Fulcrum Perspectives

An interactive blog sharing the Fulcrum team's policy updates and analysis.

Recommended Weekend Reads

Foreign Private Capital Overtook Central Banks in the Treasury Market, U.S. Grand Strategy and China, and How a Quiet US – AU Deal Could Reshape Investment in Africa

April 24 - 26, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them of interest and useful as well. Have a great weekend.

Geoeconomics, Financial Markets, and AI

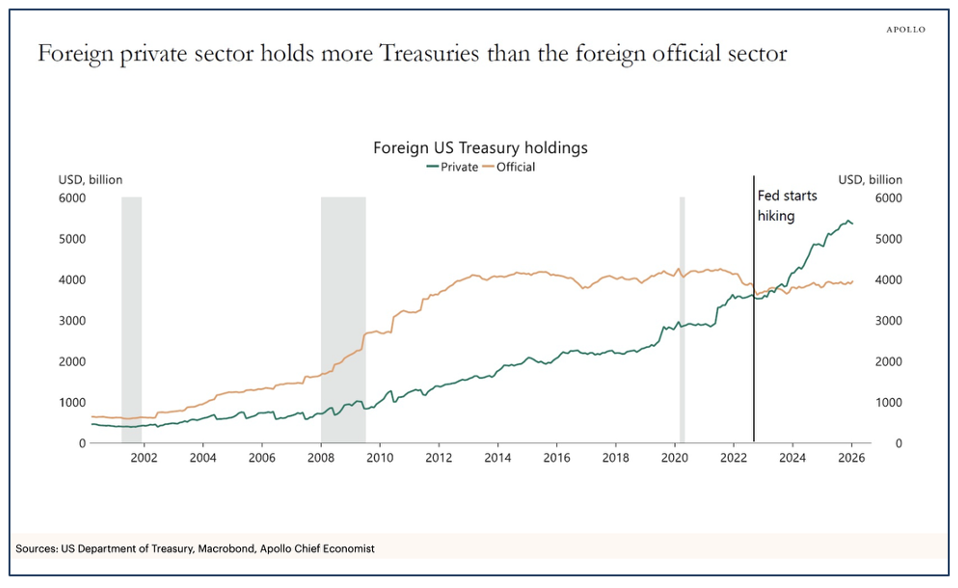

Foreign Private Capital Has Overtaken Central Banks in the Treasury Market Torsten Sløk Apollo

For the first time, foreign private buyers own more Treasuries than the foreign official sector, Slok notes, suggesting the “Treasury market [may be] increasingly sensitive to the return expectations of price-sensitive private capital.”

Corporations in the Crosshairs: Commercial Actors, Conflict Escalation, and Crisis Simulation Journal of Simulation and Gaming

Abstract: The authors reach three substantive findings. First, the game demonstrated that cyber and kinetic attacks on commercial assets can trigger escalation—challenging arguments that attacks on commercial targets are less provocative than attacks on military and government targets. Second, the growing role of commercial firms in the international security arena makes communication channels for information sharing and coordination between the government and these firms critical for crisis management. Third, the wargame highlighted how relying on influential private sector leaders involves tradeoffs. These individuals can provide critical information to governments, leverage their companies to support government efforts, and help coordinate broader private sector engagement. However, they may also prioritize their own commercial interests over national ones. Additionally, the simulation revealed lessons that may assist designers of future simulations involving commercial actors.

Drivers of Population Growth: Natural Increase vs. Net Migration Federal Reserve Bank of St. Louis

National population growth reflects both natural increase and net migration, with each factor shaping countries differently across income levels. Natural increase drove almost all population growth in poor countries from 1960 to 2023. In rich countries, however, both natural increase and net migration sustained their population growth during that same period.

Six Reasons Claude Mythos Is an Inflection Point for AI—and Global Security Council on Foreign Relations

Anthropic’s new AI model has taught itself to hack into software infrastructure systems believed to be among the most secure in history. While there is no question that the technology is profoundly dangerous, it is unclear if defenders will win a race against time to protect a sea of vulnerable targets.

