Recommended Weekend Reads

Trump’s IEEPA Tariffs Are Dead. Now What?, Iran: What Happens Next if the US Launches Attacks, How A BRICS Currency Could Happen, and the Looming Fiscal Crisis in the Western World

February 20 - 22, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them of interest and useful as well. Have a great weekend.

U.S. Trade Policy After the IEEPA Decision

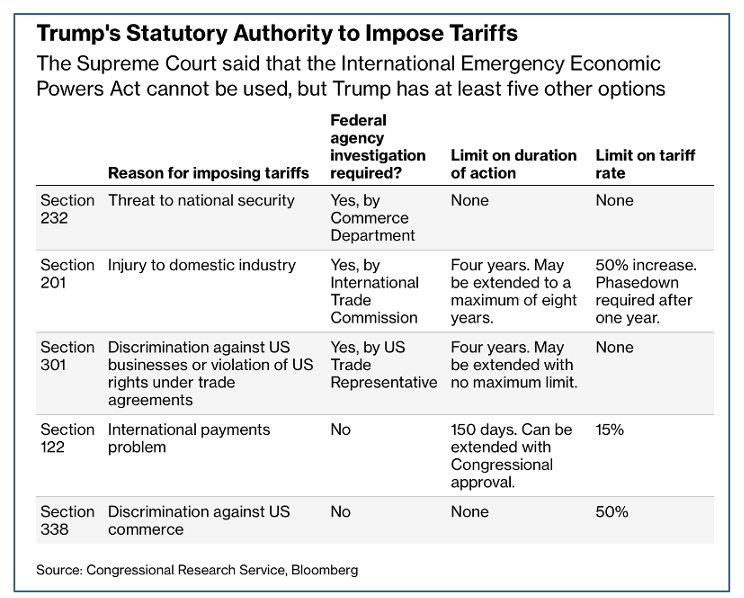

Trump’s Options After the Supreme Court Said His Tariffs Are Illegal Bloomberg

On Friday, the U.S. Supreme Court President Trump had illegally used of the International Emergency Economic Powers Act (IEEPA) for his April 2025 “Liberation Day” calls into question what Trump will do next. Trump has at least five tools he can use to offset the IEEPA tariffs; however, none of them offer the latitude that Trump’s interpretation of IEEPA allowed. Section 338 of Smoot-Hawley, which has never been used, likely has the broadest scope.

