Fulcrum Perspectives

An interactive blog sharing the Fulcrum team's policy updates and analysis.

Recommended Weekend Reads

States and Products Most at Risk if USMCA Ends, Four Scenarios for Cuba’s Endgame, Quantum Computing’s Massive National Security Risk, and How to Save Europe

June 26 - 28, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them of interest and useful as well. Have a great weekend.

The Americas

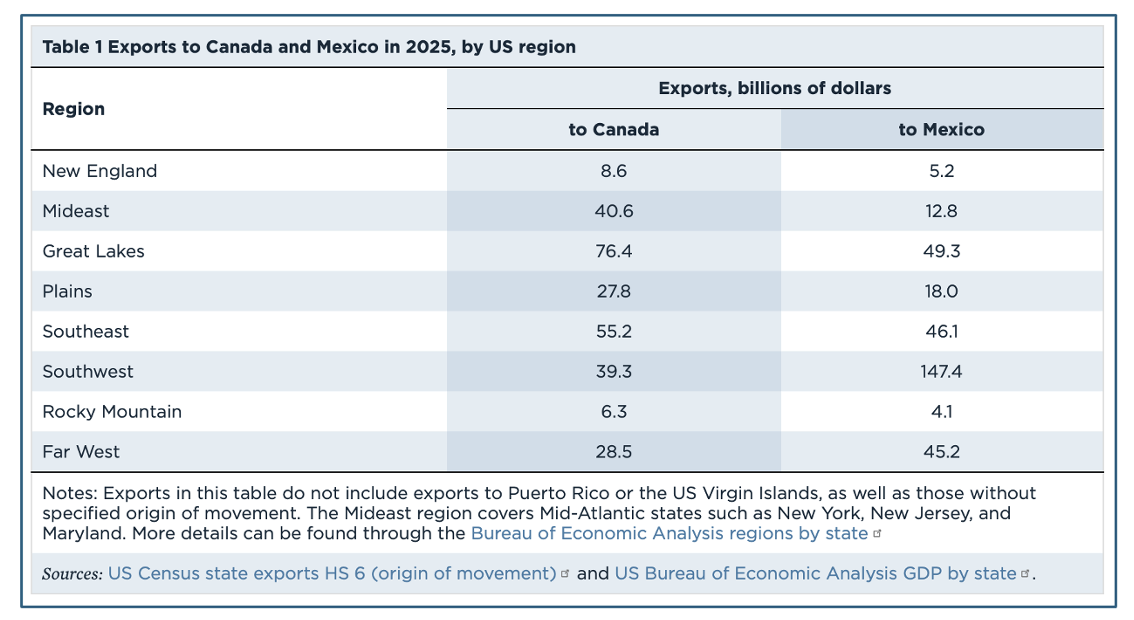

Which States and Products Risk the Greatest Losses if the USMCA is Terminated? Gary Clyde Hufbauer & Ye Zhang/Peterson Institute for International Economics

The United States-Mexico-Canada (USMCA) trade agreement, negotiated in the last year of President Donald Trump’s first term in 2020, called for the parties to decide whether to renew its terms by July 1. That deadline will no doubt be missed. Fitful negotiations started earlier this year, indicating fierce disagreements over many issues. Outright termination of the USMCA in the course of the current 6-year review is highly unlikely. But the risk is not zero for the simple reason that Trump is making heavy demands on Canada and Mexico while offering no concessions on US trade barriers. The purpose of this blog post is to highlight the risk that the third termination scenario poses to the most exposed US states and product categories. If termination looms on the political horizon in the course of the 6-year review, these states and producers (along with others) can be expected to voice strong opposition.

Cuba’s Crisis: Four Near-Term Scenarios Americas Quarterly

Senior Trump Administration officials have increasingly framed developments on the island as a direct threat to U.S. national security. Secretary of State Marco Rubio has cited Cuba’s humanitarian crisis, foreign intelligence facilities, alleged ties to terrorist organizations, and growing drone capabilities as threats to the U.S. homeland. Whether Washington is pursuing a defined objective or deliberately preserving strategic flexibility remains unclear. What is evident is that the administration is expanding its options. Four scenarios seem increasingly likely: 1) Humanitarian intervention, 2) Limited coercive action, 3) Internal regime fracture, or 4) Negotiated concessions.

A Way Out of Cuba’s Dead End The Crisis Group

The U.S. has long employed coercion to produce political change in Cuba, but little compares to its present campaign. With Cubans suffering tremendous hardship, the standoff cannot continue indefinitely. Havana’s best bet is to pursue meaningful reform while impressing the dangers of intervention upon Washington.

Latin America’s Slow But Steady Pivot Toward Africa Americas Quarterly

Africa feels distant from a Latin American and Caribbean perspective. Media coverage is sporadic, diplomatic channels are frail, and transportation connectivity is almost non-existent. Africa, however, is steadily increasing its presence and political clout, a trend that demands our attention. Together, the regions have more than two billion people, more than a third of the world’s freshwater resources, and the rainforests on Earth. They also hold significant reserves of the critical minerals on which the global energy transition depends. Latin America and the Caribbean’s exports to Africa have increased by more than 60% in the last decade. The main types of exports are agricultural products and consumer goods, economic areas that hold significant growth potential for the region. The Development Bank of Latin America and the Caribbean, CAF, has highlighted the region’s role in providing agricultural products to Africa, a net food importer whose population is forecasted to grow to 2.5 billion by 2050. CAF recently co-published its first joint report with the African Union, which reads like a business plan for a relationship that has waited too long to be taken seriously.

Latin America has turned Trumpy. That creates opportunities The Economist

In little more than a year, seven Latin American countries have held presidential elections—and right-wingers have won them all. Never has the regional pendulum swung so fast. Barring Brazil and Mexico, nearly every sizeable Latin country now has a leader who either courts Donald Trump or sounds like him. The latest is Abelardo de la Espriella, who was formally declared president-elect of Colombia on June 24th after a tight race. He calls himself El Tigre and promises to “hunt down” gangsters “in their burrows”. This Trumpian “Orange Wave” has risen because voters are sick of gangs and illegal migrants. Centrists and leftists have failed to calm their fears. Populists on the right offer tough-sounding solutions. If Mr. Trump can mass-deport migrants, they reason, why can’t we? If he can blow up drug boats, why shouldn’t we be ruthless? Such messages have proved popular. In economic matters warm ties with the White House are clearly helpful. The region relies on trade with the United States. Chums may be spared the stiffest tariffs, and sometimes receive direct help. Argentina’s painful but necessary economic reforms might have failed, had they not been led by a pro-Trump president, Javier Milei. The US Treasury extended him a $20bn credit line to avert a currency crisis.

Europe

How European NATO allies are stepping up, by the numbers The Atlantic Council

This year’s NATO Summit takes place at a critical time for the Alliance. Political churn across the Atlantic is high, magnified by the recent US conflict with Iran, a country that shares a border with summit-host Turkey, and by US President Donald Trump’s frustrations that European allies did not do enough to back the US campaign in the region. This is the latest flashpoint in a broader pattern of transatlantic friction that includes territorial provocations over Greenland and public spats with European leaders such as German Chancellor Friedrich Merz. All of it threatens to overshadow a gathering that should, by the numbers, be a moment to show genuine progress. With no marquee deliverable like last year’s 5 percent defense spending target for the Alliance to boast, NATO leadership will point to progress from European allies on three key issues: defense spending, defense industrial production, and aid to Ukraine. Expect the message from NATO Secretary General Mark Rutte to be that European allies are stepping up in meaningful ways. By almost every quantitative measure, Europe is doing more now than ever before.

The Only Way to Save Europe Foreign Affairs Magazine

The European Union today faces a set of external challenges that threaten its very existence. In December 2025, Pentagon officials told European diplomats that the continent must assume leadership of NATO by 2027, suggesting that the transatlantic alliance may be coming to an end. Meanwhile, Washington’s decision to go to war with Iran, made without serious consultation with its European allies, has produced a global energy crisis and raised further doubts about U.S. reliability. Europeans have only one option for responding effectively to these dual threats: they must complete the project of European integration. The way forward is to connect the reform proposals of Mario Draghi, the former Italian prime minister and former president of the European Central Bank, with German leadership. Draghi argues for accelerating integration by crafting a common EU policy on artificial intelligence, defense, and energy. Germany is the only country with the political strength to push the bloc in such a direction, and its leaders understand the urgency of the moment: at the World Economic Forum in Davos in January, German Chancellor Friedrich Merz acknowledged the unraveling of the international order and highlighted the importance of increasing EU unity and competitiveness in response.