Forecasting the Economic Effects of AI National Bureau of Economic Research

Abstract: We elicit forecasts of how AI will affect the U.S. economy, comparing the beliefs of five groups: academic economists, employees at AI companies, policy researchers focused on AI, highly accurate forecasters, and the general public. The median respondent in each group expects substantial advances in AI capabilities by 2030, small declines in labor force participation consistent with demographic shifts, and an annual GDP growth rate of 2.5%, which exceeds both the typical medium-run (2.0%) and long-run (1.7%) baseline forecasts from government agencies and private-sector forecasters. Conditional on a “rapid” AI progress scenario, in which AI systems surpass human performance on many cognitive and physical tasks, experts forecast substantial, though not historically unprecedented, economic shifts: annualized GDP growth rising to around 4% and the labor force participation rate falling from its current level of 62% to 55% by 2050, with roughly half of that decline—equivalent to around 10 million lost jobs—attributable to AI. A variance decomposition suggests that expert disagreement about these effects is driven primarily by different beliefs about the economic effects of highly capable AI systems rather than by disagreement about the pace of AI progress. These forecasts map onto notably different policy preferences across groups: experts strongly favor targeted measures such as worker retraining, whereas the general public supports both targeted programs and broader interventions, including a job guarantee and universal basic income.

·Construction Costs Rarely Fall Brian Potter Construction Physics

Multiple measures show real construction costs have “virtually never fallen” since 1875, with the striking exception of 1975–95—consistent with input cost and productivity series. The upward drift is not new; if anything, it has moderated over time

Africa

A quiet US-AU deal that could reshape investment in Africa Africa Futures/AUDA NEPAD

The Trump administration and the AU have started a bold journey that could ‘flip the script’ on decades of development cooperation. The Strategic Infrastructure and Investment Working Group (SIWG), formed on 28 January 2026, will enable senior officials and experts to identify investment opportunities, particularly involving the US private sector. It could strengthen African and US strategic options amid major-power rivalries globally. But both sides must ensure Africans’ full partnership as investors and decision makers in those projects.

The Sudan War in 10 Charts The Center for Strategic and International Studies

Sudan’s civil war has now entered its fourth year, with its two main factions locked in a grinding war of attrition. The conflict began on April 15, 2023, between the Sudanese Armed Forces (SAF) led by General Abdel Fattah al-Burhan, and the Rapid Support Forces (RSF) paramilitary, led by Mohamed Hamdan Dagalo, popularly known as Hemedti. Today, the country is split roughly in two, with the SAF in control of the east and the RSF in control of the west. As a result of the war, Sudan is now the world’s largest displacement and hunger crisis. Rape and sexual violence are both widespread and systematic and have become a defining feature of the war. Sudan’s rich cultural heritage, too, is being erased.

Impact of the Iran War

The Iran War Is a Stress Test for Gulf States Carnegie Endowment for International Peace

The U.S.-Israeli war on Iran has had dire security and economic consequences for the Arab states of the Gulf Cooperation Council (GCC). Iranian missiles and drones struck airports, hotels, and energy infrastructure across the region, triggering the largest oil supply shock in the history of global energy markets and a near-total collapse of aviation and tourism. Attacks on desalination plants have raised fears of a humanitarian emergency. Threats to shipping through the Strait of Hormuz have disrupted over 70 percent of the region’s food imports. Externally, the war has prompted questions about the risks and costs of the region’s reliance on American security guarantees and bases. Beyond these effects, the Iran war is a stress test for domestic governance and social cohesion inside Gulf states, surfacing and sharpening preexisting fissures and vulnerabilities while introducing new pressures. Among the more prominent of these dynamics are a worsening crackdown on freedom of expression and increased securitization more broadly; a rise in sectarian tensions and internal scapegoating amid the very real threat of Iranian subversion; and the imperilment of the Gulf’s migrant labor communities, upon which much of the region’s prosperity relies. None of these shocks poses a serious challenge to stability or the survival of the region’s monarchies—Gulf regimes are hardly brittle and have weathered such shocks in the past.

The Strait of Hormuz in 8 Charts Center for Strategic and International Studies

CSIS has put together a superb interactive, moving set of charts showing what is happening – and not happening – in the Strait. Overall, access to the Strait of Hormuz, which carries roughly a quarter of global oil flows, remains contested. The waterway has been effectively closed since March 2, following U.S. and Israeli strikes on Iran. Although Tehran declared the strait open on April 17, the Islamic Revolutionary Guard Corps reversed course and announced it shut just one day later. The United States has since moved to enforce its own presence, including by seizing an Iranian-flagged cargo vessel on April 19. Vessel tracking and maritime trade data offer key insights into the ongoing dispute.

