Fulcrum Perspectives

An interactive blog sharing the Fulcrum team's policy updates and analysis.

Recommended Weekend Read

What Impact Will Trump’s Latest Tariffs Have on 60 Targeted Countries? Cuba On the Brink, How DARPA Intends to Build Nuclear Reactors the Size of AA Batteries, and Inside Ukraine’s Kill Zone

July 31 - August 2, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them of interest and useful as well. Have a great weekend.

Assessing the Impact of the Latest US Tariffs

The State of U.S. Tariffs July 24, 2026 John Iselin/Yale University Budget Lab

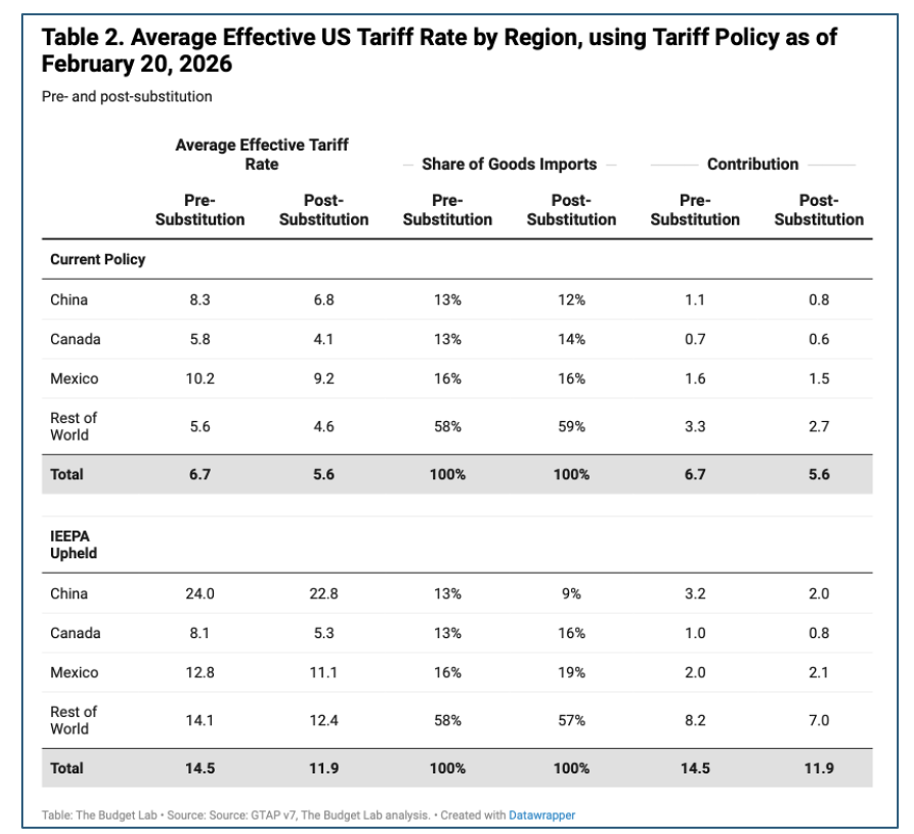

As of July 24th, the average statutory tariff rate stands at 11.1% after falling by about 0.3pp when Section 122 tariffs expired and were replaced with new tariffs under Section 301. Under current law, which includes several scheduled tariff increases in the coming months, this figure is set to be 11.8% by the end of this year. The Yale Budget Lab estimates the ultimate consumer price impact of current-law tariff policy to be about 0.7%. They also estimate household costs due to tariffs total about $1,100 annually under current law. Over the next ten years, the Lab estimates that current-law tariffs will raise about $1.9 trillion. These numbers are somewhat lower, though, after considering the negative impact of tariffs on GDP.

Global Trade Alert’s panopticon on Section 301 forced labor final findings Hinrich Foundation

Global Trade Alert repackaged the USTR’s 24 July final finding on its Section 301 probe on forced labor practices in 60 economies into 60 economy-specific PDFs as a handy trade research tool. New US Section 301 tariffs of 10% or 12.5% took effect on 60 economies for alleged forced-labor practices, with limited exemptions. The Global Trade Alert breaks down how the tariffs were levied based on each economy’s forced-labor import ban regime. USTR’s 431-page notice covers three parts: findings, tariff-schedule Annex I, and 15 exemption lists (Annex II) covering specific products and economies.

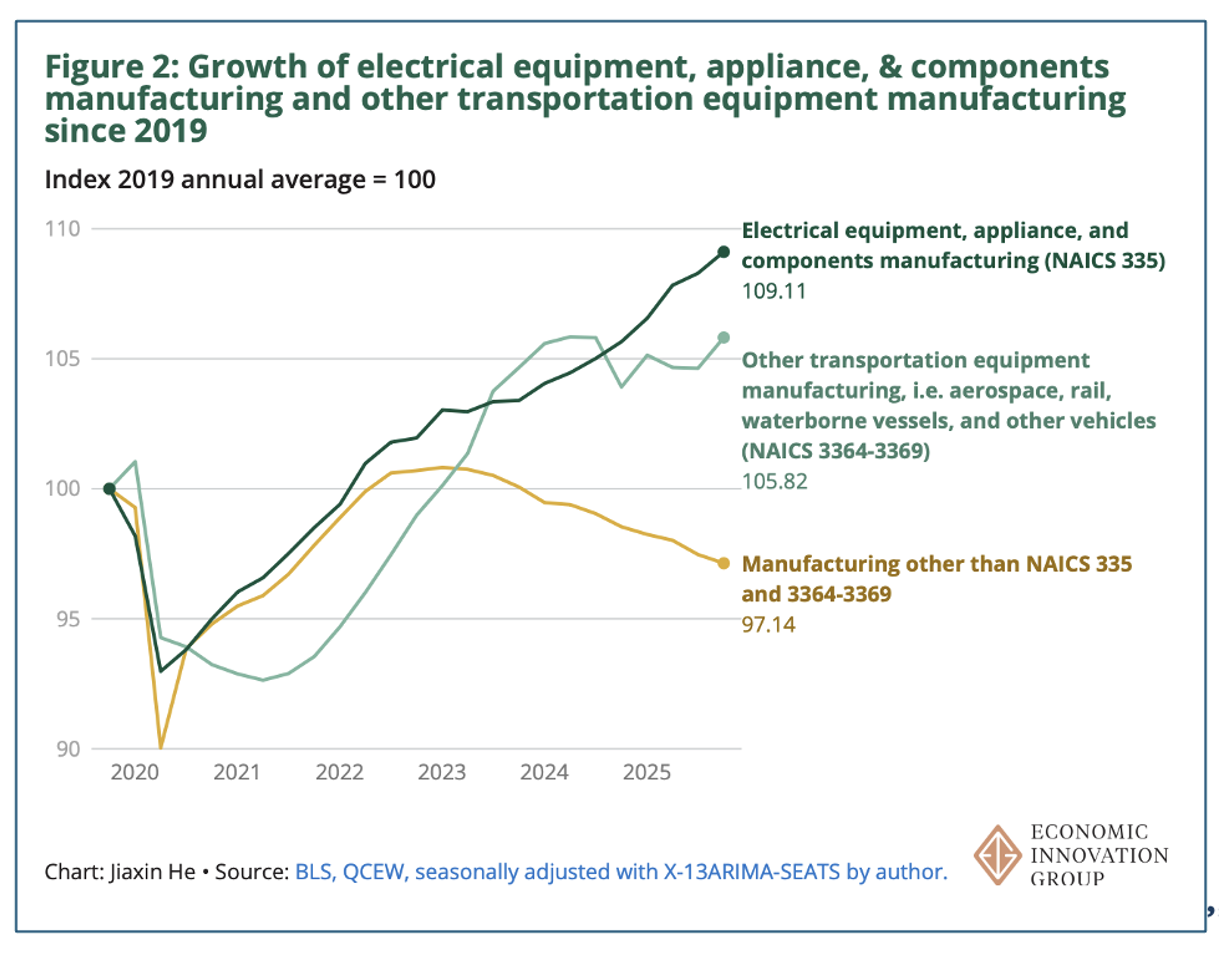

The Big Exceptions to the American Manufacturing Jobs Decline Jiaxin (Jason) He Agglomerations

The Trump Administration’s hope that its tariff policy would increase manufacturing jobs has failed to materialize. Even after a modest uptick in the last three months, the manufacturing sector lost 53,000 jobs in the year through June. It has now shed 300,000 jobs since its post-pandemic peak of 12.9 million in the second quarter of 2023. The short version of what we found is that nearly every manufacturing subsector has lost jobs since the post-COVID peak roughly three years ago. But this study also discovered a few intriguing exceptions, and each of them tells a useful story about recent trends in the U.S. economy. Jobs in two other subsectors - electrical components and transportation equipment - not only have grown since the peak but also have continued their growth throughout 2025. As of the end of last year, electrical components manufacturing employed 9.1 percent more workers than in 2019, while transportation equipment employed 5.8 percent.

Cuba

Cuba: The Capital of 21st Century Communism US State Department

The US State Department, in a new report which ratchets up US-Cuba tensions to a new level, strongly accuses Cuba of waging “a sustained campaign of subversion against the United States. It is a campaign that has infiltrated the highest reaches of the U.S. government, recruited and cultivated generations of American activists, backed an unprecedented wave of left-wing terrorism on American soil, and carried out one of the most durable and damaging foreign intelligence penetrations in American history.” The report goes on to charge, “The Cuban campaign against America is unique. It is irregular and covert – even at the peak of its military power, Havana never possessed the capacity to defeat the United States in a conventional armed conflict. Instead, the Cubans perfected a new model for a long war of attrition, organized around espionage, infiltration, sabotage, proxy networks, and a revolutionary infrastructure designed to turn America against itself. In contrast to every other aspect of Cuba’s failed state, this model has yielded remarkable success.”

Does Cuba Really Have Iranian Drones? Foreign Policy

U.S. President Donald Trump recently said the United States is “looking into” whether Cuba is stockpiling Iranian drones and suggested that Washington could act if that’s the case. National security and Latin America experts told FP that it’s probable that Cuba has such drones, but they also emphasized that it’s extraordinarily unlikely that Havana is planning on taking offensive actions against the United States. The experts also believe that the recent alarm raised over drones in Cuba is part of a broader effort by the Trump administration to establish a pretext for U.S. military action against the island as it works toward the goal of collapsing the government in Havana.