Germany’s Pensions Plans Draw Praise and Outrage Der Welt

A 33-point plan to reform Germany’s pension system has drawn praise and criticism in almost equal measure. Centrist politicians have called it a good compromise, but opposition parties on the left and right are unhappy.

AI, Quantum Computing, Housing, and Oil Price Shock

The State of the AI Economy Exponential View

Over the past 12 months, the AI ecosystem generated $110 billion in revenue when you remove double-counting. Annualising the most recent month’s revenues indicates a $175 billion revenue run rate. AI revenues cover the capital investment that’s required to build the infrastructure. Our model separates AI-oriented CapEx from ordinary CapEx across the major hyperscalers and neoclouds, the specialist AI cloud providers. This adjustment is important because hyperscalers were already spending around $120 billion annually on CapEx before ChatGPT. We capture the additional investment in AI infrastructure, then depreciate compute assets over 6 years and other infrastructure over 14 years. Our modelling shows that revenues attributable to hyperscalers just about clear the depreciation expense. Six years is defensible. That longer useful life reflects that, one, demand still exceeds available AI compute, and two, operators are getting better at managing GPU fleets. Both help. The second alone is enough to justify a longer economic life.

The Coming Quantum National Security Crisis Anne Neuberger/Foreign Affairs

Because quantum computing has the potential to crack the encryption most broadly used by governments and individuals alike, the threat that it poses to national security is difficult to overstate. The cryptography that secures much of the Internet today relies on the difficulty that conventional computers have solving certain math problems, such as factoring very large numbers. Quantum computers, however, are expected to perform some of these computations far more efficiently, enabling attackers to break the codes and seize sensitive data.

Congress Passed a Major Housing Bill. It Won’t Help You Buy a Home. Arthur Gailes & Edward Pinto, Barron’s

Many in Washington are hailing the 21st Century ROAD to Housing Act, passed by Congress this week, as the most important federal housing bill in years. The bipartisan bill targets the country’s housing affordability crisis by capping institutional investors’ ownership of single-family homes and removing obstacles to home building. It eliminates an expensive requirement to build manufactured housing on permanent steel frames, streamlines environmental reviews, and incentivizes cities to provide preapproved home designs, which will simplify things for governments, regulators, and builders. Beyond that, it likely won’t change the homeownership equation for Americans. Congress can’t unfreeze the market by lowering mortgage rates, which have been stuck above 6% since 2022, nor can it meaningfully shrink the six-million-unit housing shortage through the Act’s supply measures. Even if the president decides to sign it into law—a big “if” since he backed out of a signing ceremony on Wednesday—real progress on housing affordability will have to be made at the state level.

U.S. economy less vulnerable to geopolitical oil price shocks than in the past Federal Reserve Bank of Dallas

The 2026 Iran war has raised the question of how exposed the U.S. economy is to geopolitical oil supply disruptions. It is widely believed that the U.S. economy has become less vulnerable to such disruptions, as it has reduced its dependence on oil and changed from a major net oil importer to a net oil exporter. Recent Federal Reserve Bank of Dallas research shows that the response of U.S. real (inflation-adjusted) GDP growth to this shock is only one-twentieth of what it would have been in 1980. Moreover, the response of U.S. real GDP growth today is only one-sixth of the decline in the rest of the world.

Supply chain uncertainty, energy prices, and inflation European Central Bank Working Paper

Abstract: Using U.S. and Euro area data, we document that (i) the pass-through of energy prices to inflation is state-dependent - stronger when supply chain uncertainty is elevated – and (ii) in such states, energy prices become more informative about logistical conditions. We develop a model in which firms combine energy and a specialized input transported through a capacity-constrained transportation network. When congestion binds, energy remains available in local markets at a premium, whereas the specialized input is subject to delivery delays. Because energy prices reflect both raw energy shocks and transportation conditions, firms treat them as noisy signals of supply disruptions and update beliefs through Bayesian learning. This signal-extraction channel increases perceived marginal costs, generating an uncertainty wedge that amplifies and propagates energy shocks. Within a general-equilibrium New Keynesian model, the mechanism raises the impact elasticity and the persistence of inflation in response to transitory energy shocks. This challenges the conventional monetary policy prescription to “look through” supply disturbances.

Recommended Weekend Reads

June 12 - 14, 2026

The Battle Over Data Centers, Is the iPhone Birth Control?, Germany’s Evolving Defense Policy, and US Debt Levels Won’t Be Sustainable in 20 Years

Below are a number of studies, research reports, and news analyses we read this past week. We thought you might find them of interest and, hopefully, of use. Please let us know if you have any questions.

The Growth and Growing Battle Over Data Centers

Latin America’s Data Center Gold Rush: Myth and Reality Americas Quarterly

The numbers speak for themselves: Google is building an $850 million data center in Uruguay; Amazon committed $5 billion to a new cloud region in Mexico; and Microsoft is investing $2.7 billion in cloud and AI infrastructure in Brazil. From Montevideo to Querétaro, data center providers are expanding capacity, governments are rolling out tax incentives, and multilateral banks are publishing frameworks to help countries “capture the data center opportunity.” The opportunity is real. So is the risk of misreading it. Latin America and the Caribbean are emerging as credible destinations for digital infrastructure investment for reasons that go beyond hype. The region’s electricity matrix is a structural asset: Brazil generates nearly 90% of its electricity from renewables, and companies like Equinix, Ascenty and Scala have expanded aggressively in São Paulo for exactly that reason.

OpenAI’s Threat Report: “Data Center Bandwagon” The Special Competitive Studies Project

In this YouTube interview, OpenAI’s Ben Nimmo, who leads the company’s intelligence and investigations work, details a covert influence operation — likely out of China — that used ChatGPT to generate content posted by fake accounts posing as Americans, aimed at one surprising target: America’s own data centers. Ben connects it to a pattern that should worry anyone tracking the AI race, and answers the question— why reach for ChatGPT instead of China’s own DeepSeek?

America’s Data-Center Build-Out Is Falling Way Behind Schedule Wall Street Journal

Tech companies are earmarking unprecedented sums of money to finance the build-out of massive data centers, with a planned $85 billion equity-raise by Google being the latest example. But even as the piles of capital secured have grown ever larger, the ability to deploy it in the artificial-intelligence race has become less certain. Supply-chain backlogs, permitting fights and availability of power supplies are among the issues that have caused the construction of data centers to fall behind targeted timelines, with the gap growing wider in recent months: A JPMorgan analysis last month found that more than 60% of data-center capacity planned for completion in 2027 isn’t yet under construction, and another 7% is delayed. It is a seeming paradox: If hyperscalers can’t break ground on many of the projects they have already announced, what difference can hundreds of billions of dollars more make—however eager Wall Street may be to supply it?

Demographics

·Is the iPhone Birth Control? Causal Evidence from AT&T’s 2007–2011 Carrier Monopoly Caitlin Myers & Ezekiel Hooper/National Bureau of Economic Research

Abstract: The U.S. general fertility rate has fallen by 22% since 2007, a sustained decline not readily explained by economic conditions, contraceptive use, housing or childcare costs, or other commonly cited factors. We assess the potential role of a different shock: the diffusion of the smartphone. The U.S. rollout of the iPhone, the first modern smartphone, provides a natural experiment: from June 2007 through February 2011, the device was sold only on AT&T, allowing us to identify its effect from variation in AT&T’s mobile broadband coverage. Entropy-balanced Poisson and synthetic difference-in-differences event studies imply that access to the iPhone reduced births by 4.5–8.0% at ages 15–19 and 3.2–6.6% at ages 20–24, with statistically significant but smaller declines among older cohorts. Placebo analyses applied to Verizon and Sprint’s pre-2011 coverage footprint are null. Taken together, these cohort effects imply that the diffusion of the iPhone deepened the decline in births among women under 30 while suppressing the rise in births among older women. Overall, the diffusion of the iPhone explains 33–52% of the decline in the general fertility rate among women aged 15–44. National-survey evidence on time use and sexual behavior is consistent with the iPhone reducing in-person interactions, increasing pornography use, and reducing sexual frequency.