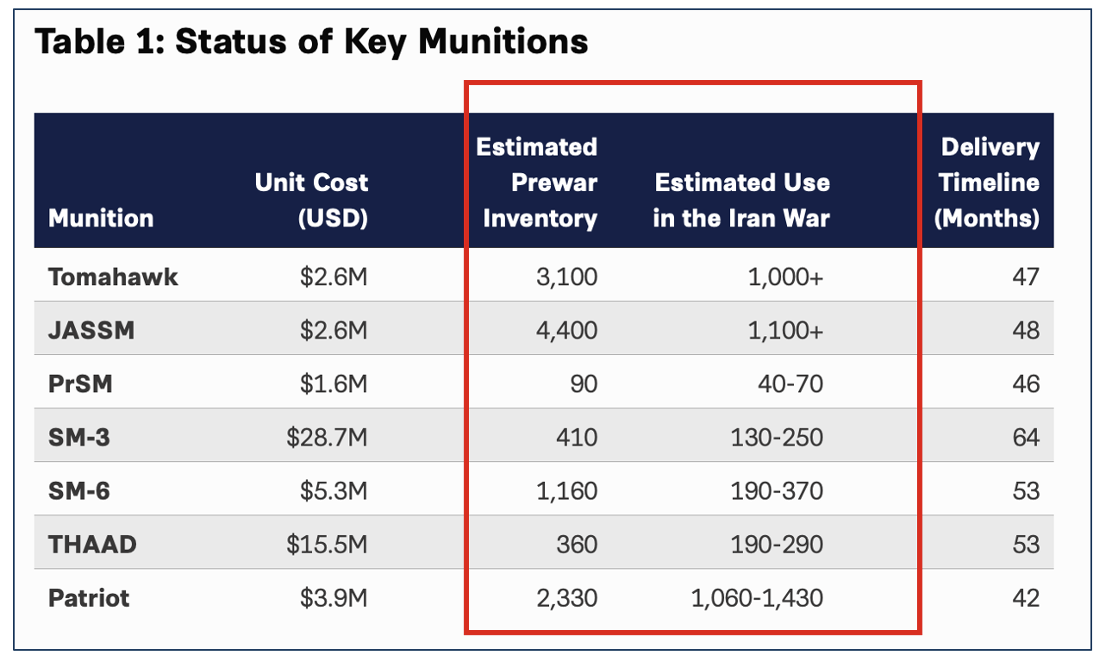

Last Rounds? Status of Munitions at the Iran War Ceasefire The Center for Strategic and international Studies

Concern about the status of U.S. munitions inventories has intensified as reports emerge about high expenditures of Tomahawks, Patriots, and other missiles in the Iran war. As Operation Epic Fury remains paused in a shaky ceasefire, there is an opportunity to assess whether the U.S. military nears the point of going “Winchester”—or running out of ammunition. Analysis of seven key munitions shows that the United States has enough missiles to continue fighting this war under any plausible scenario. The risk—which will persist for many years—lies in future wars.

Strategy Going Forward from the U.S. And German Perspectives

US Grand Strategy and the China Factor with Nadia Schadlow China Considered Podcast

Dr. Elizabeth Economy sits down with Nadia Schadlow, former deputy national security advisor for strategy in the first Trump administration and author of the influential 2017 National Security Strategy (NSS). Schadlow reflects on how the NSS was architected around the shift toward great power competition and America's four core national security interests: protecting the homeland and way of life; promoting American prosperity; preserving peace through strength; and advancing American influence. The conversation moves through key differences between the first and second Trump administrations, including process, tone, and the role of ideology in foreign policy, before turning to a substantive debate about the limits of multilateral institutions and Schadlow's argument in a recent Foreign Affairs essay that state-centric approaches can outperform global governance frameworks. Economy and Schadlow also assess the strategic landscape ahead of a potential Trump-Xi summit, discussing where US leverage is real, where it may be overstated, and whether tariffs alone can move China's economic model. They close with a shared critique: that the United States has consistently failed to develop a coherent, assertive diplomatic and development strategy to compete with China's Belt and Road Initiative.