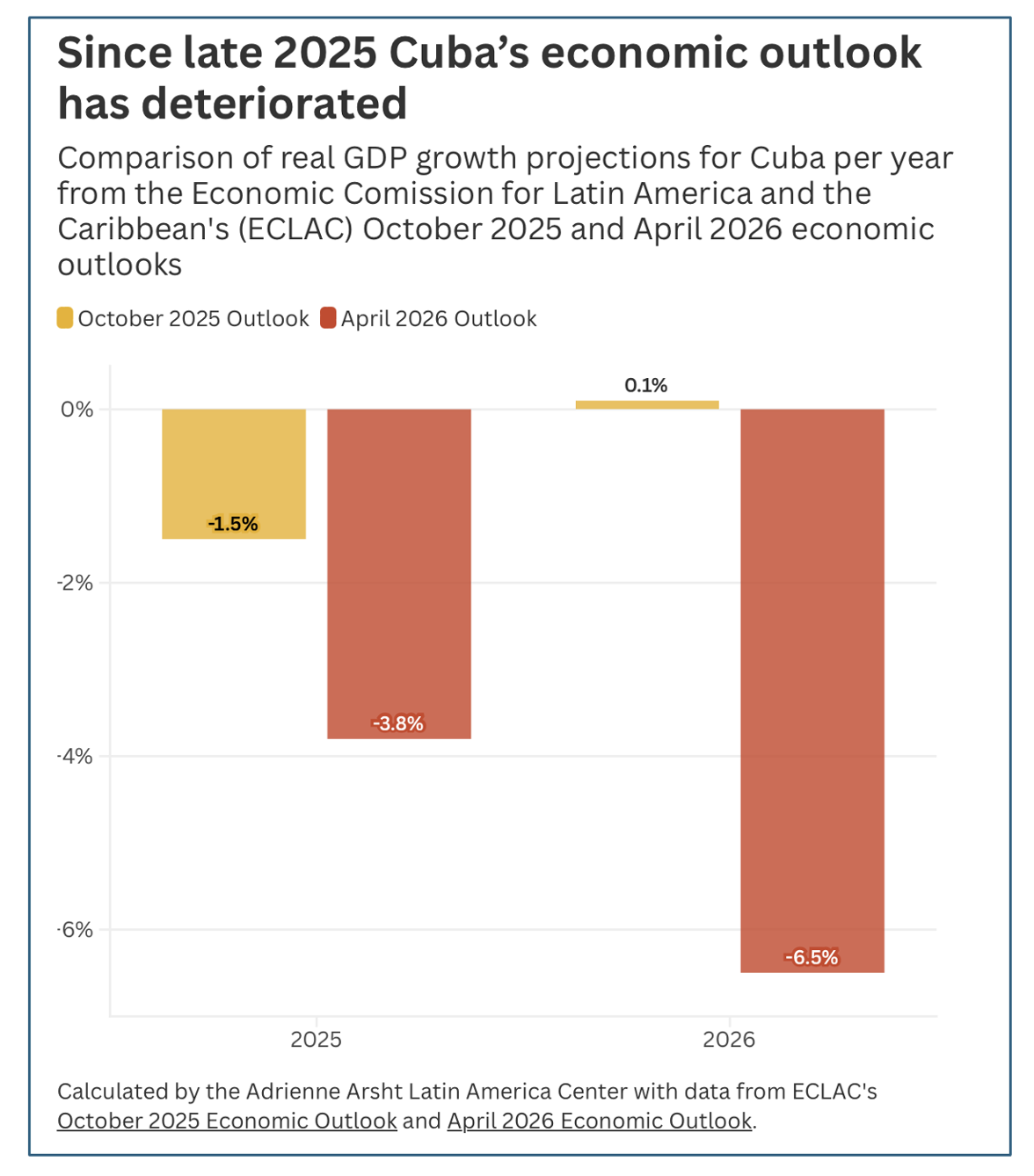

The collapse of Cuba’s state-run economy is years in the making The Atlantic Council

In April, the United Nations Economic Commission for Latin America and the Caribbean (ECLAC) projected that the island’s economy would shrink by 6.5 percent in 2026. This projection is significantly worse than the October 2025 projection of practically zero growth. The pressure is mounting, but the economy’s collapse precedes the recent pressure campaign. Another projection, from the Economist Intelligence Unit, further downgraded the outlook to a 7.2 percent drop in total output for this year. To look at only this data gives an incomplete picture. To begin with, even though ECLAC conducts its own independent assessment, its projections are based on official statistics from the Cuban government, presenting a credibility issue. But even more important, the two-year window is too narrow a snapshot of the Cuban economy’s problems.

Can Cuba Outlast Marco Rubio? Lee Schlenker/Quincy Institute for Responsible Statecraft

Shortly after four members of Congress returned from a fact-finding visit to Havana early last week, Secretary of State Marco Rubio announced a tranche of new sanctions against Cuba’s tourism, energy, trade and security sectors, the latest move in a months-long maximum pressure campaign intended to overthrow the island’s government by year’s end. Nonetheless, all signs indicate that progress in bilateral talks made back in March — when the U.S. “allowed” a Russian fuel tanker to dock in Havana, providing momentary relief for Cuba’s economy — has largely stalled, and other unconventional backchannels have petered out.

Big Strides in Energy Innovation and Drone Warfare

How DARPA plans to get nuclear power in the size of a ‘AA battery’ Breaking Defense

The biggest roadblocks to having transportable nuclear power, according to DARPA program manager Tabitha Dodson, come down to heat and weight. “There’s an enormous amount of energy inside a nuclear reaction, whether it’s fission or radioisotope,” Dodson told Breaking Defense. “[But] there is a lot of heavy and non-transportable hardware that deals with heat management for both fission and RTG [radioisotope thermal generators] systems. That heat management piece is always what drags down all of the dreams of transportable nuclear power.” As a way to bypass that roadblock, DARPA funded seven competing teams as part of its Rads to Watts program to refine a range of approaches to radiovoltaics. The objective of the multi-million-dollar program (full figures weren’t disclosed) is a new kind of miniature power cell that can run anything from satellites in space to tactical radios to pacemakers, tough enough to work for years or decades without recharging and in extreme environments that freeze or try traditional power systems.

Inside Ukraine’s Kill Zone Reuters Graphics

This fascinating, in-depth video/motion report by Reuters is the most detailed reconstruction yet of the new breed of battlefront. It will take you into the kill zone via a “fly-over” that starts 15 km inside Russian-held territory before heading to the contact line between the two sides and then 15 km further into Ukrainian-held land. The war, well into its fifth year, has become the first major conflict to be dominated by unmanned aerial vehicles, with thousands of the cheap but deadly machines filling the skies. Ukraine and invader Russia are constantly advancing the new technology, which is transforming modern warfare. Both sides have had to abandon age-old tactics of gathering troops, vehicles and artillery in a relatively compressed area along the front lines. Such visible targets are easy prey for drones.

Killer Drones: Ready or Not, Here They Come American Enterprise Institute

Lethal autonomy is arriving, regardless of preference or treaty. Shrinking populations and accelerating technology are pushing every military toward increasingly autonomous machines in the kill chain; the live question is whether the US or its adversaries set the bounds. Proliferated precision sensing and strike capabilities create two coupled operational problems: Concentrated forces are now fatally targetable, and the dispersal that addresses this problem depends on dataflows that are themselves an attack surface. Both problems demand uncrewed mass and bounded autonomy to attain scales of force that crewed forces alone cannot reach. The principal barrier is institutional, not technological. The color-of-money structure, Planning, Programming, Budgeting, and Execution cadence, milestone-style test and evaluation approach, and platform-centric sustainment cannot develop capabilities that must iterate continuously—and service cultures resist capabilities that threaten dominant communities.

Recommended Weekend Reads

Crypto and US Household Finance, How Disconnected Youth Spend Their Time, Challenges to the US Industrial Base Policy, and the EU Growing Focus on Geopolitical/Geoeconomic Threats

July 17 - 19, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them of interest and useful as well. Have a great weekend.

Crypto, AI, and Fiscal Policy

Do You Even Crypto, Bro? Cryptocurrencies in Household Finance Federal Reserve Bank of Cleveland

Using repeated large-scale surveys of US households, we study the cryptocurrency investment decisions and motives of households relative to other financial assets. Cryptocurrency holders tend to be young, male, and more libertarian relative to non-crypto holders. Crypto holders expect much higher rates of return for crypto and perceive it as relatively safer than non-holders do. For those holding cryptocurrencies, changes in Bitcoin prices translate into their purchases of durable goods. Finally, information about historical returns of cryptocurrencies in an information provision experiment embedded in the survey leads individuals to increase their desired crypto holdings and increases their actual cryptocurrency purchases subsequently. We compare these views and behaviors to those of households toward other financial assets and argue that cryptocurrency is unique in many of these respects.

How Might Fiscal Policy Respond to the Rise of Artificial Intelligence? Karen Dynan, Douglas Elmendorf, and Louise Sheiner – National Bureau of Economic Research

Abstract: Artificial intelligence will probably generate major changes in the US economy, although the nature, timing, and magnitude of those changes are highly uncertain. We analyze a set of long-term scenarios involving different combinations of faster productivity growth, greater income inequality, job displacement, and a higher capital share of income. For each scenario, we assess the implications for federal debt and potential policy responses related to faster economic growth, the distribution of income, support for workers who are laid off, and taxation and ownership of capital. Given the uncertainty surrounding AI’s economic effects, policies that are robust to different scenarios would be especially valuable.

Economic Well-Being of U.S. Households in 2025 Federal Reserve Board Research and Analysis

A recent Federal Reserve Board research piece shows that 49% of U.S. adults under 30 lived with a parent in 2025, up 12 percentage points since 2019, while 33% of adults lived in households with at least two generations of adults. Specifically, 19% of adults lived with their adult children (age 18 or older), and 15% lived with a parent. Two percent of adults simultaneously lived with a parent and an adult child. The share of young adults who live with their parents has increased in recent years. In 2025, 49% of adults under age 30 lived with a parent. This share was up by 6 percentage points since 2022, and up 12 percentage points since 2019, just before the pandemic. Conversely, adults aged 60 and older were more likely to live alone than were younger adults. Overall, 13% of people lived alone in 2025. Among those ages 60 and older, a higher 20% were living alone.

How Are “Disconnected” Young Adults Spending Their Time? Federal Reserve Bank of St. Louis

In 2024, the share of U.S. 18- to 24-year-olds who were neither employed nor enrolled in school—that is, “disconnected”—was measured at 16%. That share remained essentially unchanged as of December 2025, despite a generally healthy labor market overall. Rural young adults, less-educated young adults, young Black adults, and young adults from lower-income families tended to have higher rates of disconnection than their peers. The American Time Use Survey offers a nuanced view of how disconnected young adults spend their time, suggesting constraints on the way their time can be allocated rather than disengagement or inactivity. Disconnected young adults spend more time on caregiving responsibilities and household activities than their not-disconnected peers, and less time on work- and education-related activities. Patterns in social and leisure time are similar across both groups.

The AI Investment Race Phurichai Rungcharoenkitkul - Bank of International Settlements

AI infrastructure investment is expanding faster than any previous technology boom, including the railway mania and dotcom bubble, within just three years. Debt-fueled buildout and circular financing arrangements are creating financial interconnectedness that makes the current cycle more fragile and prone to sharp correction. The analysis warns, “Their model suggests that investment is 50% above the efficient level.” This fragility is further aggravated by the leverage that accompanies the rapid ramp-up of investment. This boom-bust pattern recurs across history, from the US canal mania in the 1830s and the British railway mania in the 1840s to the roaring 20s and the dotcom boom in the late 90s. These episodes all ended in sharp corrections with wider economic fallout.

The EU’s Global Threat Analysis & The Challenges to US Industrial Base Policy

Common Understanding – The Threats and Challenges We Face: Assessment of the EU’s Strategic Environment Council of the European Union

A new EU report argues The EU faces an uncertain geostrategic context driven by sustained, simultaneous threats on multiple fronts – but singles out China and Russia of trying to “reshape the global order in line with their interests” and “fostering a return to a sphere-of-influence logic.”

The Coming Clash Between China and Europe Thorsten Benner/Foreign Affairs

In 2025, Chinese leader Xi Jinping tried to capitalize on U.S. belligerence toward Europe by promoting China as the responsible great-power alternative. In a message sent to mark the 50th anniversary of diplomatic relations between China and the European Union, Xi invited Brussels to join forces with Beijing, to “uphold multilateralism, safeguard fairness and justice,” and “oppose unilateralism and bullying.” Key EU leaders, as well as the Brussels bureaucracy, are not buying it. They have concluded that the very survival of Europe’s core industries is threatened by China. Increasingly, European leaders are arguing that the EU needs to take action to protect its industries. So severe is the threat that measures that were unthinkable a few years ago are now gaining momentum. An all-out trade war with China is becoming a real possibility.