India’s population will soon be falling—probably quite fast The Economist

In 1950 India’s population was 360m. The average woman had six children—roughly the same as an American woman a century earlier. Today, with a population of 1.45bn, India accounts for a sixth of humanity. It surpassed China as the world’s most populous country in 2023 and has kept growing. But its total fertility rate (tfr), the number of births a typical woman has over her lifetime, has fallen to 1.9 (see chart 1), below the level needed to keep the population stable in the long run. Although the population will keep growing for a spell, as the generation that are currently children themselves become parents, a future contraction is inevitable unless the fertility rate rises back above 2.15. In practice, it is likely to keep falling, accelerating the impending shrinkage. In Delhi, for instance, the tfr is 1.2.

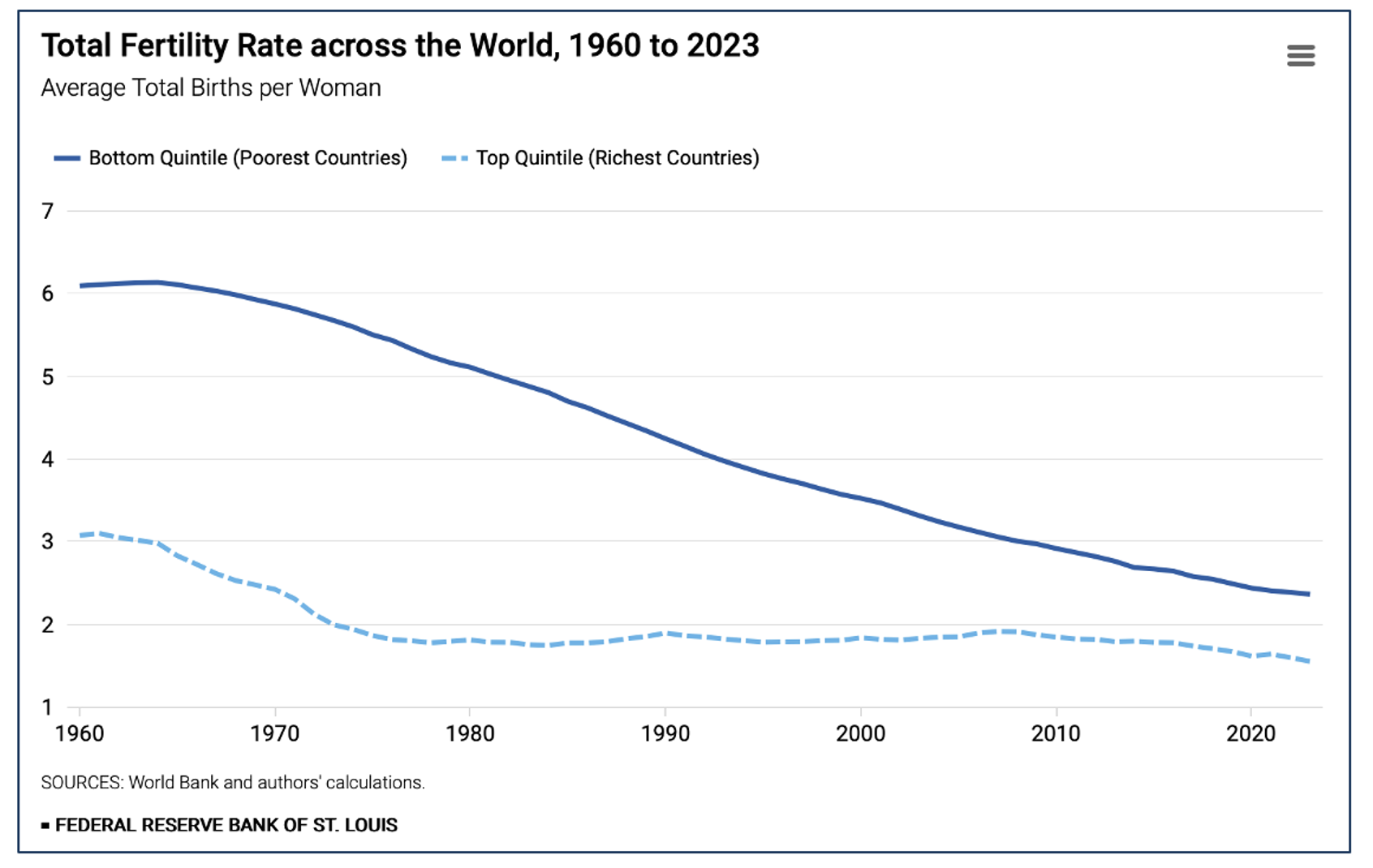

Declining Fertility Rates Across the World Federal Reserve Bank of St. Louis

The total fertility rate (TFR), or the average number of births per woman over her entire reproductive life, is one factor affecting population growth. Trends in the TFR have implications for the world’s demography. Although poor countries have a higher TFR than rich countries, the rate has been declining in both for 60 years. This has narrowed the TFR gap between the poorest and richest countries from three children per woman to less than one child per woman. In rich countries, the TFR has been lower than the rate needed to maintain population levels for a few decades. But the TFR in low-income countries remains higher than the replacement rate.

Europe’s Evolving Defense Strategy: The German Perspective

Understanding Germany's Defense Strategy Chain Reaction Podcast/Foreign Policy Research Institute

The podcast features a conversation with FPRI President Aaron Stein and Roderich Kiesewetter, a Member of the German Bundestag (CDU/CSU) who has held various command and staff positions, including at the EU Council , NATO and the German Ministry of Defense. The two discuss the strategic framework of the recently released German defense policy, key reforms and capabilities, and what strength means in the new European security environment.

Making Defense European Again European Council on Foreign Relations

Between an expansionist Russia and a careless America, one thing is clear: Europeans must be prepared to defend themselves, and quickly. To do so, they need to adopt a distinctly European way of defense. They cannot hope to replicate America’s security approach, nor do they need a new institutional superstructure. Rather, they need to be pragmatic and resourceful by building on what exists. A European way of defense has three pillars. First, a layered decision-making architecture would draw on NATO’s command structure for military operations; on the EU for funding and pan-European solidarity; and on minilateral arrangements for fast adaptability. Second, Europeans would build up their military capabilities, capacity and readiness to deter and defend effectively with little to no American help. Third, all of this must rest on a coordinated European defense industry wherever possible and draw on capabilities from diversified, allied sources if needed. This model would set Europeans up to defend themselves with America where possible, with less America where necessary and without America if it comes to that.

The Overall Concept of Military Defense: Military Strategy and Plan for the Armed Forces German Federal Minister of Defense

The German Ministry of Defense recently published its first-ever integrated military strategy connecting threat assessment to force structure to capability investment over a defined timeline — the most serious attempt in the history of the Federal Republic to close the gap between strategic understanding and actual defense commitment. The plan runs in three phases: a rapid buildup through 2029, a capability-focused expansion through 2035, and a longer-term technology-driven phase through 2039 and beyond. Together with its allies, Germany aims to be ready to deploy at least 460,000 troops to deter potential aggression.