A Grand Strategy of Consolidation: How Trump Can Revitalize American PowerA. Wess Mitchell/ Foreign Affairs

For three and a half decades, it has maintained peace and sustained influence in all the world’s major regions without difficult tradeoffs. It continued to assume it can do so even as the country’s relative economic strength decreased, and rival military buildups eroded its superiority. As a consequence, the United States now faces a serious misalignment between its national power and the strategic objectives to which it has become accustomed.

The Return of Power Politics to the Market: Theory and Practice of the Geoeconomic Zeitenwende The Stiftung Wissenschaft und Politik/German Institute for International and Security Affairs

The return of power politics to the market is a defining feature of the geoeconomic Zeitenwende, as is currently being experienced in international politics. This has brought renewed attention to the long-standing conventional wisdom that economic activity can not only generate prosperity but also promote foreign and security policy objectives. The analysis and strategy of foreign, security, and economic policy require a clear conceptualization of the term “geoeconomics”. This is necessary not least to weigh the costs and benefits of geoeconomic measures in a well-founded manner, and to assess their prospects for success more realistically. The contributions to this research paper focus on the theoretical and conceptual foundations of geoeconomic thought and examine selected empirical case studies of geoeconomic action in functionally defined policy areas. In order for German geoeconomic policy to become more effective and coherent, the following approaches are recommended: first, the establishment of interagency structures for the cross-cutting task of geoeconomics; second, the expansion of communication and coordination with relevant stakeholders from the business sector and academia; and third, the strengthening of international cooperation with like-minded partners.

Recommended Weekend Reads

Assessing The Iran War’s Global Economic Shocks, The Myths and Realities of Petrodollars, The Fog of AI War, and How the U.S. Post Office is About to Collapse

April 17 - 19, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them of interest and useful as well. Have a great weekend.

More On the Impact of the Iran War

How the War in the Middle East Is Affecting Energy, Trade, and Finance International Monetary Fund

According to the IMF, “Although the war could shape the global economy in different ways, all roads lead to higher prices and slower growth. A short conflict might send oil and gas prices soaring before markets adjust, while a long one could keep energy expensive and strain countries that rely on imports. Or the world may settle somewhere in between—tensions linger, energy stays costly, and inflation proves hard to tame—with ongoing uncertainty and geopolitical risk. Much depends on how long the conflict lasts, how far it spreads, and how much damage it inflicts on infrastructure and supply chains.”

"Look Through" the Hormuz Shock if You Want. U.S. Inflation is Still Running Hot Matt Klein/The Overshoot

Core goods inflation was running ~1 percentage point above pre-pandemic levels in both 2023 and 2024, with price declines slowing from mid-2024 onward — before tariffs became a primary factor. The question for policymakers is what this “one-time thing”, as Federal Reserve boss Jerome Powell has called it, will do to the underlying trend rate of inflation.

Petrodollars. Myths and Reality Brad Setser Council on Foreign Relations

The Iran War has brought renewed focus to the role of Petrodollars. The foundation of the dollar’s global role, it is sometimes argued, rests on the willingness of the Gulf countries (but not Russia) to price their oil in dollars. But it was never quite clear why oil pricing mattered quite as much as some claim. To be sure, there are network effects around dollar pricing. But it isn’t hard to pay for oil in a global currency like the euro, even if the underlying contract is priced in dollars. There is a deep and liquid market for converting euros into dollars, and a firm aiming to lock in the euro price of oil 3 months forward can buy oil forward in dollars and dollars forward with euros, thereby locking in a euro price. Dollar settlement is a problem for countries that are sanctioned by the U.S. and the EU and for frontier economies that cannot settle their oil bill in local currency, but it hasn’t required most European oil importers to build up big stocks of dollar reserves just to pay for oil. What has mattered at times is how the big oil exporters manage their surplus funds when there is a surge in the global price of oil.