Europe must really confront China now: delay is no longer an option Steven Everts/European Union Institute for Security Studies

Europe urgently needs a serious debate on China. Not a technical discussion about tariffs, subsidies, or market access, but a strategic one. After all, China affects everything at once: industrial policy, defense, technology, critical raw materials, and trade. This is geopolitics, and therefore a top priority. The challenge is becoming more urgent. Pressure is growing in sector after sector. Electric cars, batteries, solar panels, wind turbines, pharmaceuticals, chemicals – European companies are feeling the rise of Chinese competition everywhere. Behind this lies an economic model in which state aid, cheap financing, export promotion, and strategic market access are closely intertwined. At the same time, it is becoming increasingly difficult for European companies to operate in China itself under fair conditions.

Is the Industrial Base on a Wartime Footing? A Progress Report Jerry McGinn and A.J. Dilts - Center for Strategic and International Studies

Roughly 10,000 new firms have entered the market in the past two years and nontraditional companies received over $120 billion in contract obligations in FY 2025, adding competition and innovation to the sector. Munitions contract obligations have risen 330% since FY 2010. Spurred by this increased demand and depleted inventories, the Pentagon is signing multiyear agreements with munitions producers and suppliers on a historic scale. In addition to developing magazine depth, the DOD is prioritizing magazine breadth, placing an increased emphasis on equipping the Joint Force with a “high-low mix” of both exquisite and affordable missiles and interceptors. Stockpiles require resilient supplies of subcomponents, and new firms and forms of government-industry collaboration are reshaping the solid rocket motor (SRM) sub-sector. At the bedrock of defense supply chains, unprecedented commitments of public and private capital are focused on establishing a secure mine-to-magnet rare earth supply chain outside Chinese control.

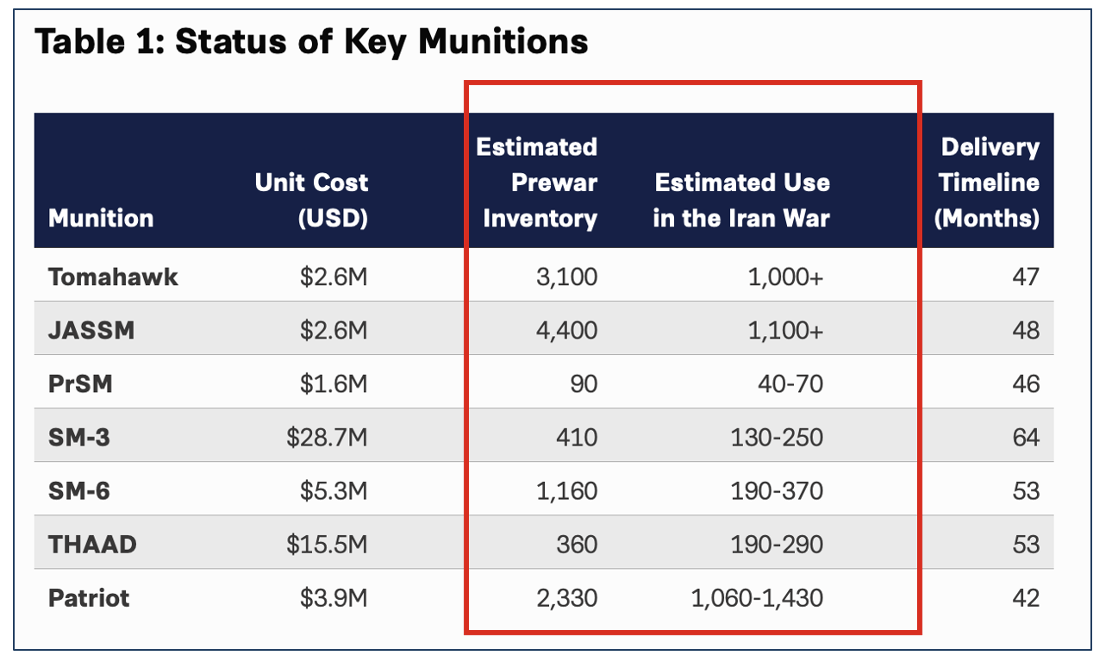

Scaling Patriot Production: The Industrial Base Crisis Explained Foreign Policy Research Institute

On April 10th this year, after coalition forces had fired at least 1,700 Patriots in just five weeks, the Pentagon announced $4.76 billion contract to accelerate production. While a seemingly forceful response, the move only highlighted the core problem. At the current build rate of 600 missiles per year, it would take three years to replace what was used in a little over a month. Replenishment runs on an industrial clock, and that clock is measured in years, not days. Patriot missile expenditure by the United States and its allies in the 2026 Iran War is the clearest case study in command of the reload. The problem is not simply how to fire more missiles, but how to sustain missile defense once the opening magazine is gone. That requires three things:

Buying time through multiyear demand that gives industry room to invest;

Buying redundancy across the sub-tier bottlenecks that pace production

Buying efficiency through defensive doctrines that preserve premium interceptors for premium threats.

For decades, US grand strategy was what Barry Posen famously called “Command of the Commons,” the ability to dominate every war-fighting domain to shape the terms of a conflict. That advantage still matters, but the Iran war exposed the harder foundation beneath it. The United States can expend advanced precision-guided munitions in weeks, while the defense-industrial base takes years to replace them. Command of the commons now depends more heavily on “Command of the Reload.”

Recommended Weekend Reads

Foreign Private Capital Overtook Central Banks in the Treasury Market, U.S. Grand Strategy and China, and How a Quiet US – AU Deal Could Reshape Investment in Africa

April 24 - 26, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them of interest and useful as well. Have a great weekend.

Geoeconomics, Financial Markets, and AI

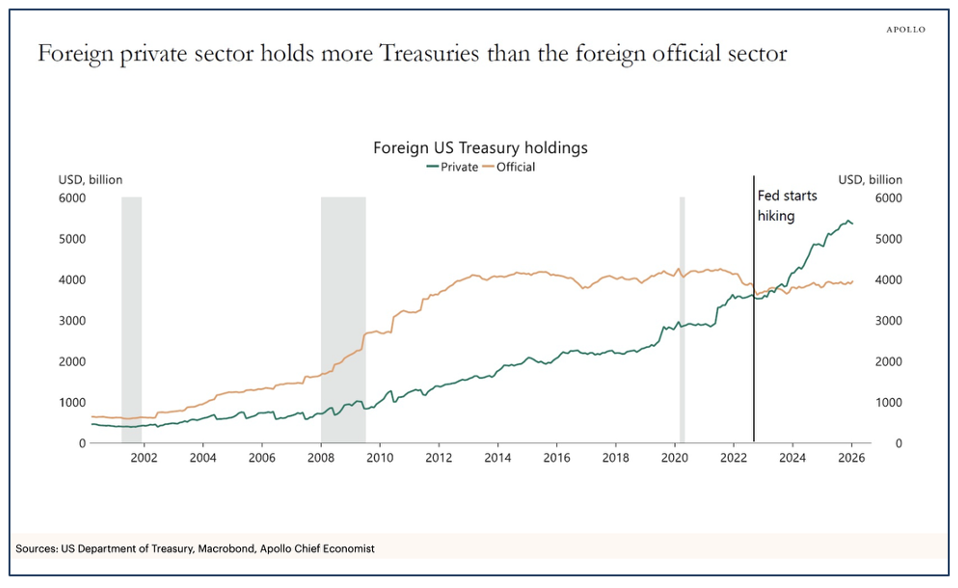

Foreign Private Capital Has Overtaken Central Banks in the Treasury Market Torsten Sløk Apollo

For the first time, foreign private buyers own more Treasuries than the foreign official sector, Slok notes, suggesting the “Treasury market [may be] increasingly sensitive to the return expectations of price-sensitive private capital.”

Corporations in the Crosshairs: Commercial Actors, Conflict Escalation, and Crisis Simulation Journal of Simulation and Gaming

Abstract: The authors reach three substantive findings. First, the game demonstrated that cyber and kinetic attacks on commercial assets can trigger escalation—challenging arguments that attacks on commercial targets are less provocative than attacks on military and government targets. Second, the growing role of commercial firms in the international security arena makes communication channels for information sharing and coordination between the government and these firms critical for crisis management. Third, the wargame highlighted how relying on influential private sector leaders involves tradeoffs. These individuals can provide critical information to governments, leverage their companies to support government efforts, and help coordinate broader private sector engagement. However, they may also prioritize their own commercial interests over national ones. Additionally, the simulation revealed lessons that may assist designers of future simulations involving commercial actors.

Drivers of Population Growth: Natural Increase vs. Net Migration Federal Reserve Bank of St. Louis

National population growth reflects both natural increase and net migration, with each factor shaping countries differently across income levels. Natural increase drove almost all population growth in poor countries from 1960 to 2023. In rich countries, however, both natural increase and net migration sustained their population growth during that same period.

Six Reasons Claude Mythos Is an Inflection Point for AI—and Global Security Council on Foreign Relations

Anthropic’s new AI model has taught itself to hack into software infrastructure systems believed to be among the most secure in history. While there is no question that the technology is profoundly dangerous, it is unclear if defenders will win a race against time to protect a sea of vulnerable targets.

Forecasting the Economic Effects of AI National Bureau of Economic Research

Abstract: We elicit forecasts of how AI will affect the U.S. economy, comparing the beliefs of five groups: academic economists, employees at AI companies, policy researchers focused on AI, highly accurate forecasters, and the general public. The median respondent in each group expects substantial advances in AI capabilities by 2030, small declines in labor force participation consistent with demographic shifts, and an annual GDP growth rate of 2.5%, which exceeds both the typical medium-run (2.0%) and long-run (1.7%) baseline forecasts from government agencies and private-sector forecasters. Conditional on a “rapid” AI progress scenario, in which AI systems surpass human performance on many cognitive and physical tasks, experts forecast substantial, though not historically unprecedented, economic shifts: annualized GDP growth rising to around 4% and the labor force participation rate falling from its current level of 62% to 55% by 2050, with roughly half of that decline—equivalent to around 10 million lost jobs—attributable to AI. A variance decomposition suggests that expert disagreement about these effects is driven primarily by different beliefs about the economic effects of highly capable AI systems rather than by disagreement about the pace of AI progress. These forecasts map onto notably different policy preferences across groups: experts strongly favor targeted measures such as worker retraining, whereas the general public supports both targeted programs and broader interventions, including a job guarantee and universal basic income.

·Construction Costs Rarely Fall Brian Potter Construction Physics

Multiple measures show real construction costs have “virtually never fallen” since 1875, with the striking exception of 1975–95—consistent with input cost and productivity series. The upward drift is not new; if anything, it has moderated over time

Africa

A quiet US-AU deal that could reshape investment in Africa Africa Futures/AUDA NEPAD

The Trump administration and the AU have started a bold journey that could ‘flip the script’ on decades of development cooperation. The Strategic Infrastructure and Investment Working Group (SIWG), formed on 28 January 2026, will enable senior officials and experts to identify investment opportunities, particularly involving the US private sector. It could strengthen African and US strategic options amid major-power rivalries globally. But both sides must ensure Africans’ full partnership as investors and decision makers in those projects.