The U.S. Federal Debt

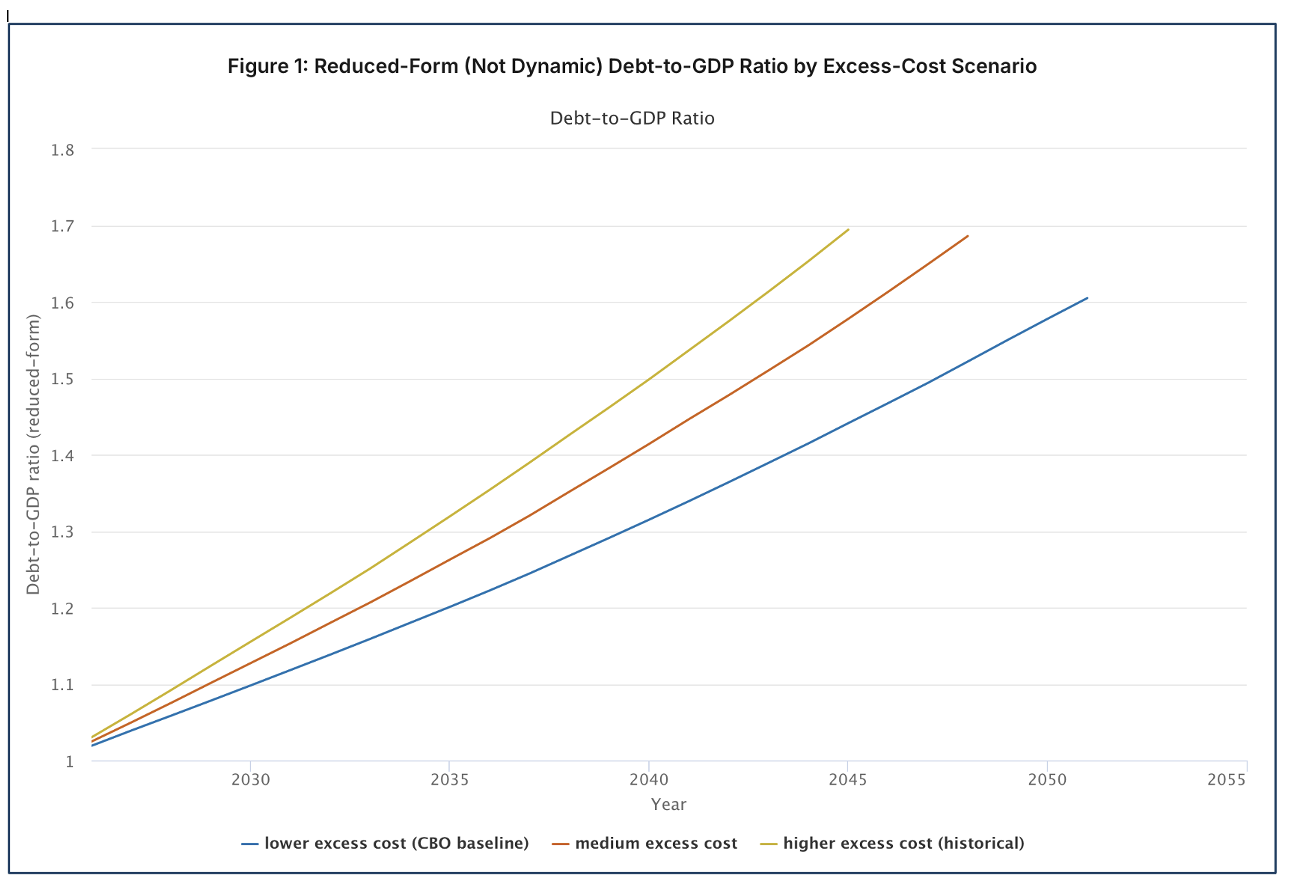

When Does Federal Debt Reach Unsustainable Levels? Spring 2026 – Onward Penn Wharton Budget Model

The Penn Wharton center estimates that the United States federal debt cannot rationally exceed roughly 210 percent of GDP as an outer limit. Under historical excess cost growth in healthcare, this outer limit is likely reached within 20 years; there is a 25% chance of reaching it in 14 years. Debt markets unravel earlier if beliefs about government repayment shift.

Recommended Weekend Reads

Assessing The Iran War’s Global Economic Shocks, The Myths and Realities of Petrodollars, The Fog of AI War, and How the U.S. Post Office is About to Collapse

April 17 - 19, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them of interest and useful as well. Have a great weekend.

More On the Impact of the Iran War

How the War in the Middle East Is Affecting Energy, Trade, and Finance International Monetary Fund

According to the IMF, “Although the war could shape the global economy in different ways, all roads lead to higher prices and slower growth. A short conflict might send oil and gas prices soaring before markets adjust, while a long one could keep energy expensive and strain countries that rely on imports. Or the world may settle somewhere in between—tensions linger, energy stays costly, and inflation proves hard to tame—with ongoing uncertainty and geopolitical risk. Much depends on how long the conflict lasts, how far it spreads, and how much damage it inflicts on infrastructure and supply chains.”

"Look Through" the Hormuz Shock if You Want. U.S. Inflation is Still Running Hot Matt Klein/The Overshoot

Core goods inflation was running ~1 percentage point above pre-pandemic levels in both 2023 and 2024, with price declines slowing from mid-2024 onward — before tariffs became a primary factor. The question for policymakers is what this “one-time thing”, as Federal Reserve boss Jerome Powell has called it, will do to the underlying trend rate of inflation.

Petrodollars. Myths and Reality Brad Setser Council on Foreign Relations

The Iran War has brought renewed focus to the role of Petrodollars. The foundation of the dollar’s global role, it is sometimes argued, rests on the willingness of the Gulf countries (but not Russia) to price their oil in dollars. But it was never quite clear why oil pricing mattered quite as much as some claim. To be sure, there are network effects around dollar pricing. But it isn’t hard to pay for oil in a global currency like the euro, even if the underlying contract is priced in dollars. There is a deep and liquid market for converting euros into dollars, and a firm aiming to lock in the euro price of oil 3 months forward can buy oil forward in dollars and dollars forward with euros, thereby locking in a euro price. Dollar settlement is a problem for countries that are sanctioned by the U.S. and the EU and for frontier economies that cannot settle their oil bill in local currency, but it hasn’t required most European oil importers to build up big stocks of dollar reserves just to pay for oil. What has mattered at times is how the big oil exporters manage their surplus funds when there is a surge in the global price of oil.

Three Scenarios for the Gulf States After the Iran War Carnegie Emissary

Amid a tenuous U.S.-Iran ceasefire, Arab Gulf monarchies are aiming to project strength. “We prevailed through an epic national defense . . . in the face of treacherous aggression,” Emirati diplomatic adviser Anwar Gargash wrote on X. Saudi-owned newspaper Asharq Al-Awsat emphasized the kingdom’s “intensive political consultations” with regional countries as leading to the present calm. Yet member states of the Gulf Cooperation Council (GCC) still face immense challenges in shoring up their security. A substantial U.S. and Israeli air campaign was unable to eliminate Iran’s will or capability to exert power in the Gulf, with Iran turning historically secure neighbor states into war zones overnight. Neither the United States nor any other actor put forward a decisive solution for the de facto Iranian closure of the Strait of Hormuz, while the Islamic Republic retains its highly enriched uranium and its nuclear program. And the GCC has no seat at the table, despite its entreaties, for negotiations that will shape the bloc’s economic and security environment for years to come. Where do the Gulf states go from here? We offer three scenarios—a hopeful one, a realistic one, and a cautionary one—that illustrate both potential areas of cooperation and the risks of greater fragmentation.

What the Iran War Means for the “Axis of Resistance” Hamidreza Azizi/Foreign Affairs

The war is heightening the salience of Shiite identity across multiple arenas at once and, in doing so, reshaping how political and military actors assess both their interests and their risks. Groups that might otherwise have remained on the sidelines are becoming more likely to get involved in the strife, and those already fighting face growing pressure to escalate. The consequence is a feedback loop: actions driven by fears of marginalization provoke responses that alarm more and more people, expanding the social base for Shiite mobilization. The “axis of resistance,” Iran’s network of nonstate allies and proxies across the region, has endured numerous setbacks since 2023. But ongoing U.S. and Israeli military actions may lead to its reconstitution, not through the orchestration of Tehran but rather as a result of the altogether more organic impetus of an embattled Shiite identity.

Europe

A Transatlantic Economic Reset Penny Nass/German Marshall Fund

The fixation on tariffs and trade skirmishes obscures a more consequential reality, one in which the EU-US relationship is being shaped by a rapidly deteriorating geopolitical environment that tests political trust and strategic coordination. It also overshadows the fact that the transatlantic relationship is not primarily a trade relationship but the world’s largest and most strategically significant investment partnership. Three areas demand urgent join action: Critical minerals, the Digital Stack, and Infrastructure.

The Fog of AI War Raluca Csernatoni/Carnegie Strategic Europe

An irreducible uncertainty haunts every battlefield: the fog of war. And for two centuries, military innovation has promised to lift that fog. Artificial Intelligence (AI) was supposed to be the technology that finally did so, replacing human guesswork with machine precision and processing oceans of data at speeds that would render uncertainty obsolete. But acknowledging the advantages is not the same as ignoring what happens when speed, attrition, and scale become organizing principles of warfare. U.S. President Donald Trump's dispute with Anthropic, which insisted that its models should not be used without guardrails against fully autonomous weapons and mass domestic surveillance, ended with the Pentagon designating the company a supply chain risk. The message from the world’s largest military power is that normative constraints on military AI are obstacles to innovation rather than preconditions for lawful use. Europe can play a key role in all of this.