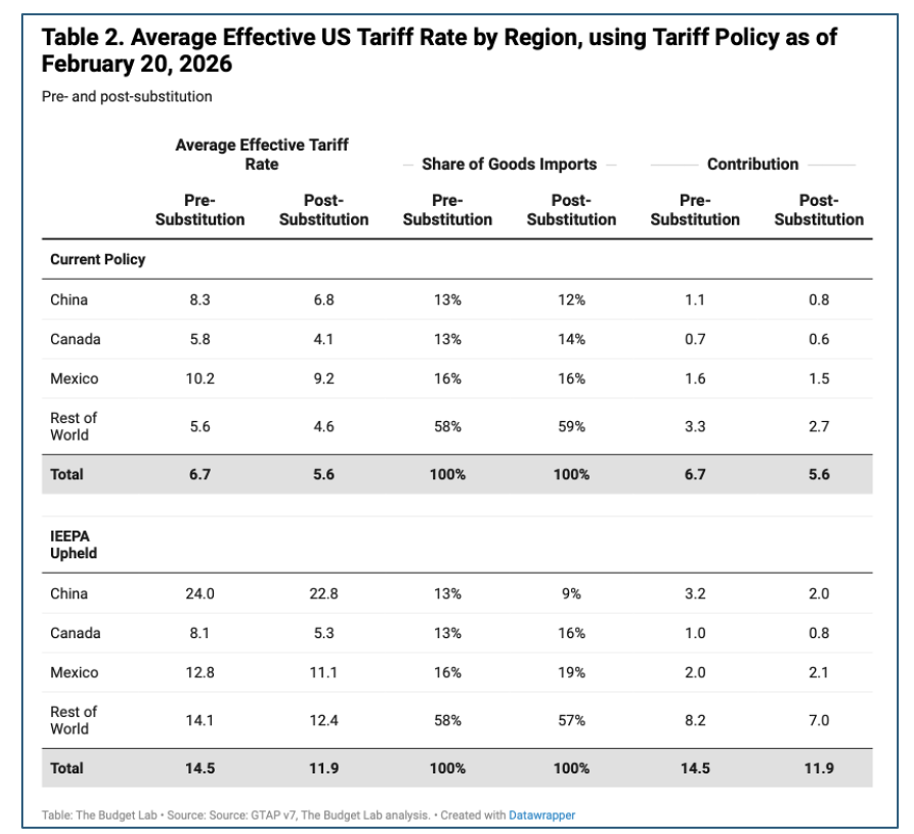

State of U.S. Tariffs: February 20, 2026 Yale University Budget Lab

The Budget Lab estimates the effects of all US tariffs and foreign retaliation implemented in 2025 after the decision by the Supreme Court of the United States that President Trump exceeded his authority to invoke the 1977 International Emergency Economic Powers Act (IEEPA) to impose reciprocal tariffs. Without IEEPA tariffs, consumers will face an overall average effective tariff rate of 9.1%, which remains the highest since 1946 excluding 2025. (If IEEPA tariffs had been allowed to stay in effect, this figure would have been 16.9%.) All tariffs to date as of February 2026 are projected to raise about $1.2 trillion over 2026-35, though slower economic growth reduces revenues and brings the net dynamic revenue to $1 trillion. (With IEEPA, these figures would be more than twice as large.) The economic implications of the SCOTUS decision are complicated by two major factors. First, in the short-term, firms will be aggressively seeking refunds on tariffs paid in 2025, which has large revenue effects and uncertain distributional effects. Second, the current Administration has stated its intent to replace IEEPA tariffs with tariffs using other authorities, but there remain timing and other questions regarding these steps.

Implications of Growing U.S. – Iran Military Tensions

The Day After Khamenei: Iran’s ‘Liberation’ Will Begin as an IRGC Power Struggle Charbel Antoun/National Interest

Many imagine the day after Ali Khamenei as a moment of sudden liberation: Iranians shaking off the mullahs and deciding their own destiny. The likelier opening act is far less romantic. The immediate aftermath will probably look less like a velvet revolution and more like the opening round of an insider power struggle—staged and refereed by the Islamic Revolutionary Guard Corps (IRGC) and its allies. The institutions that have grown strongest under Khamenei are not parliaments, parties, or independent courts, but the security state and its sprawling economic empire. Those are the actors best positioned to inherit the republic he leaves behind.

Iran’s regime is suffering from strategic vertigo. Its next misstep may be its last The Atlantic Council

Tehran appears to be suffering from a case of strategic vertigo. As Iranian leaders continue to see their major decisions backfire over the course of two and a half years, a disorienting dizzy spell may be the best way to describe the state of Iranian foreign policy. Negotiations between the United States and Iran are ongoing, with US President Donald Trump Thursday that he expects a resolution within ten to fifteen days, as he also undertakes a massive military buildup for a possible conflict. The talks provide the regime with a rare opportunity—a gift, even—to escape from yet another predicament. The question right now is whether leaders in Tehran grasp the magnitude of the moment and refrain from their old habits of obstinacy, or whether they will add another strategic error to their string of missteps—one that could be their last. With the United States preparing for strikes if negotiations fail, the question arises of how Iran reached the precipice in the first place.

What War With Iran Would Look Like Arash Reisinezhad/Foreign Policy Magazine

Washington and Tehran may be closer to military confrontation than at any point in memory, but they are not on the brink of war in any conventional sense. The most plausible outcome of the current standoff is not a U.S. invasion of Iran or a full-scale regional war. It is a limited, carefully calibrated strike designed to reshape bargaining dynamics rather than end them.

Iran: What Challenges face the country in 2026? House of Commons Library

In 2025, the US and Israel struck Iran’s nuclear program, the UN reimposed sanctions against the country and its economy continued to struggle. Iran’s regional position also worsened. Established leaders of many Iran-backed armed and proscribed terrorist groups have been eliminated, and their strength weakened in the regional conflict that has been ongoing since 2023. Some Iran-backed groups are facing renewed local and international calls to disarm. This briefing for UK Members of Parliament surveys the situation in Iran, including the challenges facing its government; the status of Iran’s nuclear program and the potential for further strikes in 2026; and pressures on Iran-backed groups in the region.

Iran Oil And Gas Market Size & Share Analysis - Growth Trends and Forecast (2026 - 2031) Mordor Intelligence

According to Mordor’s recent research, Iran’s oil and gas market size in 2026 is estimated at USD 39.18 billion, growing from 2025 value of USD 37.10 billion with 2031 projections showing USD 51.51 billion, growing at 5.62% CAGR over 2026-2031. Robust reserve availability, state-backed capital deployment, and resilient export flows underpin this trajectory even as sanctions pressure persists. The upstream sector anchors revenue, as Iran is the fourth-largest crude producer in OPEC. Meanwhile, the downstream segment is growing faster, with domestic firms adding fluid catalytic cracking and condensate-splitting capacity to increase product yields. Onshore production remains the backbone of the Iranian oil and gas market, but offshore investments at South Pars are accelerating to protect reservoir pressure and sustain natural-gas output. Asset deployment overwhelmingly favors development projects, yet exploration spending is rising because reserve replacement has become a policy imperative. High market concentration persists: The National Iranian Oil Company (NIOC) and its subsidiaries continue to dictate most decisions, although private and quasi-state contractors now win multi-billion-dollar tenders that were once the domain of foreign major oil companies.

