the unraveling of the international order and highlighted the importance of increasing EU unity and competitiveness in response.

Germany’s Pensions Plans Draw Praise and Outrage Der Welt

A 33-point plan to reform Germany’s pension system has drawn praise and criticism in almost equal measure. Centrist politicians have called it a good compromise, but opposition parties on the left and right are unhappy.

AI, Quantum Computing, Housing, and Oil Price Shock

The State of the AI Economy Exponential View

Over the past 12 months, the AI ecosystem generated $110 billion in revenue when you remove double-counting. Annualising the most recent month’s revenues indicates a $175 billion revenue run rate. AI revenues cover the capital investment that’s required to build the infrastructure. Our model separates AI-oriented CapEx from ordinary CapEx across the major hyperscalers and neoclouds, the specialist AI cloud providers. This adjustment is important because hyperscalers were already spending around $120 billion annually on CapEx before ChatGPT. We capture the additional investment in AI infrastructure, then depreciate compute assets over 6 years and other infrastructure over 14 years. Our modelling shows that revenues attributable to hyperscalers just about clear the depreciation expense. Six years is defensible. That longer useful life reflects that, one, demand still exceeds available AI compute, and two, operators are getting better at managing GPU fleets. Both help. The second alone is enough to justify a longer economic life.

The Coming Quantum National Security Crisis Anne Neuberger/Foreign Affairs

Because quantum computing has the potential to crack the encryption most broadly used by governments and individuals alike, the threat that it poses to national security is difficult to overstate. The cryptography that secures much of the Internet today relies on the difficulty that conventional computers have solving certain math problems, such as factoring very large numbers. Quantum computers, however, are expected to perform some of these computations far more efficiently, enabling attackers to break the codes and seize sensitive data.

Congress Passed a Major Housing Bill. It Won’t Help You Buy a Home. Arthur Gailes & Edward Pinto, Barron’s

Many in Washington are hailing the 21st Century ROAD to Housing Act, passed by Congress this week, as the most important federal housing bill in years. The bipartisan bill targets the country’s housing affordability crisis by capping institutional investors’ ownership of single-family homes and removing obstacles to home building. It eliminates an expensive requirement to build manufactured housing on permanent steel frames, streamlines environmental reviews, and incentivizes cities to provide preapproved home designs, which will simplify things for governments, regulators, and builders. Beyond that, it likely won’t change the homeownership equation for Americans. Congress can’t unfreeze the market by lowering mortgage rates, which have been stuck above 6% since 2022, nor can it meaningfully shrink the six-million-unit housing shortage through the Act’s supply measures. Even if the president decides to sign it into law—a big “if” since he backed out of a signing ceremony on Wednesday—real progress on housing affordability will have to be made at the state level.

U.S. economy less vulnerable to geopolitical oil price shocks than in the past Federal Reserve Bank of Dallas

The 2026 Iran war has raised the question of how exposed the U.S. economy is to geopolitical oil supply disruptions. It is widely believed that the U.S. economy has become less vulnerable to such disruptions, as it has reduced its dependence on oil and changed from a major net oil importer to a net oil exporter. Recent Federal Reserve Bank of Dallas research shows that the response of U.S. real (inflation-adjusted) GDP growth to this shock is only one-twentieth of what it would have been in 1980. Moreover, the response of U.S. real GDP growth today is only one-sixth of the decline in the rest of the world.

Supply chain uncertainty, energy prices, and inflation European Central Bank Working Paper

Abstract: Using U.S. and Euro area data, we document that (i) the pass-through of energy prices to inflation is state-dependent - stronger when supply chain uncertainty is elevated – and (ii) in such states, energy prices become more informative about logistical conditions. We develop a model in which firms combine energy and a specialized input transported through a capacity-constrained transportation network. When congestion binds, energy remains available in local markets at a premium, whereas the specialized input is subject to delivery delays. Because energy prices reflect both raw energy shocks and transportation conditions, firms treat them as noisy signals of supply disruptions and update beliefs through Bayesian learning. This signal-extraction channel increases perceived marginal costs, generating an uncertainty wedge that amplifies and propagates energy shocks. Within a general-equilibrium New Keynesian model, the mechanism raises the impact elasticity and the persistence of inflation in response to transitory energy shocks. This challenges the conventional monetary policy prescription to “look through” supply disturbances.