Assessing the damage: What the Iran war really means for Europe’s defense European Union Institute for Security Studies

Regardless of whether the ceasefire between the US and Iran holds, the war in the Middle East complicates European rearmament and support for Ukraine, while also further eroding confidence in the United States as a reliable guarantor of Europe's defense. To put their defense ramp-up on a firmer footing, Europeans should reduce exposure to US political volatility, industrial bottlenecks, and the diversion of defense equipment during wartime.

Geoeconomics, Technology, and Trade

A Tax Revolt Is Under Way In America The Economist

Democrats and Republicans alike think they are overtaxed, as do both rich and poor. YouGov’s polling finds that around 60% of Americans at every income level think they are taxed too much—despite being taxed at very different rates. Statehouses are hearing this, too. Many, citing strong economic growth, have cut taxes in recent years. Enthusiasm is building to go further and faster, leaving some observers wary. “Most have done so responsibly thus far,” says Jared Walczak of the Tax Foundation, a think-tank. “But they now risk overreaching and making reductions they cannot afford.” A wave of localities is pushing through property-tax exemptions for retirees. Florida is flirting with abolishing non-school property taxes altogether. Ohio has a possible ballot initiative to scrap them in all forms.

Evaluating the Impact of Tariffs on US Agriculture a Year After Liberation Day Joseph Glauber/American Enterprise Institute

In April 2025, the Trump administration levied 10 percent tariffs on virtually all countries and higher “reciprocal” tariffs on certain countries, ushering in a new and uncertain tariff architecture that saw significant changes, exemptions, and additional actions over the following year. The tariffs modestly reduced overall US agricultural and food imports, but with significant heterogeneity by exporting country and product category. The tariffs had mixed effects on US agricultural exports, with exports to China and Canada falling partly because of retaliatory tariffs and consumer reactions, respectively. After imposing the tariffs, the United States negotiated several bilateral trade deals with other countries. However, given the lack of product-specific details, China’s continued retaliatory measures, and the Supreme Court’s decision striking down most of the US tariffs, it is unclear whether these deals will actually improve agricultural market access for US exporters.

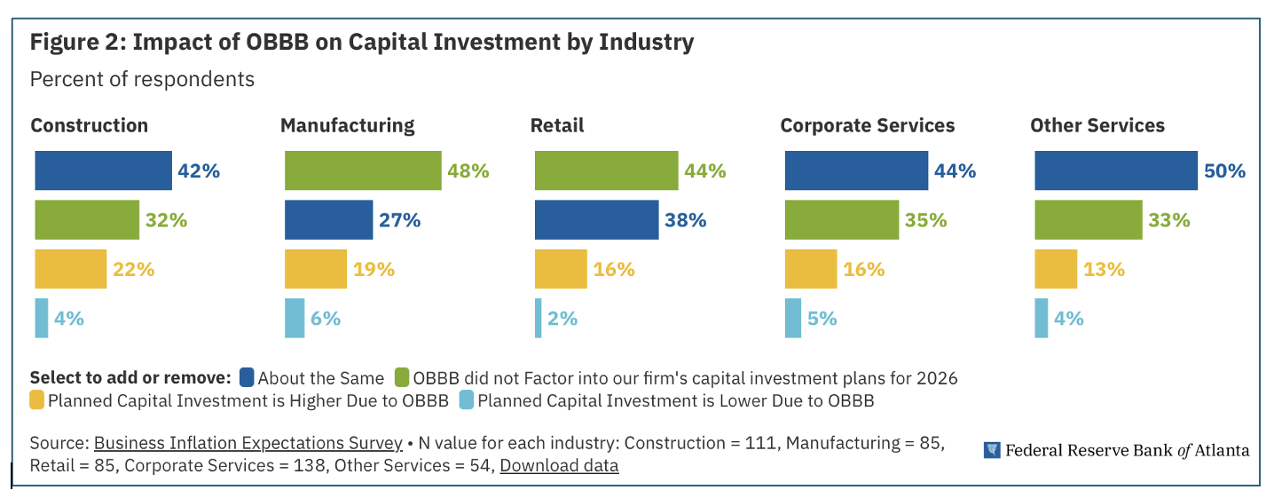

Did the OBBB Affect Firms' Plans for 2026? Federal Reserve Bank of Atlanta

Around 20 percent of respondent firms in the Atlanta Fed's Business Inflation Expectations (BIE) survey told us that they consider the One Big Beautiful Bill (OBBB) in their decision-making and short-term planning. The remaining firms said they did not factor in the OBBB when planning for outcomes such as capital expenditures, employment, and sales revenue forecasts. These results may be a reflection of the fact that many of the provisions of the law were already in place and with the passage of OBBB are now extended or made permanent (such as provisions of the 100 percent bonus depreciation and the 20 percent deduction for qualified business income). Our findings suggest that a broad-based and sizeable future surge in business activity stemming from the policy change may not be likely.

Congress Seeks Solution for Averting USPS Fiscal Collapse Kevin Kosar/Washington Examiner

Last month, U.S. Postmaster General David Steiner added another major item to Congress’s already long to-do list: rescuing the Post Office. “The Postal Service is at a critical juncture. At our current rate, we’ll be out of money in less than 12 months.” That may not sound like a big deal. Government agencies run out of money each year, and every January and February, they go hat-in-hand to Congress and ask for funding. Usually, they get it, and when Congress fails to deliver the dollars, agencies close for a bit or their staff work without pay until legislators enact a spending law. The U.S. Postal Service is different. USPS is one of 17 government corporations that pay for themselves by earning revenue through the sales of goods and services. The agency sells around $80 billion in postage each year, mostly to large companies offering credit cards (e.g., Capital One) or selling goods (e.g., Walmart). When the Post Office runs out of cash in the first half of 2026, Steiner explained, “the Postal Service would be unable to deliver the mail.”

Recommended Weekend Reads

Focus on Cuba, Venezuela, and Peru, Iran, and A Look at The Global Implications of the War, and China Cracks Down on “Bone-Ash” Burials in Empty Apartments

April 10 - 12, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them of interest and useful as well. Have a great weekend.

The Americas: Focus on Venezuela, Cuba, and Peru

Preparing for the Consequences of Collapse in Cuba Christopher Hernandez-Roy & Team/Center for Strategic and International Studies

Much has been written on what comes next for Cuba—in terms of U.S. pressure, regime change or regime management, and who might be Cuba’s “Delcy”—with less focus on the impact that U.S. policy is having on the people of Cuba, who already faced a dire humanitarian situation created by their leaders. What consequences would stem from a sudden collapse of the regime, and what should the United States and the international community be doing to prepare for this eventuality?

