Recommended Weekend Reads

A Deeper Dive Into Cuba, Europe’s Critical Mineral Dependency Trap, The Geography of Start-Ups During COVID, and the Case for Data Centers in Space

May 22 - 25, 2026

Happy Memorial Day Weekend! Hopefully, you will get a little time to rest and read. Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them of interest and useful as well. Have a great weekend.

Cuba

The Secretive Conglomerate that Controls Cuba’s Economy The New York Times

The most powerful entity in Cuba is not the Communist Party. It is a secretive military-run conglomerate known as GAESA which is estimated to control between 40 percent to 70 percent of the Cuban economy. It is a commercial empire established by Raul Castro – brother of the late dictatorial leader Fidel Castro – to bolster the military. Today, it controls the finest hotels, restaurants, most of the gas stations on the island, the internet, and supermarkets. The New York offers a comprehensive, inter-active report on who exactly runs GAESA and just how sprawling an empire it is.

In Cuba, Socialism Has Morphed Into A Racket: What I saw on the island that once considered itself the future Persuasion (Substack by James Bloodworth)

The author traveled to Cuba recently, touring the capital, Havana, and was appalled by what he found. In the past, apologists for the Cuban government, wanting to show that the people have enough to live on, would point to the monthly ration book—the libreta—through which Cubans received a basic food basket. But since Raúl Castro succeeded Fidel in 2008, the ration book has been steadily pared back. Today it supplies, on average, enough to subsist on for perhaps 10 days at most, and only with careful rationing. Everyday items such as toothpaste and shampoo have disappeared from it altogether. In their place is the unforgiving market: a tube of toothpaste can now cost as much as 600 pesos, around 15 percent of a typical monthly salary. That is the equivalent of spending something like $800 on a single tube.

The Dilemma Over Cuba’s Future El País

Between grandstanding, contradictory statements, and secret meetings, something is happening in Cuba. A path has opened that is still full of unknowns, but one that now seems hard to reverse. In recent days, events have accelerated with the unusual visit by the CIA chief to Havana, the U.S. indictment of Raúl Castro — the Cuban Revolution’s last great symbol — and the deployment of an aircraft carrier in Caribbean waters near the island. As to what is likely to happen next, the precedent in Caracas looms over the island, but analysts and historians see a horizon of ‘capitalism without democracy’ as more likely than regime change.

Cuba’s Soviet-Era Military Could Still Complicate U.S. Operations in a Caribbean Crisis Global Defense News

Recent U.S.-Cuba tensions have sharpened a practical military question: what Cuba’s armed forces could actually bring to bear in a crisis with the United States, and which assets would matter first. Cuba’s Revolutionary Armed Forces remain built for territorial defense, relying on Soviet-era ground equipment, layered but aging air defenses, limited combat aviation, coastal patrol forces, and mobilization manpower. A 2025 profile estimates about 50,000 active armed forces personnel, with mandatory service for men aged 17 to 28, a 24-month obligation in the armed forces or Interior Ministry, and reserve liability for men until age 45. Older open-source military tables give lower regular army figures, around 38,000 active and 39,000 reserve personnel, illustrating the uncertainty that surrounds Cuban force accounting. The important point is functional rather than numerical: the FAR is designed to combine regular units, territorial militias, internal-security forces, dispersed storage sites, and local defense zones. In practical terms, that means Cuba’s military value is concentrated in delaying, absorbing, dispersing, and imposing local costs, not in matching U.S. joint forces in mobility, air power, naval reach, or precision strike.