The Sudan War in 10 Charts The Center for Strategic and International Studies

Sudan’s civil war has now entered its fourth year, with its two main factions locked in a grinding war of attrition. The conflict began on April 15, 2023, between the Sudanese Armed Forces (SAF) led by General Abdel Fattah al-Burhan, and the Rapid Support Forces (RSF) paramilitary, led by Mohamed Hamdan Dagalo, popularly known as Hemedti. Today, the country is split roughly in two, with the SAF in control of the east and the RSF in control of the west. As a result of the war, Sudan is now the world’s largest displacement and hunger crisis. Rape and sexual violence are both widespread and systematic and have become a defining feature of the war. Sudan’s rich cultural heritage, too, is being erased.

Impact of the Iran War

The Iran War Is a Stress Test for Gulf States Carnegie Endowment for International Peace

The U.S.-Israeli war on Iran has had dire security and economic consequences for the Arab states of the Gulf Cooperation Council (GCC). Iranian missiles and drones struck airports, hotels, and energy infrastructure across the region, triggering the largest oil supply shock in the history of global energy markets and a near-total collapse of aviation and tourism. Attacks on desalination plants have raised fears of a humanitarian emergency. Threats to shipping through the Strait of Hormuz have disrupted over 70 percent of the region’s food imports. Externally, the war has prompted questions about the risks and costs of the region’s reliance on American security guarantees and bases. Beyond these effects, the Iran war is a stress test for domestic governance and social cohesion inside Gulf states, surfacing and sharpening preexisting fissures and vulnerabilities while introducing new pressures. Among the more prominent of these dynamics are a worsening crackdown on freedom of expression and increased securitization more broadly; a rise in sectarian tensions and internal scapegoating amid the very real threat of Iranian subversion; and the imperilment of the Gulf’s migrant labor communities, upon which much of the region’s prosperity relies. None of these shocks poses a serious challenge to stability or the survival of the region’s monarchies—Gulf regimes are hardly brittle and have weathered such shocks in the past.

The Strait of Hormuz in 8 Charts Center for Strategic and International Studies

CSIS has put together a superb interactive, moving set of charts showing what is happening – and not happening – in the Strait. Overall, access to the Strait of Hormuz, which carries roughly a quarter of global oil flows, remains contested. The waterway has been effectively closed since March 2, following U.S. and Israeli strikes on Iran. Although Tehran declared the strait open on April 17, the Islamic Revolutionary Guard Corps reversed course and announced it shut just one day later. The United States has since moved to enforce its own presence, including by seizing an Iranian-flagged cargo vessel on April 19. Vessel tracking and maritime trade data offer key insights into the ongoing dispute.

Last Rounds? Status of Munitions at the Iran War Ceasefire The Center for Strategic and international Studies

Concern about the status of U.S. munitions inventories has intensified as reports emerge about high expenditures of Tomahawks, Patriots, and other missiles in the Iran war. As Operation Epic Fury remains paused in a shaky ceasefire, there is an opportunity to assess whether the U.S. military nears the point of going “Winchester”—or running out of ammunition. Analysis of seven key munitions shows that the United States has enough missiles to continue fighting this war under any plausible scenario. The risk—which will persist for many years—lies in future wars.

Strategy Going Forward from the U.S. And German Perspectives

US Grand Strategy and the China Factor with Nadia Schadlow China Considered Podcast

Dr. Elizabeth Economy sits down with Nadia Schadlow, former deputy national security advisor for strategy in the first Trump administration and author of the influential 2017 National Security Strategy (NSS). Schadlow reflects on how the NSS was architected around the shift toward great power competition and America's four core national security interests: protecting the homeland and way of life; promoting American prosperity; preserving peace through strength; and advancing American influence. The conversation moves through key differences between the first and second Trump administrations, including process, tone, and the role of ideology in foreign policy, before turning to a substantive debate about the limits of multilateral institutions and Schadlow's argument in a recent Foreign Affairs essay that state-centric approaches can outperform global governance frameworks. Economy and Schadlow also assess the strategic landscape ahead of a potential Trump-Xi summit, discussing where US leverage is real, where it may be overstated, and whether tariffs alone can move China's economic model. They close with a shared critique: that the United States has consistently failed to develop a coherent, assertive diplomatic and development strategy to compete with China's Belt and Road Initiative.

A Grand Strategy of Consolidation: How Trump Can Revitalize American PowerA. Wess Mitchell/ Foreign Affairs

For three and a half decades, it has maintained peace and sustained influence in all the world’s major regions without difficult tradeoffs. It continued to assume it can do so even as the country’s relative economic strength decreased, and rival military buildups eroded its superiority. As a consequence, the United States now faces a serious misalignment between its national power and the strategic objectives to which it has become accustomed.

The Return of Power Politics to the Market: Theory and Practice of the Geoeconomic Zeitenwende The Stiftung Wissenschaft und Politik/German Institute for International and Security Affairs

The return of power politics to the market is a defining feature of the geoeconomic Zeitenwende, as is currently being experienced in international politics. This has brought renewed attention to the long-standing conventional wisdom that economic activity can not only generate prosperity but also promote foreign and security policy objectives. The analysis and strategy of foreign, security, and economic policy require a clear conceptualization of the term “geoeconomics”. This is necessary not least to weigh the costs and benefits of geoeconomic measures in a well-founded manner, and to assess their prospects for success more realistically. The contributions to this research paper focus on the theoretical and conceptual foundations of geoeconomic thought and examine selected empirical case studies of geoeconomic action in functionally defined policy areas. In order for German geoeconomic policy to become more effective and coherent, the following approaches are recommended: first, the establishment of interagency structures for the cross-cutting task of geoeconomics; second, the expansion of communication and coordination with relevant stakeholders from the business sector and academia; and third, the strengthening of international cooperation with like-minded partners.

Recommended Weekend Reads

Focus on Cuba, Venezuela, and Peru, Iran, and A Look at The Global Implications of the War, and China Cracks Down on “Bone-Ash” Burials in Empty Apartments

April 10 - 12, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them of interest and useful as well. Have a great weekend.

The Americas: Focus on Venezuela, Cuba, and Peru

Preparing for the Consequences of Collapse in Cuba Christopher Hernandez-Roy & Team/Center for Strategic and International Studies

Much has been written on what comes next for Cuba—in terms of U.S. pressure, regime change or regime management, and who might be Cuba’s “Delcy”—with less focus on the impact that U.S. policy is having on the people of Cuba, who already faced a dire humanitarian situation created by their leaders. What consequences would stem from a sudden collapse of the regime, and what should the United States and the international community be doing to prepare for this eventuality?

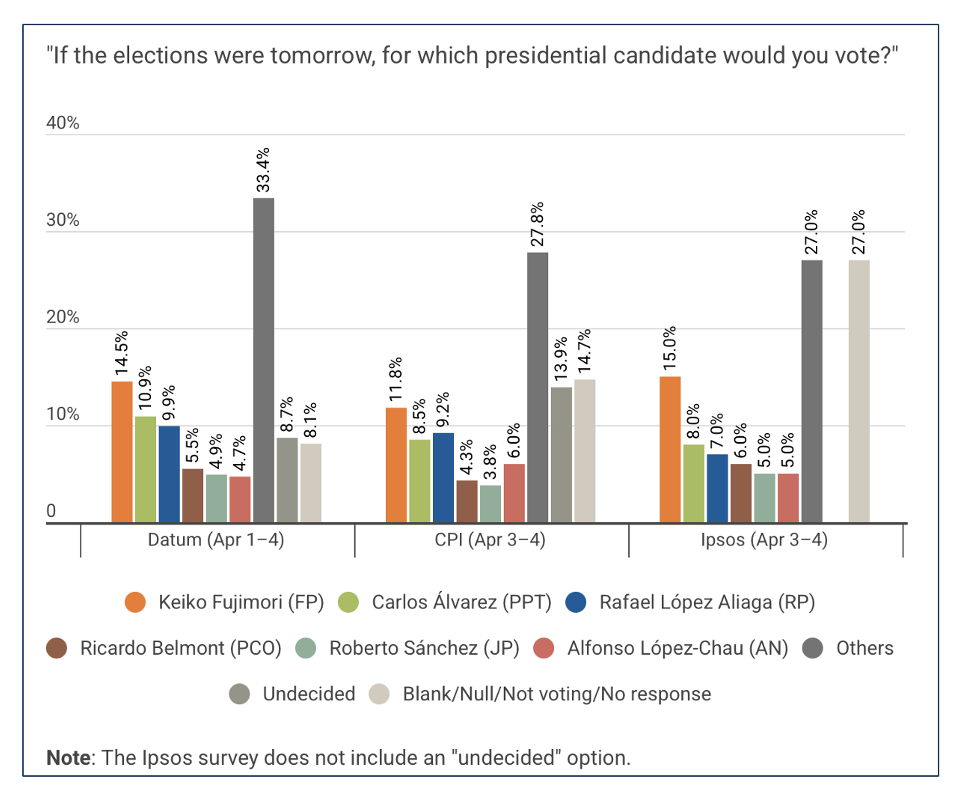

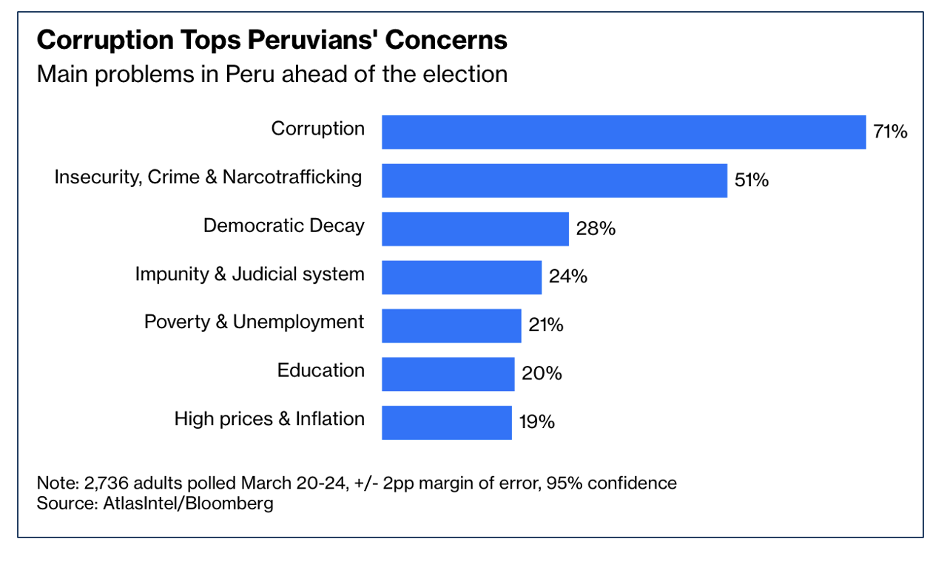

Peru: Meet the Candidates 2026 Americas Quarterly

A record 36 candidates are now vying for the presidency, crowding the field and reflecting the country’s fragmented political landscape. If no candidate wins more than 50% of the vote on April 12, the top two will advance to a June 7 runoff. All seats in Congress are also up for election in the high-stakes April 12 contest. For the first time in decades, the country will vote to choose a Senate, the result of a 2024 electoral reform that reinstituted a bicameral system and reversed a ban on consecutive terms for legislators. All winners will be elected to a five-year term. For this analysis, AQ has included only candidates polling above 6% in recent IPSOS surveys, listed in alphabetical order by last name, and has asked eight nonpartisan experts on Peru to help us identify where each candidate stands on two spectrums: left versus right on economic matters, and personalistic versus institutionalist on leadership style.

Poll Tracker: Peru’s 2026 Presidential Election Americas Society/Council of the Americas

The AS/COA has been closely monitoring the upcoming Peru elections. Via this link you can dive into the details of voter polling in advance of the election and post-election analysis.