Three Scenarios for the Gulf States After the Iran War Carnegie Emissary

Amid a tenuous U.S.-Iran ceasefire, Arab Gulf monarchies are aiming to project strength. “We prevailed through an epic national defense . . . in the face of treacherous aggression,” Emirati diplomatic adviser Anwar Gargash wrote on X. Saudi-owned newspaper Asharq Al-Awsat emphasized the kingdom’s “intensive political consultations” with regional countries as leading to the present calm. Yet member states of the Gulf Cooperation Council (GCC) still face immense challenges in shoring up their security. A substantial U.S. and Israeli air campaign was unable to eliminate Iran’s will or capability to exert power in the Gulf, with Iran turning historically secure neighbor states into war zones overnight. Neither the United States nor any other actor put forward a decisive solution for the de facto Iranian closure of the Strait of Hormuz, while the Islamic Republic retains its highly enriched uranium and its nuclear program. And the GCC has no seat at the table, despite its entreaties, for negotiations that will shape the bloc’s economic and security environment for years to come. Where do the Gulf states go from here? We offer three scenarios—a hopeful one, a realistic one, and a cautionary one—that illustrate both potential areas of cooperation and the risks of greater fragmentation.

What the Iran War Means for the “Axis of Resistance” Hamidreza Azizi/Foreign Affairs

The war is heightening the salience of Shiite identity across multiple arenas at once and, in doing so, reshaping how political and military actors assess both their interests and their risks. Groups that might otherwise have remained on the sidelines are becoming more likely to get involved in the strife, and those already fighting face growing pressure to escalate. The consequence is a feedback loop: actions driven by fears of marginalization provoke responses that alarm more and more people, expanding the social base for Shiite mobilization. The “axis of resistance,” Iran’s network of nonstate allies and proxies across the region, has endured numerous setbacks since 2023. But ongoing U.S. and Israeli military actions may lead to its reconstitution, not through the orchestration of Tehran but rather as a result of the altogether more organic impetus of an embattled Shiite identity.

Europe

A Transatlantic Economic Reset Penny Nass/German Marshall Fund

The fixation on tariffs and trade skirmishes obscures a more consequential reality, one in which the EU-US relationship is being shaped by a rapidly deteriorating geopolitical environment that tests political trust and strategic coordination. It also overshadows the fact that the transatlantic relationship is not primarily a trade relationship but the world’s largest and most strategically significant investment partnership. Three areas demand urgent join action: Critical minerals, the Digital Stack, and Infrastructure.

The Fog of AI War Raluca Csernatoni/Carnegie Strategic Europe

An irreducible uncertainty haunts every battlefield: the fog of war. And for two centuries, military innovation has promised to lift that fog. Artificial Intelligence (AI) was supposed to be the technology that finally did so, replacing human guesswork with machine precision and processing oceans of data at speeds that would render uncertainty obsolete. But acknowledging the advantages is not the same as ignoring what happens when speed, attrition, and scale become organizing principles of warfare. U.S. President Donald Trump's dispute with Anthropic, which insisted that its models should not be used without guardrails against fully autonomous weapons and mass domestic surveillance, ended with the Pentagon designating the company a supply chain risk. The message from the world’s largest military power is that normative constraints on military AI are obstacles to innovation rather than preconditions for lawful use. Europe can play a key role in all of this.

Assessing the damage: What the Iran war really means for Europe’s defense European Union Institute for Security Studies

Regardless of whether the ceasefire between the US and Iran holds, the war in the Middle East complicates European rearmament and support for Ukraine, while also further eroding confidence in the United States as a reliable guarantor of Europe's defense. To put their defense ramp-up on a firmer footing, Europeans should reduce exposure to US political volatility, industrial bottlenecks, and the diversion of defense equipment during wartime.

Geoeconomics, Technology, and Trade

A Tax Revolt Is Under Way In America The Economist

Democrats and Republicans alike think they are overtaxed, as do both rich and poor. YouGov’s polling finds that around 60% of Americans at every income level think they are taxed too much—despite being taxed at very different rates. Statehouses are hearing this, too. Many, citing strong economic growth, have cut taxes in recent years. Enthusiasm is building to go further and faster, leaving some observers wary. “Most have done so responsibly thus far,” says Jared Walczak of the Tax Foundation, a think-tank. “But they now risk overreaching and making reductions they cannot afford.” A wave of localities is pushing through property-tax exemptions for retirees. Florida is flirting with abolishing non-school property taxes altogether. Ohio has a possible ballot initiative to scrap them in all forms.