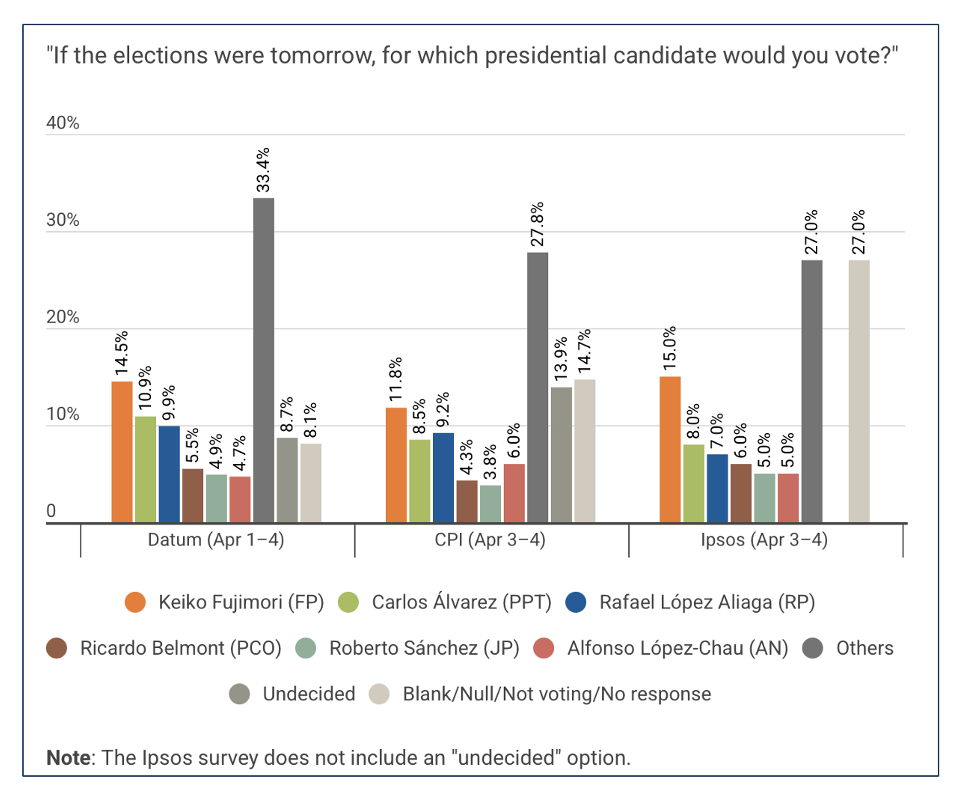

Peru: Meet the Candidates 2026 Americas Quarterly

A record 36 candidates are now vying for the presidency, crowding the field and reflecting the country’s fragmented political landscape. If no candidate wins more than 50% of the vote on April 12, the top two will advance to a June 7 runoff. All seats in Congress are also up for election in the high-stakes April 12 contest. For the first time in decades, the country will vote to choose a Senate, the result of a 2024 electoral reform that reinstituted a bicameral system and reversed a ban on consecutive terms for legislators. All winners will be elected to a five-year term. For this analysis, AQ has included only candidates polling above 6% in recent IPSOS surveys, listed in alphabetical order by last name, and has asked eight nonpartisan experts on Peru to help us identify where each candidate stands on two spectrums: left versus right on economic matters, and personalistic versus institutionalist on leadership style.

Poll Tracker: Peru’s 2026 Presidential Election Americas Society/Council of the Americas

The AS/COA has been closely monitoring the upcoming Peru elections. Via this link you can dive into the details of voter polling in advance of the election and post-election analysis.

Peru’s Dysfunctional Politics Are an Economic Time Bomb Bloomberg

Peru has had three presidents since October, yet markets have largely remained unaffected, with country risk and credit default swaps only marginally increasing. The economy continues to expand, with exports hitting records and inflation remaining low, despite the political turmoil and a fuel-price shock in March. The upcoming general election may not resolve the country’s political instability, and the next government will likely face challenges in addressing corruption, insecurity, and geopolitical pressures.

Venezuela’s Treacherous Recovery: The Peril and Promise of an Economic Boom Moisés Naím/Foreign Affairs

Venezuela may soon experience something it has not seen in years: a surge of economic growth and activity. Although the removal of President Nicolás Maduro by U.S. forces in January left his deputy, Delcy Rodríguez, in place, it has nonetheless opened possibilities that for decades seemed out of reach. Political prisoners are slowly being released, exiles are considering returning home, investors are exploring new opportunities, and countries are reopening their embassies in Caracas. Venezuelans’ long-suppressed hopes are flaring back to life. However, many Venezuelans have great expectations for what the future might hold. Should the state fail to deliver, it could plunge the country into chronic political instability. The only way to guarantee that an economic recovery serves all Venezuelans is to also ensure a political recovery, one in which institutions can once again constrain executive power and in which the will of the public finally finds expression in elections that are genuinely free and fair.

Venezuela Seems to Be Going … Well? Missy Ryan/The Atlantic

Three months after U.S. troops snatched Nicolás Maduro and brought him to New York, life in Venezuela has returned to normal, whatever normal is in a nation that has been gripped by turmoil and economic calamity for years. Government services and the bleak economic conditions that Venezuelans have been living under haven’t improved much, but there is a sense of optimism that Maduro’s departure brings the possibility of better days. Oil revenue is increasing. And Washington’s handpicked interim authorities, led by Maduro’s vice president, Delcy Rodríguez, have rolled out a succession of investor-friendly measures devised by their new North American patrons. A recent pollappears to bear this out. The survey, from Atlas Intel and Bloomberg, shows that nearly 80 percent of Venezuelans think their country is the same or better off now than under Maduro; 54 percent said that greater U.S. influence is positive; 52 percent say that the country’s civil liberties have increased. Trump could only wish for such favorable numbers at home.

What Happens Next with Iran and The Possible Implications of the War For the Rest of the World

The Iran War’s Real Lessons for China: U.S. Tactical Successes Should Give Beijing PauseForeign Affairs

The performance should give pause to U.S. adversaries that have been watching the war in Iran unfold. Massive volleys of long-range drones and ballistic missiles are a preferred offensive tool of China, North Korea, and Russia, used to pound military bases and headquarters, sink fleets, and level civilian infrastructure. If a U.S. adversary were to undertake a war of aggression in Asia or Europe,its plan would be to launch strikes to try to neutralize U.S. and allied military forces, likely inflicting high civilian losses in the process, and then use that cover to carry out its war objectives. The success of high-end Western missile defenses against Iranian strikes calls such a plan into question. Ballistic missiles and drones may not be the decisive offensive weapons that many countries thought them to be. They could still be effective in a campaign of attrition and coercion—but this would be a slow process, not a path to quick victory.

The war on Iran: Nobody won, everyone paid Mahjoob Zweiri/Al Jazeera

Yet before the architecture of this agreement is examined, it is worth pausing to assess the conflict itself: its origins, its legal standing, and who ultimately absorbed its costs. he US-Israeli campaign has failed to achieve its goals. Iran has been badly hit, and the Gulf is paying the bill too.

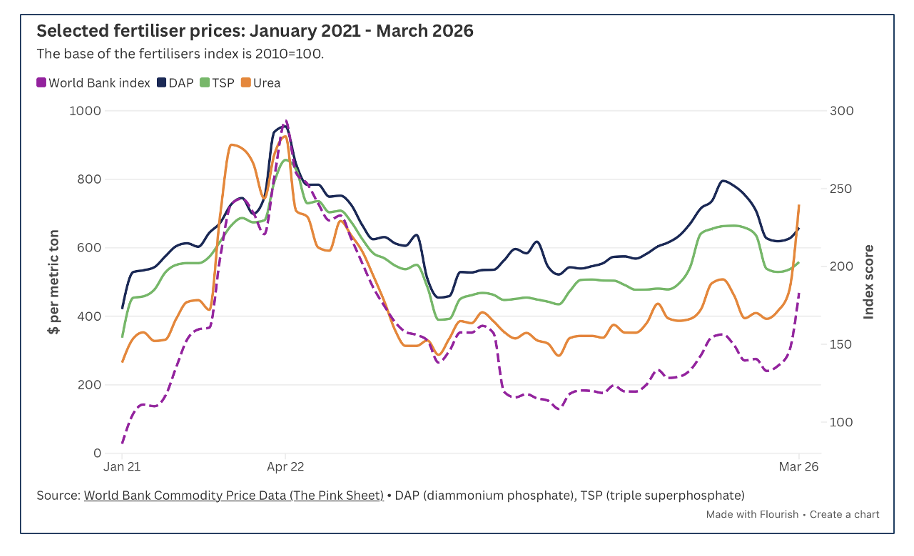

Hormuz Exposes Africa’s Fertilizer Structural Risk African Futures Blog

For Africa, the recent tensions in the Middle East are exposing an already known, deeper dependency. The continent’s agricultural systems largely rely on fertilizer supply chains shaped by external production hubs, energy markets and geopolitical risk. In addition to rising costs of direct agricultural input, disruptions in fertilizer supply chains can quickly affect food prices and availability, as many African countries have high import volumes and bills for foodstuffs. Domestic fertilizer production in Africa remains uneven and insufficient to meet the growing demand, with many countries depending heavily on imports to sustain agricultural output. Production capacity exists in parts of North and West Africa, driven by massive phosphate deposits and natural gas reserves. Morocco leads in phosphates, accounting for over 50% of Africa’s supply, and ranks among the top five global phosphate fertilizer exporters, while Nigeria, Egypt and Algeria dominate in nitrogenous (urea) fertilizer production.