Europe’s Competitiveness Challenge

Out of the Dependency Trap: Why Germany’s and Europe’s Critical Raw Materials Policy Falls Short and How to Fix It Global Public Policy Institute

We find that Germany and Europe’s policy approaches are still too strongly based on the false assumption that improving framework conditions for private-sector projects in Europe and elsewhere in the world will suffice to drive supply diversification. This assumption is misaligned with the reality of China’s state-backed, vertically integrated dominance that allows Beijing to shape prices and supply conditions. As a result, policies focused primarily on stimulating supply through permitting reform, financial derisking and project support in partner countries are insufficient. Other players such as Japan and the United States (US) have responded with greater resolve, deploying tools such as coordinated offtake agreements and price-support mechanisms to actively shape market dynamics. Europe’s failure to take similar steps reflects persistent misconceptions about global CRM markets, alongside fragmented and insufficient capacity in public institutions and a weak CRM ecosystem. Past efforts along four policy levers – (1) stockpiling, (2) expansion of primary supply, (3) expansion of recycling, and (4) demand reduction – exhibit a range of shortcomings, among which one stands out: the absence of stable, long-term demand at price levels that make investment in diversified supply chains in Europe and partner countries commercially viable. Without addressing this demand-side gap, even well-designed supply-side measures will fail to unlock the investment required.

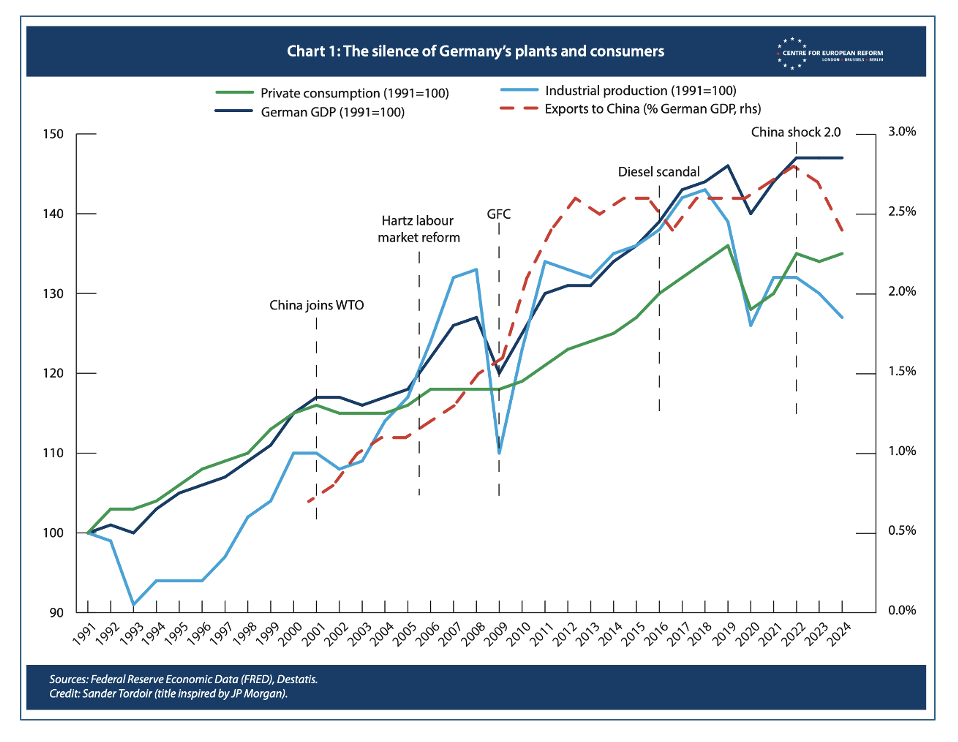

China Shock 2.0: The Cost of Germany’s Complacency Brad Setser/Sander Tordoir, Centre for European Reform

There is a growing consensus a new China shock is reverberating across global goods markets. Nowhere is that shock more consequential than in Germany. Its manufacturers in core industries – cars, machinery, chemicals and aircraft – are being simultaneously squeezed out of China and other foreign markets, and at home. The shock is worsening. Analysts had estimated China would only export 10 million cars a year by the end of the decade. But China’s 2025 fourth quarter exports, annualized, already hit that mark. The car sector is not unique. In 2025, China’s overall export volumes grew at more than twice the pace of global trade. And they gained strength in early 2026, with first quarter export volume growth at 15 per cent. The risk for Berlin, which already struggled to adjust when China’s surplus jumped from 2 to 5 per cent of GDP from 2022 to 2025, is acute. Germany faces a structural demand shock from a state-distorted rival that cannot be addressed like past competitiveness challenges: Berlin and Brussels must either bolster their trade defenses and industrial policy or prepare to offset the social and economic costs of deindustrialization at China’s hand.