Evaluating the Impact of Tariffs on US Agriculture a Year After Liberation Day Joseph Glauber/American Enterprise Institute

In April 2025, the Trump administration levied 10 percent tariffs on virtually all countries and higher “reciprocal” tariffs on certain countries, ushering in a new and uncertain tariff architecture that saw significant changes, exemptions, and additional actions over the following year. The tariffs modestly reduced overall US agricultural and food imports, but with significant heterogeneity by exporting country and product category. The tariffs had mixed effects on US agricultural exports, with exports to China and Canada falling partly because of retaliatory tariffs and consumer reactions, respectively. After imposing the tariffs, the United States negotiated several bilateral trade deals with other countries. However, given the lack of product-specific details, China’s continued retaliatory measures, and the Supreme Court’s decision striking down most of the US tariffs, it is unclear whether these deals will actually improve agricultural market access for US exporters.

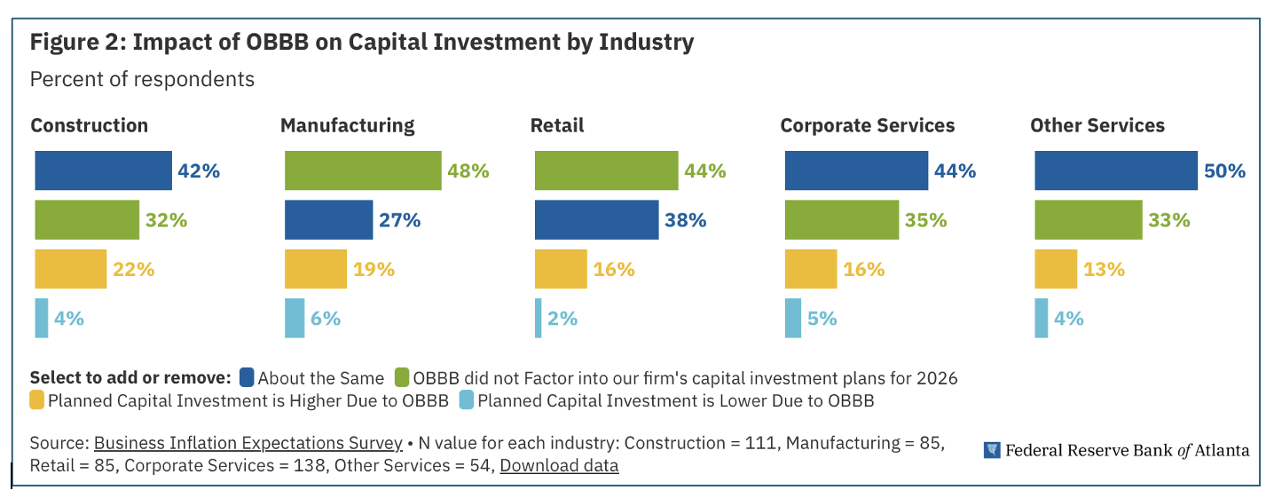

Did the OBBB Affect Firms' Plans for 2026? Federal Reserve Bank of Atlanta

Around 20 percent of respondent firms in the Atlanta Fed's Business Inflation Expectations (BIE) survey told us that they consider the One Big Beautiful Bill (OBBB) in their decision-making and short-term planning. The remaining firms said they did not factor in the OBBB when planning for outcomes such as capital expenditures, employment, and sales revenue forecasts. These results may be a reflection of the fact that many of the provisions of the law were already in place and with the passage of OBBB are now extended or made permanent (such as provisions of the 100 percent bonus depreciation and the 20 percent deduction for qualified business income). Our findings suggest that a broad-based and sizeable future surge in business activity stemming from the policy change may not be likely.