Geoeconomics, Demographics, and Tech

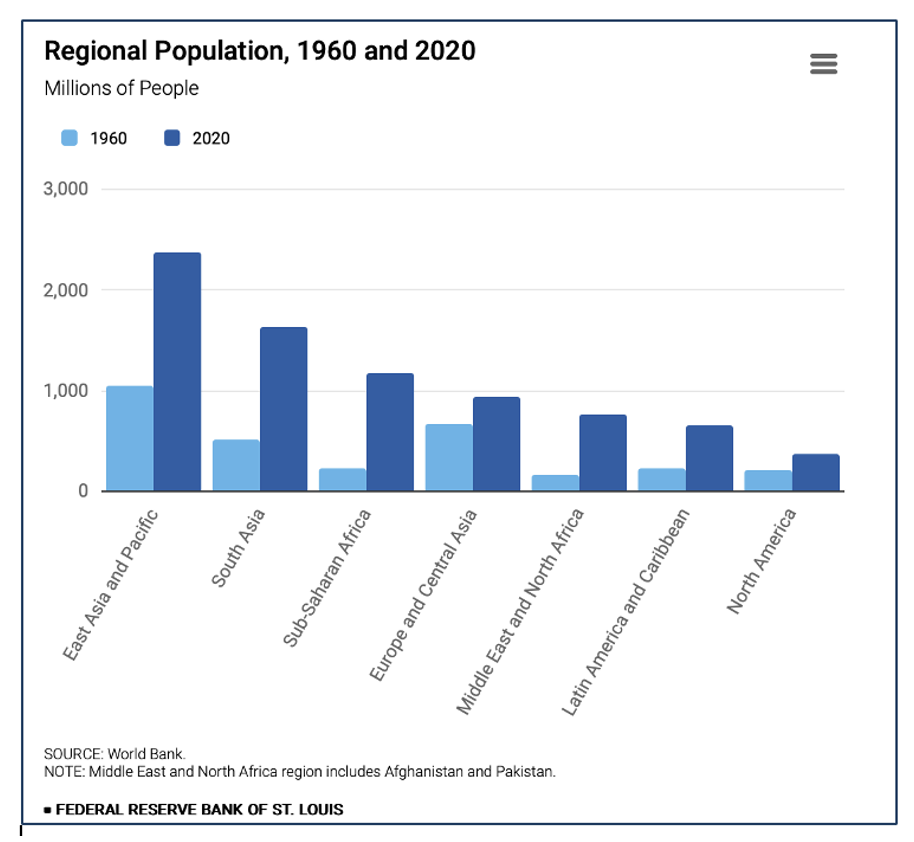

How Regions Shaped World Population Growth since 1960 Federal Reserve Bank of St. Louis

World population has increased from approximately 3 billion in 1960 to almost 8 billion in 2020. While global population growth is significant, some countries are concerned about declining population trends within their borders. This blog post documents population shifts across various geographic regions. While North American population increased from 199 million to 370 million, South Asian population increased from 508 million to 1.6 billion and sub-Saharan African population increased from 228 million to almost 1.2 billion.

China Cracks Down On ‘Bone Ash’ Burials In Empty Apartments Financial Times

Chinese funeral expenses were 45% of the mean annual wage in 2020. As real estate prices declined, many families started using empty apartments as “bone ash apartments.” The practice was formally outlawed two weeks ago. Rapid urbanization has raised demand for limited cemetery plots in cities. Coupled with this, China’s population is ageing at one of the fastest paces in history. The number of deaths in 2025 was 11.3mn, up from 9.8mn in 2015 and outpacing 7.9mn births last year. In contrast to apartments, whose prices have fallen sharply since President Xi Jinping’s campaign that “properties are for living in, not for speculation,” cemetery plots have become prohibitively expensive. A global funeral expense survey in 2020 by the insurer SunLife showed that China’s average funeral expenses were the second highest in the world at about Rmb 37,375 ($5,400), after Japan, accounting for about 45% of average annual wages. While residential properties in China carry 70-year usage rights from the government, cemetery plots come with only a 20-year lease.

Space for the Departed: Land Scarcity and Bone-Ash Apartments in ChinaXinyi Wu/Pitzer College, Claremont Graduate University

Abstract:The rise of bone ash apartments in China reflects a layered response to urban land scarcity, shifting funeral policies, and real estate speculation. As the state mandates cremation and restricts private cemetery development, traditional burial customs are increasingly reshaped by spatial limitations, economic pressures, and political regulation. For some families, bone ash apartments function as modern ancestral halls—domestic spaces for remembrance and ritual continuity. For others, they represent a pragmatic investment strategy, offering long-term storage of ashes within assets that retain market value. This thesis examines how urban planning, state funeral policy, real estate dynamics, and the disintegration of neighborhood relationships collectively give rise to this phenomenon. Rather than interpreting bone ash apartments as merely a cultural departure or financial tactic, the study argues that they embody a complex convergence of spatial constraint, ritual transformation, political governance, and socio-economic adaptation within the conditions of contemporary urban China.

Private Credit Markets Theory, Evidence, and Emerging Frontiers Jiacheng Zou/Cornell University

Abstract: Private credit assets under management grew from $158 billion in 2010 to nearly $2 trillion globally by mid-2024, fundamentally reshaping corporate credit markets. This paper provides a systematic survey of the academic literature on private credit, organizing theory and evidence around four questions: why the market has grown so rapidly, how direct lender technology differs from bank lending, what risk-adjusted returns investors earn, and whether the sector poses systemic risks.

The payment system puts a floor on the Fed’s balance sheet The Brookings Institute

If the Federal Reserve wants to shrink its massive balance sheet—as President Trump’s nominee to be the next Fed Chair, Kevin Warsh, advocates—it must find ways to reduce the demand by banks for reserve deposits at the Fed or risk severe disruptions to money markets. On the asset side of its balance sheet ($6.6 trillion in mid-March), the Fed holds mainly Treasury securities and government-guaranteed mortgage-backed securities. The Fed’s largest liability is in the form of reserve balances, currently totaling about $3 trillion. These are deposits held at the Fed by banks. The Fed controls short-term interest rates primarily through the interest rate it pays on those balances.

Recommended Weekend Reads

How Maduro’s Capture Puts Cuba at an Inflection Point, Mexico’s Morena Party is Floundering, The Iranian Regime Will Break – Then What Happens?, and the Geography of Science

January 23 - 25, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them interesting and useful as well. Have a great weekend.

The Americas

The Geopolitics of Maduro’s Capture: Cuba’s Inflection Point Christopher Hernandez-Roy/Center for Strategic and International Studies

The release of the US 2025 National Security Strategy that declared a “Trump Corollary” to the Monroe Doctrine, along with the early January U.S. military action in Venezuela, is altering political calculations across the Western Hemisphere, with deep implications for Cuba. The January 3, 2026, military operation to capture Nicolás Maduro and bring him to the United States to face terrorism charges, and the subsequent coercive management of the remaining Chavista regime, is a signal to the region that challenges long-standing assumptions about U.S. restraint, regime durability, change, and the use of external pressure in Latin America. Rather than pursuing traditional regime change centered on rapid democratization or wholesale dismantling of authoritarian systems, the United States has demonstrated a willingness to employ coercive power to manage regimes—controlling their behavior, extracting concessions, and preserving sufficient institutional continuity to avoid collapse.

Mexico’s mighty left-wing government is floundering The Economist

Mexico’s Morena Party has no serious rivals in Mexico. The party has dominated Mexican politics. Together with its allies, it controls 24 of Mexico’s 32 states. It holds supermajorities in both legislative houses, more than two-thirds of the seats in each. It draws comparisons with the Institutional Revolutionary Party that ruled Mexico as a one-party state for seven decades until 2000. But under Morena, Mexico has no money. Its economic growth has long lagged behind that of its neighbors in Latin America and comparable emerging economies in Asia, but the Morena years have been the most sluggish in a quarter-century. The IMF thinks the economy will grow by 1.5% in 2026, about half the Latin American average. Mexico’s President Claudia Sheinbaum’s Plan México, a flagship development strategy, is faltering: in 2025, investment reached 22% of GDP, short of the 25% target. With weak growth and little sign of a turnaround, few believe the government can maintain expansive welfare payments until the end of her term, in 2030.

Sheinbaum’s Cuba policy is testing Washington’s patience Washington Post

At a moment of extraordinary tension in the U.S.-Mexico relationship, the Mexican government is choosing to remain Cuba’s oil lifeline. For decades, Venezuela filled that role, sending up to 100,000 barrels of oil per day at the height of Hugo Chávez’s rule. In recent years, as Venezuela’s oil output faltered, Mexico has stepped up. According to industry data, it became the top supplier of oil to Cuba last year — well before the ouster of Nicolás Maduro. While the Trump administration has not publicly detailed its full strategy toward Cuba, Secretary of State Marco Rubio has signaled that the U.S. intends to bypass the Cuban government and direct assistance toward the Cuban people. Some members of Congress say Mexico’s approach points in the opposite direction.