How can Europe shape the Iran war’s aftermath? Nathalie Tocci/Brookings Institution

The U.S.-Israel war against Iran, encompassing the Persian Gulf and Lebanon, has revealed Europe at its worst. Looking ahead, it could also see Europe at its best. The war in Iran is laying bare a long-standing reality: Europe’s attachment to multilateralism and international law has been rooted as much in interests as in idealism. If Europeans genuinely internalize this lesson, they must be willing to act on it in concert with Gulf and Asian partners in shaping the postwar order. This neither means decoupling nor closing the door to the United States. Rather, as multilateral initiatives are planned and hopefully implemented in the region, the door should remain open for the day Washington chooses to step in.

Dawn of the Electric World Order Kate Maackenzie/Tim Sahav – Phenomenal World (Substack)

Oil and gas—the foundation of global systems of energy and production—are no longer reliably available where and when they are needed at bearable prices. Two wars in four years have triggered a permanent risk regime shift. No matter how uneven and uncertain the immediate reaction from markets and governments, the lesson of the present energy shock is unavoidable: the geopolitical conditions that once stabilized the carbon-based logistics of the modern world can no longer be guaranteed, and electrification offers a structural exit from instability. After two months of war and supply chain disruption, the situation is becoming desperate in much of Asia and Africa and roiling across Europe and the Americas. Many oil and gas importing countries are now being forced to triage: how much LNG goes to power generation versus fertilizer plants? Bidding wars will leave those without deep pockets paying in increased hunger, lost wages, and shrinking economies. It’s not just oil being affected by the war. From cooking gas to fertilizers to sulphur to helium, the war has yet again exposed the material underpinnings of the global economy and its web of interdependence. Where does this leave Europe?