Congress Seeks Solution for Averting USPS Fiscal Collapse Kevin Kosar/Washington Examiner

Last month, U.S. Postmaster General David Steiner added another major item to Congress’s already long to-do list: rescuing the Post Office. “The Postal Service is at a critical juncture. At our current rate, we’ll be out of money in less than 12 months.” That may not sound like a big deal. Government agencies run out of money each year, and every January and February, they go hat-in-hand to Congress and ask for funding. Usually, they get it, and when Congress fails to deliver the dollars, agencies close for a bit or their staff work without pay until legislators enact a spending law. The U.S. Postal Service is different. USPS is one of 17 government corporations that pay for themselves by earning revenue through the sales of goods and services. The agency sells around $80 billion in postage each year, mostly to large companies offering credit cards (e.g., Capital One) or selling goods (e.g., Walmart). When the Post Office runs out of cash in the first half of 2026, Steiner explained, “the Postal Service would be unable to deliver the mail.”

Recommended Weekend Reads

The Iran War: What to Expect and Can There Be Change? Challenges to China’s Economy, The Coming US-Cuba Showdown, and America’s Great Happiness Compression

March 6 - 8, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them both interesting and useful. Have a great weekend.

The Iran War

The Mirage of the New Middle East: War With Iran Won’t Reshape the Region the Way America Wants Dalia Dassa Kaye/Foreign Affairs

Eager to show that he can do what no American leader has done before, President Donald Trump has chosen conflict over diplomacy and gone to war with Iran. How this war will end remains uncertain. But when it does, the United States will have to face what comes next. To the extent that the Trump administration has considered plans for “the day after,” it seems to have made a series of overly optimistic assumptions about how the war might reshape Iran and the Middle East. The outcome of this war will likely fall far short of these rosy expectations. After the bombing ends, Iran and the region could look worse, or at least not better, than they did before the war. The fighting could create a power vacuum in Tehran, sour U.S. allies on their partnerships with Washington, and produce ripple effects on conflicts elsewhere in the world, all without removing sources of regional strife that have nothing to do with the regime in Iran.

How Far Can Russian Arms Help Iran? Carnegie Russia Eurasia Center

While the United States and Israel are starting another military intervention against Iran, Russia is increasing arms supplies to the isolated Islamic nation—despite its own ongoing war with Ukraine. Tehran is already in possession of Russian trainer jets, attack helicopters, armored vehicles, and small arms. Now the two countries have signed another major deal, according to the Financial Times, under which Russia will supply Iran with Verba man-portable air defense systems (MANPADS) worth 500 million euros. Despite the growing scale of the cooperation in military technology, these arms shipments are still unlikely to be able to protect Iran from U.S. or Israeli air strikes. What’s far more likely is that Russian weapons will continue and to grow significantly if Russia gets the opportunity.

War With Iran: Why Now and What Comes Next Carnegie Connects Podcast

Host Aaron David Miller discusses the Iran War with the Brooking Institution’s Suzanne Maloney, International Crisis Group’s Ali Vaez, and Yale University’s Rob Malley on these and other Iran-related issues, on the next Carnegie Connects.

Good News: Iran’s Nuclear and Missile Programs Look Destroyed. Bad News: The Regime May Survive 19fortyfive.com

Dr. Andrew Latham, a professor of international relations and fellow at Defense Priorities, evaluates this “Trumpian Dilemma.” He argues that while the mission to disable programs has been a triumph, the mission to reshape the Iranian political order remains a dangerous, open-ended commitment that may collide with the administration’s “America First” instincts.