Peru’s Dysfunctional Politics Are an Economic Time Bomb Bloomberg

Peru has had three presidents since October, yet markets have largely remained unaffected, with country risk and credit default swaps only marginally increasing. The economy continues to expand, with exports hitting records and inflation remaining low, despite the political turmoil and a fuel-price shock in March. The upcoming general election may not resolve the country’s political instability, and the next government will likely face challenges in addressing corruption, insecurity, and geopolitical pressures.

Venezuela’s Treacherous Recovery: The Peril and Promise of an Economic Boom Moisés Naím/Foreign Affairs

Venezuela may soon experience something it has not seen in years: a surge of economic growth and activity. Although the removal of President Nicolás Maduro by U.S. forces in January left his deputy, Delcy Rodríguez, in place, it has nonetheless opened possibilities that for decades seemed out of reach. Political prisoners are slowly being released, exiles are considering returning home, investors are exploring new opportunities, and countries are reopening their embassies in Caracas. Venezuelans’ long-suppressed hopes are flaring back to life. However, many Venezuelans have great expectations for what the future might hold. Should the state fail to deliver, it could plunge the country into chronic political instability. The only way to guarantee that an economic recovery serves all Venezuelans is to also ensure a political recovery, one in which institutions can once again constrain executive power and in which the will of the public finally finds expression in elections that are genuinely free and fair.

Venezuela Seems to Be Going … Well? Missy Ryan/The Atlantic

Three months after U.S. troops snatched Nicolás Maduro and brought him to New York, life in Venezuela has returned to normal, whatever normal is in a nation that has been gripped by turmoil and economic calamity for years. Government services and the bleak economic conditions that Venezuelans have been living under haven’t improved much, but there is a sense of optimism that Maduro’s departure brings the possibility of better days. Oil revenue is increasing. And Washington’s handpicked interim authorities, led by Maduro’s vice president, Delcy Rodríguez, have rolled out a succession of investor-friendly measures devised by their new North American patrons. A recent pollappears to bear this out. The survey, from Atlas Intel and Bloomberg, shows that nearly 80 percent of Venezuelans think their country is the same or better off now than under Maduro; 54 percent said that greater U.S. influence is positive; 52 percent say that the country’s civil liberties have increased. Trump could only wish for such favorable numbers at home.

What Happens Next with Iran and The Possible Implications of the War For the Rest of the World

The Iran War’s Real Lessons for China: U.S. Tactical Successes Should Give Beijing PauseForeign Affairs

The performance should give pause to U.S. adversaries that have been watching the war in Iran unfold. Massive volleys of long-range drones and ballistic missiles are a preferred offensive tool of China, North Korea, and Russia, used to pound military bases and headquarters, sink fleets, and level civilian infrastructure. If a U.S. adversary were to undertake a war of aggression in Asia or Europe,its plan would be to launch strikes to try to neutralize U.S. and allied military forces, likely inflicting high civilian losses in the process, and then use that cover to carry out its war objectives. The success of high-end Western missile defenses against Iranian strikes calls such a plan into question. Ballistic missiles and drones may not be the decisive offensive weapons that many countries thought them to be. They could still be effective in a campaign of attrition and coercion—but this would be a slow process, not a path to quick victory.

The war on Iran: Nobody won, everyone paid Mahjoob Zweiri/Al Jazeera

Yet before the architecture of this agreement is examined, it is worth pausing to assess the conflict itself: its origins, its legal standing, and who ultimately absorbed its costs. he US-Israeli campaign has failed to achieve its goals. Iran has been badly hit, and the Gulf is paying the bill too.

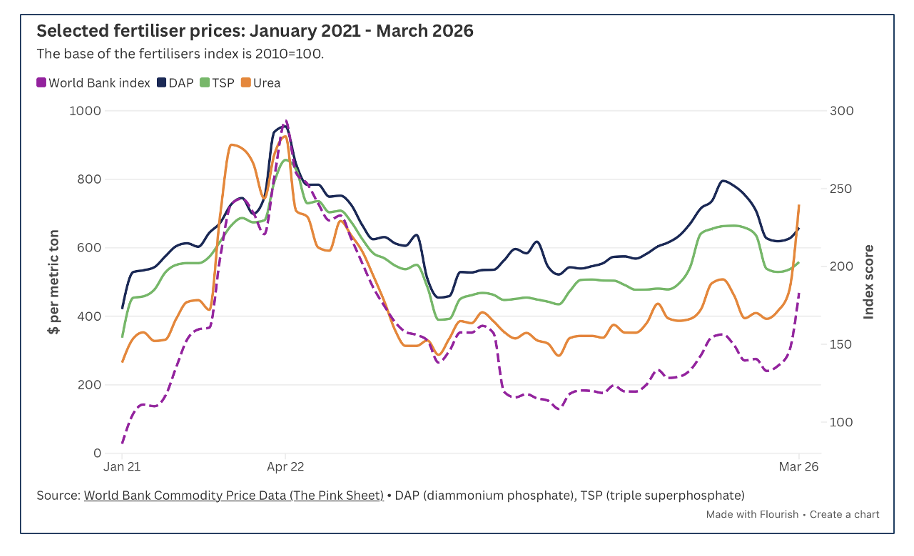

Hormuz Exposes Africa’s Fertilizer Structural Risk African Futures Blog

For Africa, the recent tensions in the Middle East are exposing an already known, deeper dependency. The continent’s agricultural systems largely rely on fertilizer supply chains shaped by external production hubs, energy markets and geopolitical risk. In addition to rising costs of direct agricultural input, disruptions in fertilizer supply chains can quickly affect food prices and availability, as many African countries have high import volumes and bills for foodstuffs. Domestic fertilizer production in Africa remains uneven and insufficient to meet the growing demand, with many countries depending heavily on imports to sustain agricultural output. Production capacity exists in parts of North and West Africa, driven by massive phosphate deposits and natural gas reserves. Morocco leads in phosphates, accounting for over 50% of Africa’s supply, and ranks among the top five global phosphate fertilizer exporters, while Nigeria, Egypt and Algeria dominate in nitrogenous (urea) fertilizer production.

Geoeconomics, Demographics, and Tech

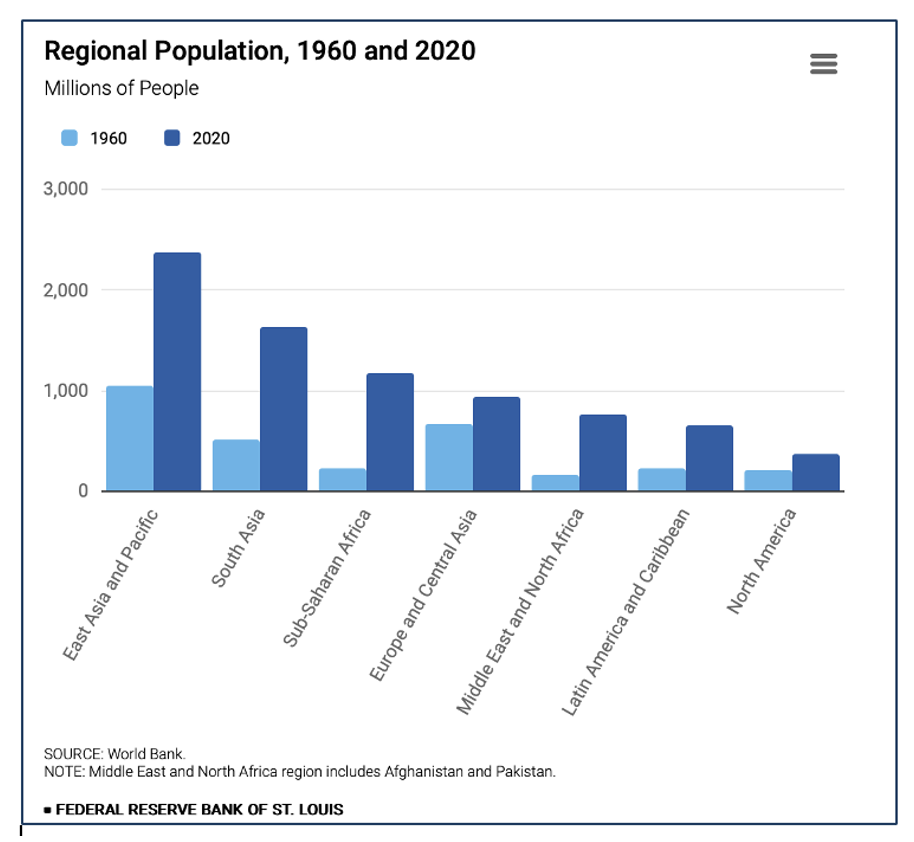

How Regions Shaped World Population Growth since 1960 Federal Reserve Bank of St. Louis

World population has increased from approximately 3 billion in 1960 to almost 8 billion in 2020. While global population growth is significant, some countries are concerned about declining population trends within their borders. This blog post documents population shifts across various geographic regions. While North American population increased from 199 million to 370 million, South Asian population increased from 508 million to 1.6 billion and sub-Saharan African population increased from 228 million to almost 1.2 billion.

China Cracks Down On ‘Bone Ash’ Burials In Empty Apartments Financial Times

Chinese funeral expenses were 45% of the mean annual wage in 2020. As real estate prices declined, many families started using empty apartments as “bone ash apartments.” The practice was formally outlawed two weeks ago. Rapid urbanization has raised demand for limited cemetery plots in cities. Coupled with this, China’s population is ageing at one of the fastest paces in history. The number of deaths in 2025 was 11.3mn, up from 9.8mn in 2015 and outpacing 7.9mn births last year. In contrast to apartments, whose prices have fallen sharply since President Xi Jinping’s campaign that “properties are for living in, not for speculation,” cemetery plots have become prohibitively expensive. A global funeral expense survey in 2020 by the insurer SunLife showed that China’s average funeral expenses were the second highest in the world at about Rmb 37,375 ($5,400), after Japan, accounting for about 45% of average annual wages. While residential properties in China carry 70-year usage rights from the government, cemetery plots come with only a 20-year lease.

Space for the Departed: Land Scarcity and Bone-Ash Apartments in ChinaXinyi Wu/Pitzer College, Claremont Graduate University

Abstract:The rise of bone ash apartments in China reflects a layered response to urban land scarcity, shifting funeral policies, and real estate speculation. As the state mandates cremation and restricts private cemetery development, traditional burial customs are increasingly reshaped by spatial limitations, economic pressures, and political regulation. For some families, bone ash apartments function as modern ancestral halls—domestic spaces for remembrance and ritual continuity. For others, they represent a pragmatic investment strategy, offering long-term storage of ashes within assets that retain market value. This thesis examines how urban planning, state funeral policy, real estate dynamics, and the disintegration of neighborhood relationships collectively give rise to this phenomenon. Rather than interpreting bone ash apartments as merely a cultural departure or financial tactic, the study argues that they embody a complex convergence of spatial constraint, ritual transformation, political governance, and socio-economic adaptation within the conditions of contemporary urban China.

Private Credit Markets Theory, Evidence, and Emerging Frontiers Jiacheng Zou/Cornell University

Abstract: Private credit assets under management grew from $158 billion in 2010 to nearly $2 trillion globally by mid-2024, fundamentally reshaping corporate credit markets. This paper provides a systematic survey of the academic literature on private credit, organizing theory and evidence around four questions: why the market has grown so rapidly, how direct lender technology differs from bank lending, what risk-adjusted returns investors earn, and whether the sector poses systemic risks.