Delcy Rodríguez and the Architecture of Venezuela’s Kleptocracy Felix Maradiaga Substack

According to an investigative report recently written by “Transparency International Venezuela in Exile” under the title “Delcy Rodríguez se blindó para la era post Maduro,” Acting Venezuelan President Delcy Rodríguez has been a central operating executive within the machinery that turned a nation’s wealth into private enrichment, political leverage, and international bargaining chips. The report notes that the Venezuelan vice presidency under Rodríguez, she received a staggering share of the national budget—40% in 2024 and 44% in 2025—concentrating extraordinary spending discretion around Rodríguez’s office.

The Iranian UprisingHow the Iranian Regime Breaks Foreign Affairs

Over the last few weeks, the Iranian regime has faced remarkable challenges—and displayed remarkable unity. Hundreds of thousands of Iranians have taken to the streets to protest the Islamic Republic in what has become the most significant internal challenge the state has faced in its 47-year history. But the elite has not yet fractured. Instead of squabbling over how to handle the demonstrations, Iran’s reformist and hardline leaders have worked together to suppress them. To date, none of the regime’s elites objected to the killings of thousands of innocent civilians by security forces. In fact, figures from across the political spectrum have all outwardly (and falsely) blamed the violence on foreign infiltrators. But behind the scenes, the picture is undoubtedly more tense. Unless they exclusively watch state television and believe their own false narratives, Iranian officials understand that the domestic system is under existential stress.

Iran’s Uprising: What’s the endgame? Brookings Institution Podcast

In recent days, the Iranian regime has conducted an unprecedented and bloody crackdown on protests across Iran. In this episode, Brookings Fellow Aslı Aydıntaşbaş is joined by two Iran experts, vice president of Foreign Policy Suzanne Maloney and visiting fellow Mara Karlin, to discuss the unique nature of the protests and the regime’s violent response, options for U.S. military action, and President Trump’s possible endgame.

Iran’s coming reckoning: Regime collapse is likely — democracy is not Middle East Institute

Since tens of thousands of Iranians took to the streets in protest and then experienced intense and gruesome repression by state security forces, the question is now: what next? Much will depend on four factors: 1) Foreign intervention 2) The behavior of the opposition 3) Information control and connectivity, and 4) Elite dynamics within the regime itself. But, as the author argues, the Islamic Republic as we know it cannot endure. However, its collapse or transformation does not guarantee liberation. What Iran is entering is not a revolution’s endgame but a dangerous interregnum — one in which brutality has proven effective, legitimacy has evaporated, and the future remains profoundly contested. But, as the author makes clear, the Islamic Republic as we know it cannot endure.

Geoeconomics

The Hollow Dollar? Alexander Evans/The British Academy & Carnegie Endowment for International Peace

Abstract: This paper explores whether the US dollar’s dominance in global finance – long a pillar of American geopolitical influence – is being quietly eroded. While the dollar remains the world’s primary reserve currency, its centrality in international payments is increasingly contested. The weaponization of the dollar, particularly through sanctions and the extraterritorial reach of the New York banking license, has prompted strategic responses from states such as China, Russia, and India. These strategic responses include the development of alternative payment systems, local currency trade settlements, and digital infrastructure. The paper argues that a ‘hollowing’ of the dollar’s infrastructural dominance is underway – (perhaps very) gradual, partial, but geopolitically significant. This shift may not end dollar supremacy, but it could fragment the global financial system, weaken US sanctions leverage, and diminish the centrality of New York and London as financial hubs. The implications for global order are subtle but potentially profound. A less dollar-dependent system may facilitate a more multipolar world yet diminish liberal democratic power.

The Geography of Science Abhishek Nagaraj & Randol Yao/

Abstract: Science has long been concentrated in the Western world, but the global research landscape is undergoing a profound reorganization. Using data on 44 million publications from 1980 to 2022, we document the geography of science in terms of who produces it, what it studies, and where it diffuses. The share of publications produced in the United States has fallen from 40% in 1980 to 15% in 2022, while China’s share has risen from near-zero to 32%. This pattern extends even to elite outlets, with China now producing over 35% of top-journal publications. Notably, this is driven not only by an expanding researcher base but also—to a large extent—by increases in individual productivity. Similar to China, other middle- and low-income countries (including India, Russia, and Brazil) have also expanded output producing as much research as high-income European Union countries combined (about 21% overall), but they remain underrepresented in top-tier journals. Overall, our findings highlight both the democratization and fragmentation of global science, raising important questions about the future of the global scientific enterprise.

The Macroeconomic Consequences of Capital Constraints Office of Financial Research, US Treasury Department

Abstract: This working paper quantifies the effect that regulatory capital requirements have on bank lending and real economic activity. Exploiting a change in capital requirements by the Federal Reserve at the onset of the pandemic recession, it establishes causally that looser requirements increased the ability for banks to extend credit to consumers. On average, banks that received relatively more balance sheet space from the policy change passed this along to their customers in the form of relatively higher credit limits from Q2 2020 to Q1 2021. This also led to relatively higher credit card borrowing among these customers. Using a general equilibrium quantitative model calibrated to match the empirical findings, the paper shows that absent the Federal Reserve policy change, consumption would have fallen by an extra 2.7% in the three years following the pandemic recession. Motivated by these estimates, this paper evaluates the efficacy of countercyclical capital requirements and finds that such policy could lower consumption volatility over the business cycle by as much as 12%.

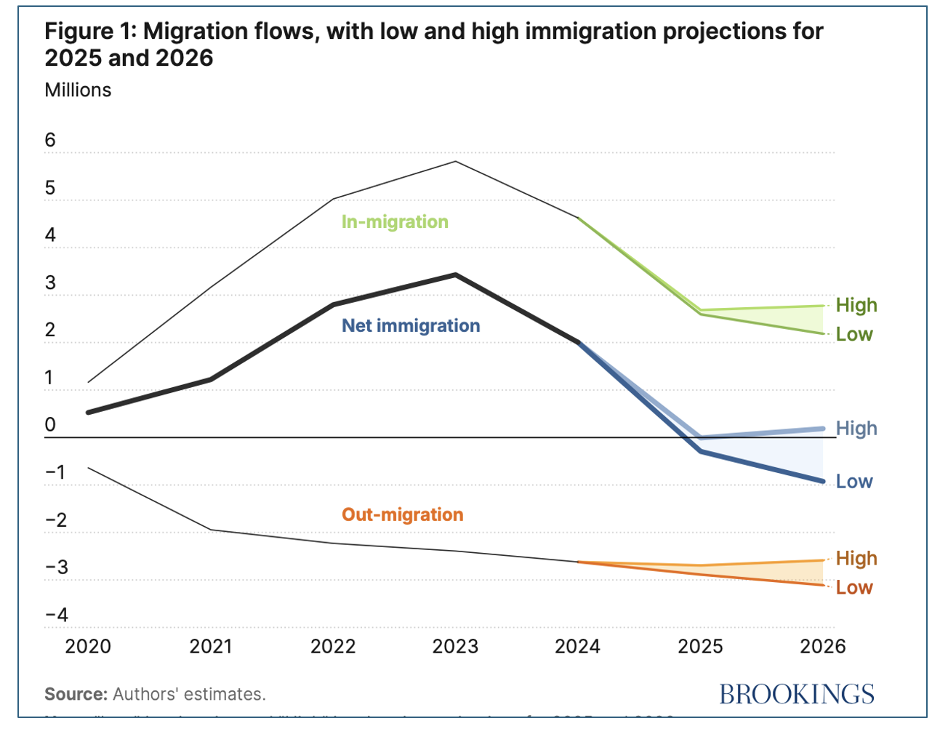

Macroeconomic Implications of Immigration Flows in 2025 and 2026: January 2026 Update The Brookings Institution

Abstract: The first year of the second Trump administration has seen dramatic changes in immigration policy, resulting in a sharp slowdown in net migration to the United States. Building on work released in late 2024 and mid-2025, we use available data combined with judgment to estimate a range of likely outcomes for net migration for the years 2025 and 2026. We conclude that net migration was likely close to zero or negative over calendar year 2025 for the first time in at least half a century. Specifically, we estimate that net migration was between –295,000 and -10,000 for the year. For 2026, we project net migration is likely to remain in negative territory. The downward pressure on population stemming from negative net migration has important implications for the macroeconomy. In recent years, growth in the U.S.-born working-age population has been weak, and nearly all growth in the labor force has stemmed from immigration flows.

Subscribe to our newsletter.

Sign up with your email address to receive news and updates.