Geoeconomics and Global Markets

Could a BRICS Currency Work? Jim O’Neill/ Project Syndicate

O’Neill – who coined the acronym “BRICS” – argues Economists have long dismissed the idea that a BRICS common currency could challenge the US dollar's role in the global economy, and for good reason. But that doesn't mean there couldn't be new common rails for settling trade between countries that want to escape the long arm of the US government.

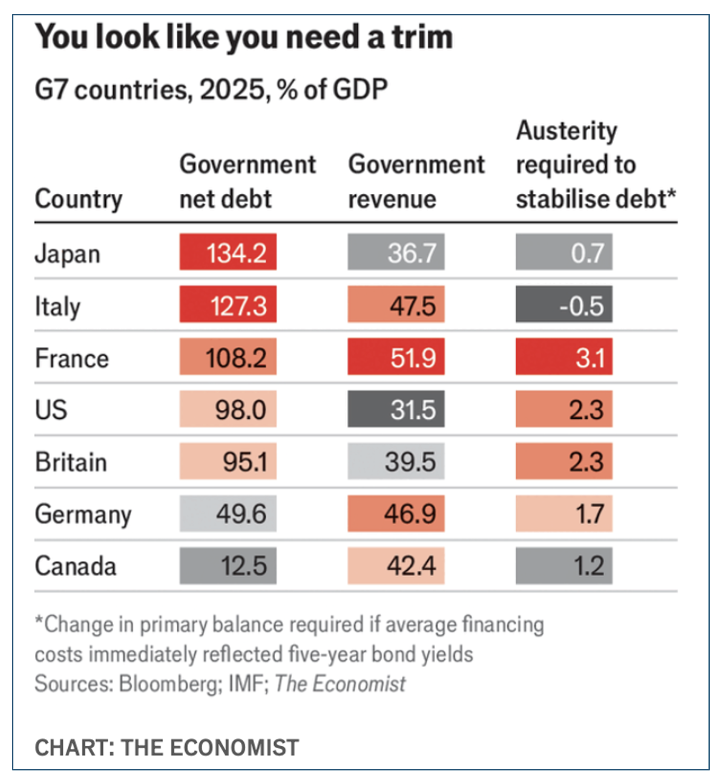

Across The Rich World, Fiscal Crises Loom The Economist

The Economist calculates that most rich countries could still run small primary deficits [deficits net of interest payments] and keep debts stable as a share of their economies, even if they had to refinance all their debt immediately at today’s rates. The largest primary surplus required to balance debts is in Britain, at just 0.3% of GDP. That is not large for countries in a pinch. In the late 1990s Italy ran primary surpluses of 3-6% of GDP to bring down debts before joining the euro. In Britain and America, deficits are large. The belt tightening needed to stabilize the debt-to-GDP ratio exceeds 2% of GDP; in France it is greater than 3% of GDP. Things look worse still when you consider the coming wave of spending on ageing populations, defense and the climate transition. And higher debt interest costs to come are not yet fully accounted for.

Are Government Bonds Safe in Times of War and Pandemic? Zhengyang Jiang, Hanno Lustig, Stijn Van Nieuwerburgh and Mindy Xiaolan National Bureau of Economic Research

Abstract: We analyze real returns on U.S. and U.K. government debt during major wars and the COVID-19 pandemic over the past three centuries. Wars are associated with sharply negative real returns on outstanding government debt, with returns falling far below economic growth, in contrast to peacetime periods when returns exceed growth. Elevated surprise inflation and financial repression account for a cumulative 31% wedge between returns and growth over four years of war, implying that bondholders bear a substantial share of wartime fiscal costs. During wartime, government bonds also systematically underperform risky assets.

When Houses Outrun Paychecks: The Lost Decades of Housing Affordability Federal Reserve Bank of St. Louis ON the Economy Blog

Abstract: In this blog post, we analyze how housing affordability has evolved over the past 20 years. For most U.S. counties, the story is remarkably similar: Home values have risen much faster than the incomes of the people living in them. From 2000 to 2024, median per-capita income has grown steadily but modestly, at around 155% in nominal terms. Over the same period, median home prices—when measured carefully and adjusted for local composition—have increased at a much faster pace, at around 207% in nominal terms. This divergence helps explain why younger households struggle to buy their first home, while longtime owners increasingly view housing as their primary source of wealth.