The payment system puts a floor on the Fed’s balance sheet The Brookings Institute

If the Federal Reserve wants to shrink its massive balance sheet—as President Trump’s nominee to be the next Fed Chair, Kevin Warsh, advocates—it must find ways to reduce the demand by banks for reserve deposits at the Fed or risk severe disruptions to money markets. On the asset side of its balance sheet ($6.6 trillion in mid-March), the Fed holds mainly Treasury securities and government-guaranteed mortgage-backed securities. The Fed’s largest liability is in the form of reserve balances, currently totaling about $3 trillion. These are deposits held at the Fed by banks. The Fed controls short-term interest rates primarily through the interest rate it pays on those balances.

Recommended Weekend Reads

Looking at How the Iran War is Impacting the Rest of the World, Will a Tax on Billionaires Have the Desired Effect? and Why Brazil’s Lula is Struggling Ahead of the October Elections

March 13 - 15, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them of interest and useful as well. Have a great weekend.

The Growing Global Impact of the US-Israel- Iran War

The Other Global Crisis Stemming from the Strait of Hormuz’s Blockage Carnegie Endowment

The Gulf region is a key producer not only of liquified natural gas (LNG) and oil products but also of fertilizer. About one-third of global seaborne trade in fertilizers typically passes through the Strait of Hormuz, which has been nearly entirely closed since the United States and Israel attacked Iran on February 28. In particular, Gulf countries are important producers of nitrogen fertilizers, which depend primarily on natural gas burned at high pressure in the presence of hydrogen to synthesize ammonia. (The hydrogen usually comes from natural gas as well.). But it’s not just that Gulf fertilizer can’t make it to export markets such as Sudan, Brazil, or Sri Lanka. It’s also that fertilizer producers elsewhere lack key ingredients. This is where the second-order effects of a supply chain crisis appear, just as they did during Russia’s invasion of Ukraine in 2022, which sent fertilizer prices soaring. Deprived of their natural gas supplies from Qatar, fertilizer firms in India, Bangladesh, and Pakistan have had to shut down production. Egypt, another important producer, has lost its gas imports from Israel and must turn to the ever-pricier LNG market. The benchmark price of urea, the most widely traded fertilizer, is up about 30 percent in the last month.

Germany’s Stress Test Markus Ziener/German Marshall Fund

The outbreak of armed conflict between Iran and the United States and Israel has become a direct stress test of Chancellor Friedrich Merz's government. It is once again exposing the fragility of Germany's post-2022 energy strategy and the dilemmas of European support for Ukraine. Further, it raises the question of whether Germany can be a security provider in an era of hard conflict.

How Azerbaijan Views the Iran War The National Interest

After two Iranian drones struck Azerbaijan’s Nakhichevan exclave last week, Azerbaijani President Ilham Aliyev demanded that Tehran apologize and punish those responsible. Threatening to respond with an “iron fist” if it refused, he ordered the armed forces to prepare “retaliatory measures.” The White House quickly condemned the strikes, declaring: “Attacks on the territory of our partners in the region are unacceptable and will be met with resolute US support for those partners.” The keyword in that statement is partner. America is drafting a new strategic map—tracing a line from Central Asia through the Caucasus to Europe—and Azerbaijan sits squarely at its center. Azerbaijan is the only country that borders both Russia and Iran. Any land route linking Europe with East Asia—if it is to avoid control by Moscow or Tehran—must pass through the South Caucasus and across Azerbaijani territory. In a world increasingly shaped by strategic competition between the United States and its allies on one side and China, Russia, and Iran on the other, this territory could decide the winners.

Shockwaves Across Asia: The Iran War’s Strategic Fallout The Diplomat

The Israeli-U.S. military strikes on Iran that began on February 28 have done more than ignite a Middle Eastern war. They have sent shockwaves rolling across Asia, from the Strait of Hormuz to the Sea of Japan, exposing the brittle underpinnings of regional energy systems, straining diplomatic balancing acts, and forcing governments to make hard choices they have long deferred. The conflict is, at its core, a distant war for most of Asia. But the consequences are arriving fast and close.

Europe’s Disjointed Response to the U.S.- Israeli War with Iran Council on Foreign Relations

The speed and scale of the Iran took most European governments by surprise. After leaving Europe in the dark about the capture of Venezuelan leader Nicolás Maduro, the United States launched a major military operation in the Middle East with little to no consultation with its allies in Europe, while expecting to use their bases and receive their broad support. Once again, European leaders found themselves scrambling to react to a conflict they had neither anticipated nor prepared for—and one in which they had little direct leverage. The result has been a strikingly disjointed European response.

What Is the Endgame in Iran? Colin Kahl/Foreign Affairs

The fog of war is thick in Iran, but two things are already crystal clear. No one can question the unrivaled military prowess displayed by the United States and Israel. Since February 28, U.S. and Israeli forces have killed Supreme Leader Ali Khamenei and senior commanders of the Islamic Revolutionary Guard Corps, struck thousands of military targets across Iran. Nor should anyone doubt the cruelty of the Iranian regime they are targeting, which has spent decades killing Americans, brutalizing its own people, threatening its neighbors with missiles and terrorist proxies, and racing to build up its nuclear program. But so much else about this war of choice remains unclear, and the biggest questions have gone unanswered by the Trump administration. In particular, how will this war end? And what will be the ultimate strategic implications of the Iran gamble?

The Potential Impact of a Billionaire Tax

The Net Present Value of the Billionaire Tax Act: An Assessment of the Fiscal Effects of California's Proposed Wealth Tax Benjamin Jaros, Joshua Rauh, Greg Kearney, John Doran, et al. Stanford University

The California Billionaire Tax Act of 2026 proposes a one-time 5% tax on the worldwide net worth of individuals exceeding $1 billion. This measure applies to tangible and intangible assets, including those held through trusts and certain recent transfers. Our proxy for these taxable assets in this dataset is the “Net Worth” of each California-based billionaire listed in the 2025 Forbes Billionaires listing. Our preferred revenue estimate implies that approximately 55% of the billionaire income tax base has or will avoid the tax, nearly double the 30.7% break-even threshold under even [proponent’s optimistic] assumption of six confirmed departures at a 1.5% real discount rate and approaching the 61.4% threshold at 3%. The wealth tax has positive net present value only if the one-time revenue exceeds the present value of foregone income taxes from departing billionaires. We simulate draws from uniform distributions over the plausible ranges for discount rates, revenue from the wealth tax, and lost income tax collections; 71% of draws yield a negative net present value, with a mean of [-] $24.7 billion, with a median of −$19.1 billion, and standard deviation of $38.4 billion. [See Figure 3 in gallery]. These estimates are conservative in that we exclude all non-income-tax fiscal spillovers, including lost sales tax, property tax, and business activity, such as employing other income taxpayers.

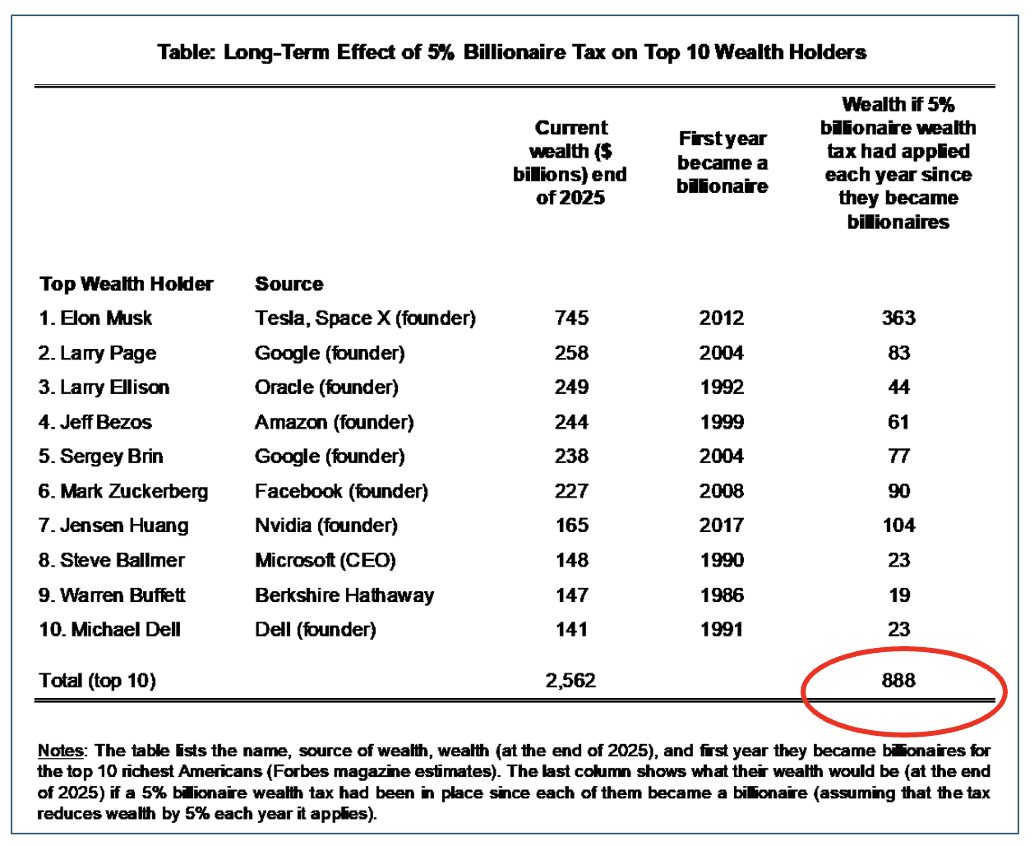

Why a Billionaire Wealth Tax Is the Most Direct Policy Tool To Curb The Growing Concentration of Wealth Emmanuel Saez & Garbiel Zucman, Professors of Economics, University of California, Berkeley (via the press release of the legislation via the website of the Office of Senator Bernie Sanders (I-VT)

The two UC-Berkely economics professors analyze Senator Bernie Sanders (I-VT) legislation proposing an annual 5% wealth tax. In their analysis, the believe it would raise approximately $4.4 trillion over the coming decade. They also argue that if such a tax had been in place since 1980, the current top 10 wealthiest Americans would be worth $888 billion, about 1/3 of the $2,562 trillion they currently possess as of the end of 2025.

The Limits of New York’s “Tax the Rich” Policy E. J. McMahon Manhattan Institute

As the nation emerged from the Great Recession in 2010, the capital gains of income millionaires were disproportionately concentrated in the four most populous states: California, New York, Texas, and Florida. Between 2010 and 2022, taxpayers earning $1 million or more in these states accounted, on average, for 50% of the nation’s total capital gains realizations. At the start of the period, California led all states, with 16% of capital gains among all U.S. income millionaires. New York ranked second, at 14%, while Texas and Florida trailed at 8.7% and 8%, respectively. The next 12 years saw a significant shift in the rankings. By 2022, Florida had topped the list, with 16.7% of capital gains income among millionaire earners, followed by California at 14.9% and Texas at 9.7%. New York had dropped to fourth place, with 8.9%—essentially changing places with Florida.

How Much Revenue Would Senator Sanders’ Wealth Tax Proposal Really Raise? The Tax Foundation

According to the Tax Foundation analysis of Senator Bernie Sanders (I-VT) recently introduced 5% wealth tax on billionaires, the projected $4.4 trillion of revenues raised over 10 years would be significantly less. The analysis also points out that most European countries have repealed wealth taxes due to limited revenue and administrative and compliance challenges.