Geoeconomics, AI, and Start-Ups

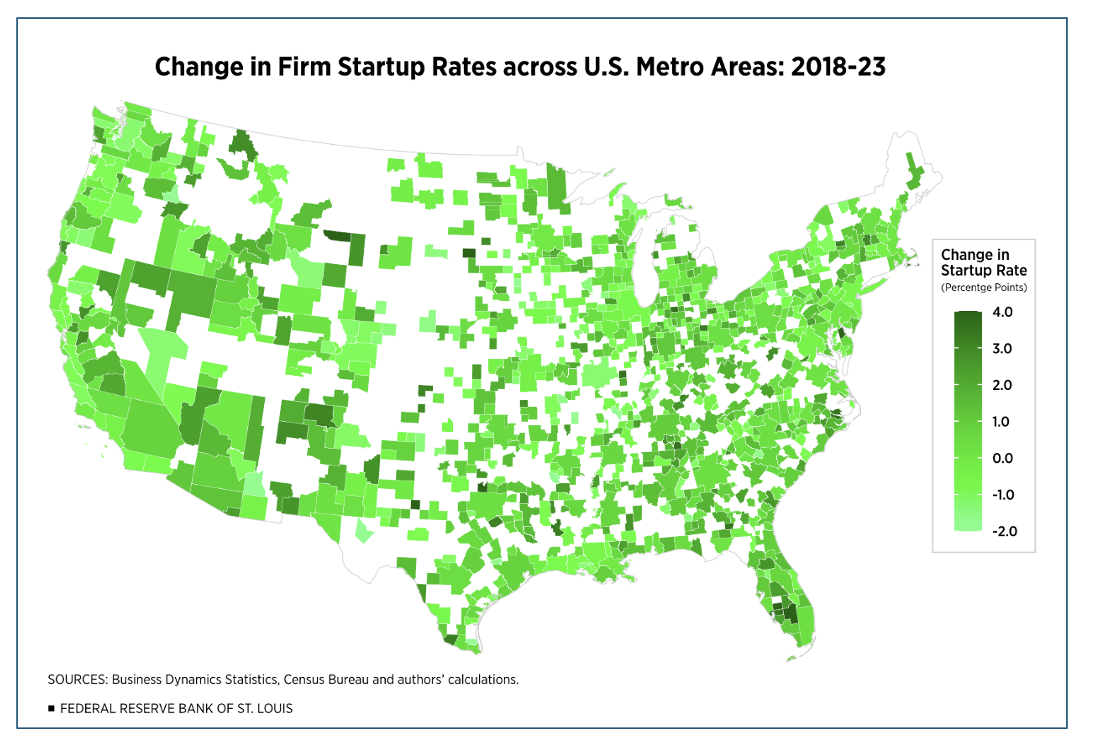

The Geography of the Startup Surge During the Pandemic Federal Reserve Bank of St. Louis

After sharply declining since the late 1970s, the firm startup rate began to steadily rise in the 2010s, with a shift toward larger cities. Startup activity then accelerated during the COVID-19 pandemic. Where did this pandemic-era growth occur? Startup growth during the pandemic was spread widely across U.S. regions instead of being concentrated in coastal tech hubs. While bigger cities continued to have higher startup rates, business formation rose across all city sizes.

The Jevons Paradox and Insatiable Humans: Why AI Won’t Empty the Finance SuiteEldar Maksymov/Arizona State University (ASU) - School of Accountancy

Abstract: The conversation around AI and white-collar work has fixated on the wrong question. Anthropic’s March 2026 finding that AI can theoretically perform 94.3 percent of business and finance tasks has executives debating which jobs will survive. They should be asking which jobs are about to come into existence. The Jevons Paradox—William Stanley Jevons’s 1865 observation that efficiency gains expand rather than contract resource use—provides the framework. Its cleanest modern test: U.S. accountants quadrupled between 1980 and 2022, growing at nearly seven times the rate of population growth, after spreadsheets automated their core work. AI is to today’s accountant what VisiCalc was to 1980’s—except more powerful. The near-term displacement is real and painful. But firms that treat AI only as a headcount-reduction tool will miss the expansion. This article maps that expansion and offers concrete prescriptions for students, executives, and educators.

The Commercial Space Race

Old Space, New Space: A Commercial Revolution in Innovation? Ruben Gaetani and Alexander T. Whalley National Bureau of Economic Research

The biggest post-1970s surge in space innovation came in the 1990s, when policy created commercial markets for satellites and communications. Incumbent firms, not “New Space” entrants, drove most of this boom and still account for most space patents. This paper uses patent data to examine the timing and composition of space innovation, finding patterns that challenge the popular narrative attributing commercial space transformation to entrepreneurial entrants after 2005. Our findings reveal that the commercial space transformation is more closely connected to its government-led origins than narratives emphasizing entrepreneurial disruption suggest.

“I’ll buy 10 of those”—NASA science chief yearns for mass-produced satellites ARS Technica

There are more opportunities to access space than ever, thanks to a bevy of commercial rockets, some with reusable boosters, led by SpaceX’s workhorse Falcon 9. So why is NASA launching fewer telescopes and planetary science missions than it did a quarter-century ago? The answer is complex. It is not necessarily the money. The space agency’s science budget this year is $7.25 billion, roughly the same as it was in 2000, adjusted for inflation. This is despite attempts by the Trump administration to drastically reduce NASA science funding.

The case for data centers in space: An Interview with Starcloud CEO Philip Johnston McKinsey

As demand for AI compute rapidly accelerates, space-based data centers have the potential to move from concept to early deployment. In practical terms, this involves packaging servers and supporting systems into space-qualified modules, powered primarily by solar energy, managing tempo, and connecting back to Earth through high-bandwidth communications links. In theory, space-based systems could offer both structural advantages, such as unconstrained energy scaling and higher solar efficiency, but also the potential for cost competitiveness with terrestrial systems. Questions remain, however, about whether space-based compute can deliver that in practice, offering predictable performance, repeatable deployment, credible reliability, and sustainable, competitive economics even after accounting for launch cadence, replacement cycles, and data-movement costs.