The Americas

Why Lula is Struggling: Brazil’s October Election Now Looks Like a Coin-Flip Brian Winter/Americas Quarterly

As recently as six weeks ago, President Luiz Inácio Lula da Silva seemed to be cruising to reelection. Unemployment was at record lows; the stock market at record highs; inflation had closed 2025 at its lowest level in seven years. Lula’s archrival, former President Jair Bolsonaro, was in prison—and had just chosen Flávio, widely seen as the least charismatic of his four sons, to be his preferred candidate in October’s vote. Today, there is nary a breeze. A Datafolha survey published Sunday showed Lula with just a three percentage point lead in a hypothetical runoff against Flávio Bolsonaro, down from a 15-point advantage in December. Other polls have shown similar dynamics. The tightening is in some ways a return to familiar battle lines; after all, Lula won the 2022 election by just a 51%-49% margin. But there are signs that the Lula of 2026 is struggling to connect with voters and could be at genuine risk.

Latin American Small States in the Belt & Road Initiative: Narrating Status Amidst US-China Tensions Zara Albright/Diego Telias/Tom Long – Cambridge Review of International Affairs

Abstract: Starting in 2017, most small states in Latin America and the Caribbean joined China’s Belt and Road Initiative (BRI). Near-uniform membership contrasts with variation in the Asian power’s importance to regional economies. The BRI has brought little new investment in these states; recently, participation has risked retaliation from the United States. What explains these states’ affinity for the BRI, despite heterogeneous material costs and benefits? We argue that the region’s small states have approached the BRI less for its immediate material benefits than for the salient discursive resources that it offers. Political leaders mobilize these resources to construct status narratives that justify, especially to domestic audiences, how BRI participation will improve national status. We analyze paired case studies during each of two temporal waves: Chile and Ecuador (wave 1, 2017–2019) and Honduras and Nicaragua (wave 2, 2020–2025). In addition, we consider Panama as the first Latin American signatory (wave 1) and the only country in the region to renounce BRI membership (wave 2).

Recommended Weekend Reads

Germany’s China Shock, Trump’s Monroe Doctrine is Aimed at China, How The U.S. Population Has Shifted, Why China Doesn’t Want A U.S – Iran Deal, and How AI is Both Helping and Replacing Workers

February 27 - March 1, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them both interesting and useful. Have a great weekend.

The Americas

Trump's latter-day Monroe Doctrine is aimed at China Peterson Institute for International Economics

The US intervention in Venezuela, attacks on vessels in the Caribbean, financial squeeze on Cuba, and its bailout of Argentina should perhaps have come as no surprise. After all, the Trump administration has made no secret of its intentions, as laid out in the 2025 National Security Strategy (NSS) document: To "reassert and enforce the 'Monroe Doctrine' to preserve U.S. preeminence in the [Western] Hemisphere and deny outside powers control of strategic locations and assets." It would certainly appear that the administration is currently achieving the goals set out in the NSS, entrenching Latin America as the main stage for a geopolitical confrontation between the United States and China. But these actions could also introduce further turbulence into a region mired in political and economic problems. China is heavily invested in Latin America through various channels, notably its "green" Belt and Road Initiative. The framework has enabled China's public banks and state-owned enterprises to underwrite massive projects in renewable energy sources, critical minerals, and infrastructure. It is estimated that since 2010, China has invested around $35 billion in renewable energy projects alone. The figure does not include the $1.3 billion spent to finance the massive Port of Chancay in Peru, which connects South America's Pacific Coast to Shanghai.

Population drops and gains in every state FlowingData

The Census Bureau released population estimates for 2025. Most states gained population, but a few states saw more people move out than move in, with births not enough to compensate. By percentage, Puerto Rico, Hawaii, and West Virginia decreased in population the most since 2020. By total change, New York and California decreased by about 200,000 people each. The population in Louisiana, Illinois, and Mississippi also dropped. Idaho went the other direction with the largest increase over 10%. Texas and Florida populations increased the most, with total increases of 2.56 million and 1.92 million, respectively.

How Trump’s 15% Tariff Move Impacts Latin America Americas Quarterly

Latin American economies seem relatively well-positioned following the U.S. Supreme Court’s decision to invalidate last year’s tariffs on imports of goods and services and President Donald Trump’s announcement of a new 15% global tariff. Trump's previous levies were invalidated on February 20, after a majority of the U.S. Supreme Court’s justices (6-3) ruled that the president exceeded his authority to issue them, dealing the government a major setback. That day, Trump set a replacement global tariff of 10%, which was increased to 15% the next day.

Europe, China, and Iran

Germany’s China Shock Internationale Politik Quarterly

The China shock is here,” the German Economic Institute declared last July. Indeed, 2025 will go down as the year in which it could no longer be denied. Germany's trade deficit with China reached a record level of €87 billion—an increase of €20 billion compared to the previous year. And German exports to China continue to be in free fall. The United States, France, the Netherlands, Poland, and Italy have by now become more important export markets for Germany than China. At the beginning of this century, China accounted for 6 percent of global industrial production. Today, the figure stands at around 30 percent. China’s economic model is firmly geared toward global dominance in industries where Germany has been traditionally strong, such as automotive, mechanical engineering, and chemicals—as well as in future industries such as robotics and biotechnology. Beijing not only leverages the economies of scale of its vast domestic market but also makes forward-looking investments in research and development.

Why China Doesn’t Want the US and Iran to Make Peace The Diplomat

While Beijing publicly advocates restraint, sustained tensions between the U.S. and Iran serve its strategic interests. China's broader perspective on Iran is unlikely to change absent a major shock. Beijing views Tehran as a useful strategic partner in its long-term effort to counter Western – especially U.S. – dominance of the international system. As a result, China supports Iran diplomatically and economically, while also offering limited and discreet military-related assistance. This support does not typically take the form of overt arms sales, but rather the provision of dual-use components and technologies that can be used in Iranian drone and missile production. These activities allow Beijing to strengthen Iran’s resilience without incurring the costs associated with formal military alliances or large-scale weapons transfers.

What It Will Take to Change the Regime in Iran Behnam Ben taleblu/Foreign Affairs

The Islamic Republic of Iran is, quite possibly, at its weakest point since its founding in 1979. In June, Israeli and U.S. attacks destroyed its uranium enrichment capacity and many of its air defense systems. In December and January, the country experienced the most widespread domestic uprising since the birth of the Islamic Republic. Throughout, it has faced spiraling economic and environmental crises that it cannot fix. None of these events has knocked out the Islamic Republic. But there is no doubt it is down. It is easy to see why the Trump administration is prioritizing diplomacy and limited strikes. The Islamic Republic may be weak, but it is still lethal and capable of harming U.S. forces and civilian targets throughout its region. Such measures could inspire the masses of Iranians who took to the streets in December and January to do so again. Just this week, Iran witnessed smaller-scale campus protests, showing that animosity against the regime very much remains. If regular protests resume, American military power could level the playing field between the street and the state, giving the country’s demonstrators a chance to succeed.

Geoeconomics

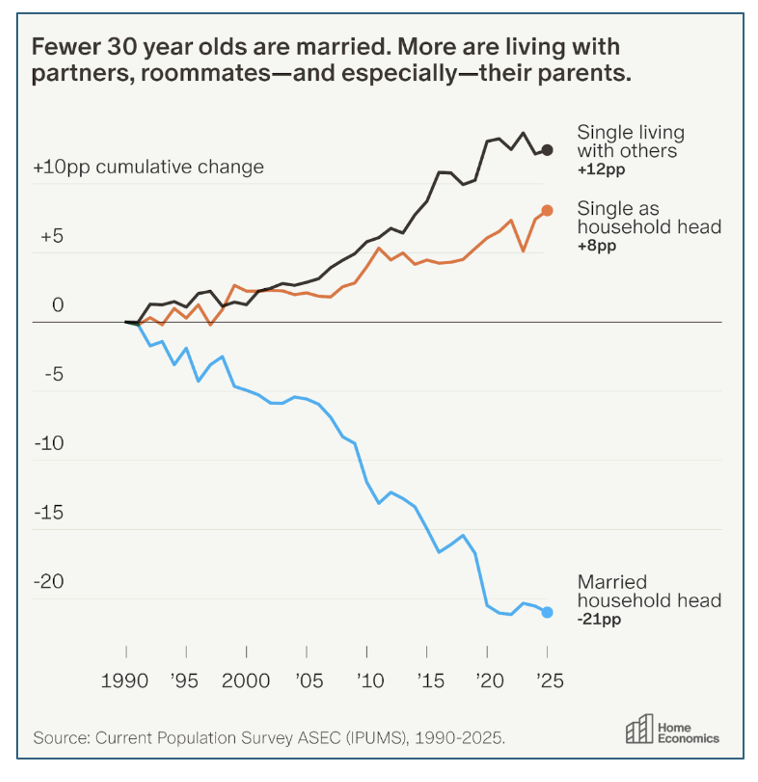

Living With Mom And Dad At 30 Aziz Sunderji Home Economics

The share of American 30-year-olds living with their parents or roommates nearly doubled btw 1990 and 2025, from 17% to 32%. Aziz Sunderji finds that this group is largely responsible for the age cohort’s 15pp decline in homeownership over that period.

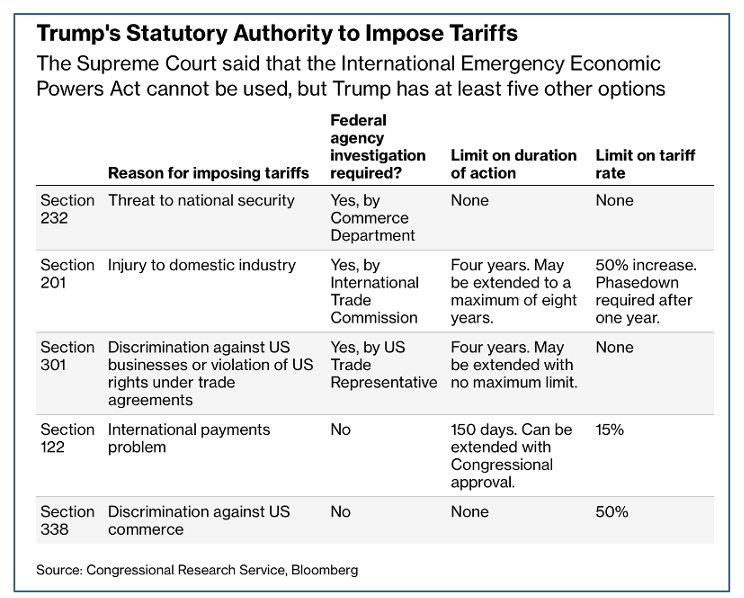

The New Global Tariffs Are Also Unlawful Philip Zelikow/Hoover Institution’s Freedom Frequency

On February 20, the Supreme Court ruled that President Trump’s tariffs imposed under an emergency powers law were unlawful. After raging at the court, the president imposed a new set of global tariffs using a different statutory authority. Now, the Trump Administration has moved to use Section 122 to carry on the tariff policy. And the author – who was involved in the recently decided case – argues the use of 122 is both obsolete and illegal.

The 2028 Global Intelligence Crisis Citrini Research

In this widely-hailed essay, Alap Shah of Citrini Research models a scenario that the author writes about the potential impact of AI on society. Shah’s vision is that “In every way AI was exceeding expectations, and the market was AI. The only problem… the economy was not…. AI capabilities improved, companies needed fewer workers, white collar layoffs increased, displaced workers spent less, margin pressure pushed firms to invest more in AI, AI capabilities improved… It was a negative feedback loop with no natural brake. The human intelligence displacement spiral. White-collar workers saw their earnings power (and, rationally, their spending) structurally impaired. Their incomes were the bedrock of the $13 trillion mortgage market - forcing underwriters to reassess whether prime mortgages are still money good.”

Speed Can Reindustrialize America Austin Vernon Blog

High US wages for skilled workers constrain robot adoption in manufacturing. “Many less productive US manufacturing firms could buy a robot, but couldn’t attract the talent to program it.” The US can’t “emulate” the low-wage, high-skilled China model.

AI Is Simultaneously Aiding and Replacing Workers, Wage Data Suggest J. Scott Davis Federal Reserve Bank of Dallas

For occupations with a very low experience premium, AI exposure lowered wage growth, likely due to substitution of AI for costly experienced workers. At the top of the experience distribution, AI raised wage growth, as it complements experienced workers.

The Flawed Paper Behind Trump’s $100,000 H-1B Fee Economic Innovation Group

Abstract: Do H-1B visa holders earn more or less than Americans? There are two different ways to answer this. If we compare H-1B holders to the average native-born worker, the answer is unequivocal that the visa holder is paid more. Median H-1B pay in 2024 was $120,000 per USCIS, compared to $67,000 for the average native-born worker. However, when we compare H-1B holders to otherwise similar native-born workers, the question becomes more complex. Answering it correctly requires careful examination. Unfortunately, a recent attempt at answering this question from Harvard economist George Borjas contains major errors.

Recommended Weekend Reads

Trump’s IEEPA Tariffs Are Dead. Now What?, Iran: What Happens Next if the US Launches Attacks, How A BRICS Currency Could Happen, and the Looming Fiscal Crisis in the Western World

February 20 - 22, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them of interest and useful as well. Have a great weekend.

U.S. Trade Policy After the IEEPA Decision

Trump’s Options After the Supreme Court Said His Tariffs Are Illegal Bloomberg

On Friday, the U.S. Supreme Court President Trump had illegally used of the International Emergency Economic Powers Act (IEEPA) for his April 2025 “Liberation Day” calls into question what Trump will do next. Trump has at least five tools he can use to offset the IEEPA tariffs; however, none of them offer the latitude that Trump’s interpretation of IEEPA allowed. Section 338 of Smoot-Hawley, which has never been used, likely has the broadest scope.

State of U.S. Tariffs: February 20, 2026 Yale University Budget Lab

The Budget Lab estimates the effects of all US tariffs and foreign retaliation implemented in 2025 after the decision by the Supreme Court of the United States that President Trump exceeded his authority to invoke the 1977 International Emergency Economic Powers Act (IEEPA) to impose reciprocal tariffs. Without IEEPA tariffs, consumers will face an overall average effective tariff rate of 9.1%, which remains the highest since 1946 excluding 2025. (If IEEPA tariffs had been allowed to stay in effect, this figure would have been 16.9%.) All tariffs to date as of February 2026 are projected to raise about $1.2 trillion over 2026-35, though slower economic growth reduces revenues and brings the net dynamic revenue to $1 trillion. (With IEEPA, these figures would be more than twice as large.) The economic implications of the SCOTUS decision are complicated by two major factors. First, in the short-term, firms will be aggressively seeking refunds on tariffs paid in 2025, which has large revenue effects and uncertain distributional effects. Second, the current Administration has stated its intent to replace IEEPA tariffs with tariffs using other authorities, but there remain timing and other questions regarding these steps.

Implications of Growing U.S. – Iran Military Tensions

The Day After Khamenei: Iran’s ‘Liberation’ Will Begin as an IRGC Power Struggle Charbel Antoun/National Interest

Many imagine the day after Ali Khamenei as a moment of sudden liberation: Iranians shaking off the mullahs and deciding their own destiny. The likelier opening act is far less romantic. The immediate aftermath will probably look less like a velvet revolution and more like the opening round of an insider power struggle—staged and refereed by the Islamic Revolutionary Guard Corps (IRGC) and its allies. The institutions that have grown strongest under Khamenei are not parliaments, parties, or independent courts, but the security state and its sprawling economic empire. Those are the actors best positioned to inherit the republic he leaves behind.

Iran’s regime is suffering from strategic vertigo. Its next misstep may be its last The Atlantic Council

Tehran appears to be suffering from a case of strategic vertigo. As Iranian leaders continue to see their major decisions backfire over the course of two and a half years, a disorienting dizzy spell may be the best way to describe the state of Iranian foreign policy. Negotiations between the United States and Iran are ongoing, with US President Donald Trump Thursday that he expects a resolution within ten to fifteen days, as he also undertakes a massive military buildup for a possible conflict. The talks provide the regime with a rare opportunity—a gift, even—to escape from yet another predicament. The question right now is whether leaders in Tehran grasp the magnitude of the moment and refrain from their old habits of obstinacy, or whether they will add another strategic error to their string of missteps—one that could be their last. With the United States preparing for strikes if negotiations fail, the question arises of how Iran reached the precipice in the first place.

What War With Iran Would Look Like Arash Reisinezhad/Foreign Policy Magazine

Washington and Tehran may be closer to military confrontation than at any point in memory, but they are not on the brink of war in any conventional sense. The most plausible outcome of the current standoff is not a U.S. invasion of Iran or a full-scale regional war. It is a limited, carefully calibrated strike designed to reshape bargaining dynamics rather than end them.

Iran: What Challenges face the country in 2026? House of Commons Library

In 2025, the US and Israel struck Iran’s nuclear program, the UN reimposed sanctions against the country and its economy continued to struggle. Iran’s regional position also worsened. Established leaders of many Iran-backed armed and proscribed terrorist groups have been eliminated, and their strength weakened in the regional conflict that has been ongoing since 2023. Some Iran-backed groups are facing renewed local and international calls to disarm. This briefing for UK Members of Parliament surveys the situation in Iran, including the challenges facing its government; the status of Iran’s nuclear program and the potential for further strikes in 2026; and pressures on Iran-backed groups in the region.

Iran Oil And Gas Market Size & Share Analysis - Growth Trends and Forecast (2026 - 2031) Mordor Intelligence

According to Mordor’s recent research, Iran’s oil and gas market size in 2026 is estimated at USD 39.18 billion, growing from 2025 value of USD 37.10 billion with 2031 projections showing USD 51.51 billion, growing at 5.62% CAGR over 2026-2031. Robust reserve availability, state-backed capital deployment, and resilient export flows underpin this trajectory even as sanctions pressure persists. The upstream sector anchors revenue, as Iran is the fourth-largest crude producer in OPEC. Meanwhile, the downstream segment is growing faster, with domestic firms adding fluid catalytic cracking and condensate-splitting capacity to increase product yields. Onshore production remains the backbone of the Iranian oil and gas market, but offshore investments at South Pars are accelerating to protect reservoir pressure and sustain natural-gas output. Asset deployment overwhelmingly favors development projects, yet exploration spending is rising because reserve replacement has become a policy imperative. High market concentration persists: The National Iranian Oil Company (NIOC) and its subsidiaries continue to dictate most decisions, although private and quasi-state contractors now win multi-billion-dollar tenders that were once the domain of foreign major oil companies.

Geoeconomics and Global Markets

Could a BRICS Currency Work? Jim O’Neill/ Project Syndicate

O’Neill – who coined the acronym “BRICS” – argues Economists have long dismissed the idea that a BRICS common currency could challenge the US dollar's role in the global economy, and for good reason. But that doesn't mean there couldn't be new common rails for settling trade between countries that want to escape the long arm of the US government.

Across The Rich World, Fiscal Crises Loom The Economist

The Economist calculates that most rich countries could still run small primary deficits [deficits net of interest payments] and keep debts stable as a share of their economies, even if they had to refinance all their debt immediately at today’s rates. The largest primary surplus required to balance debts is in Britain, at just 0.3% of GDP. That is not large for countries in a pinch. In the late 1990s Italy ran primary surpluses of 3-6% of GDP to bring down debts before joining the euro. In Britain and America, deficits are large. The belt tightening needed to stabilize the debt-to-GDP ratio exceeds 2% of GDP; in France it is greater than 3% of GDP. Things look worse still when you consider the coming wave of spending on ageing populations, defense and the climate transition. And higher debt interest costs to come are not yet fully accounted for.

Are Government Bonds Safe in Times of War and Pandemic? Zhengyang Jiang, Hanno Lustig, Stijn Van Nieuwerburgh and Mindy Xiaolan National Bureau of Economic Research

Abstract: We analyze real returns on U.S. and U.K. government debt during major wars and the COVID-19 pandemic over the past three centuries. Wars are associated with sharply negative real returns on outstanding government debt, with returns falling far below economic growth, in contrast to peacetime periods when returns exceed growth. Elevated surprise inflation and financial repression account for a cumulative 31% wedge between returns and growth over four years of war, implying that bondholders bear a substantial share of wartime fiscal costs. During wartime, government bonds also systematically underperform risky assets.

When Houses Outrun Paychecks: The Lost Decades of Housing Affordability Federal Reserve Bank of St. Louis ON the Economy Blog

Abstract: In this blog post, we analyze how housing affordability has evolved over the past 20 years. For most U.S. counties, the story is remarkably similar: Home values have risen much faster than the incomes of the people living in them. From 2000 to 2024, median per-capita income has grown steadily but modestly, at around 155% in nominal terms. Over the same period, median home prices—when measured carefully and adjusted for local composition—have increased at a much faster pace, at around 207% in nominal terms. This divergence helps explain why younger households struggle to buy their first home, while longtime owners increasingly view housing as their primary source of wealth.

Weekend Reads

Mexico – US Relations Get More Tense, Russia Hitting a Critical Inflection Point Internally, How American First Investment Pledges Are Structured – But Will It Work? , And the Impact of Inflation on Fertility

January 30 - February 1, 2026

Below are several reports and articles we read this past week that we found particularly interesting. Hopefully, you will find them of interest and useful as well. Have a great weekend.

Americas

‘What the hell do we do with this issue’: Mexico confronts Trump’s Cuba pressure Politico

President Donald Trump’s increasingly overt attempts to bring down the Cuban government are forcing Mexican President Claudia Sheinbaum into a delicate diplomatic dance. Mexico is the U.S.’s largest trading partner. It is also the primary supplier of oil to Cuba since the U.S. seized control of Venezuela’s crude. Now, Sheinbaum must manage her relationship with a mercurial Trump, who has at times both praised her leadership and threatened to send the U.S. military into her country to combat drug trafficking — all while appeasing her left-wing party Morena, factions of which have historically aligned themselves with Cuba’s communist regime.

Washington’s Sharpening Stance on Mexico Americas Quarterly

There is a deep shift underway in Washington—one that redefines Mexican organized crime not primarily as a law-enforcement problem or a bilateral cooperation challenge, but as a direct national security threat to the U.S. That redefinition is already reshaping U.S. policy tools, institutions, and expectations vis-à-vis Mexico, with potentially profound consequences for the bilateral relationship.

Can anything halt Latin America’s lurch to the right? Financial Times

“It’s because of the expansion of the major criminal markets in the region,” says Council on Foreign Relations Fellow Will Freeman. “The huge increase in the size of the cocaine trade, the boom in illegal gold mining, for a time, the wave of human smuggling, and the way that has seeded a lot of new gangs and criminal outfits in different parts of the region that didn’t previously have to deal with this.” The dramatic capture of Venezuela’s authoritarian president, Nicolás Maduro, by US commandos in the early hours of January 3 has, if anything, reinforced the swing to the right in most of the region, pollsters say.

Is Russia at a Critical Inflection Point?

Russia’s Grinding War in Ukraine Center for Strategic and International Studies