China’s Economic Outlook

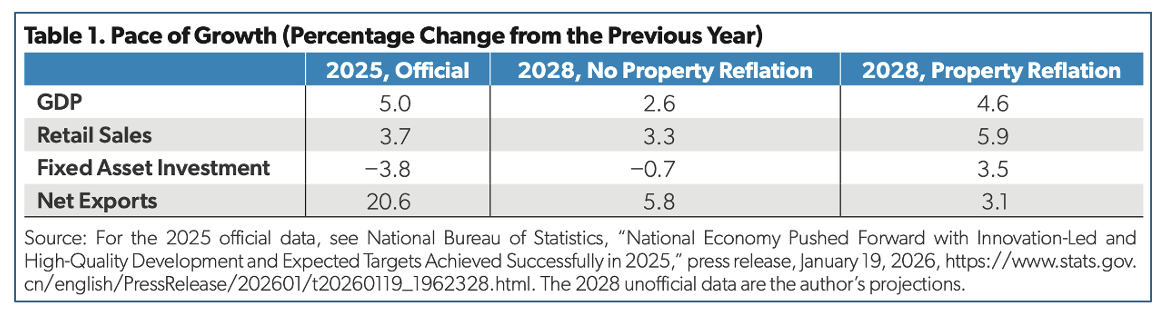

When Does China Stop Growing (Entirely)? Dereck Scissors/AEI

The Chinese economy has been generally weaker than acknowledged in the 2020s. The most frequently discussed solutions, such as stimulating consumption, cannot generate a sizable, sustained impact for more than a year or so. Reinflating the property bubble would do so. It cannot be done immediately or easily but could for a multiyear period bring clearly faster economic growth without wrenching dislocation or automatically adding to the debt burden. In the longer term, even successful property reflation will not matter much. Unwillingness to reform, debt accumulation, and especially demography guarantee a China that essentially stops growing by the late 2030s.

China’s Cheap Money Is Shaking $9.5 Trillion Global Loan Market Bloomberg

Chinese banks, flush with low-cost funds, are reshaping parts of the global loan market, underscoring how deflationary pressures in the world’s second-largest economy are increasingly influencing competition with international lenders. Much like US and European manufacturers who have long complained about being undercut by cheaper Chinese rivals, bankers at global institutions now say they’re facing the financial equivalent: being priced out of some of Asia’s most sought-after borrowers as Chinese lenders extend cheaper credit across borders. Enabled by Beijing’s monetary easing to counter slowing growth, Chinese banks are expanding overseas lending amid weakening domestic credit demand. That edge may prove even more significant as the Iran crisis threatens to upend global energy markets, raising the likelihood that major central banks will hold off easing interest rates amid mounting uncertainty.

Growing US – Cuban Tensions

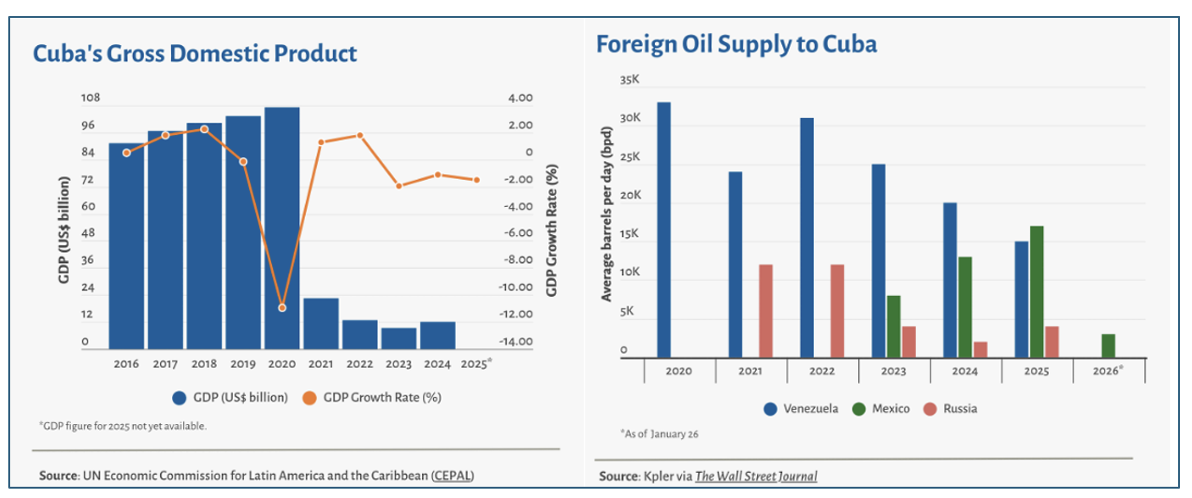

The Coming Showdown Over Cuba Rut Diamint & Laura Tedesco/Foreign Affairs

President Trump stated this past week that “Cuba is going to fall pretty soon. They want to make a deal badly.” Even before the current crisis, the Cuban people had long suffered under a cruel dictatorship, ruinous economic policies and mismanagement, and a six-decade U.S. trade embargo. In recent years, the island has experienced gasoline and medicine shortages, routine power outages, food cost increases, and mosquito-transmitted-disease outbreaks that have overwhelmed the public health system. Havana has little room to maneuver. Yet the chances that Trump will launch a Maduro-style military mission in Cuba remain low. After his Venezuela operation, undertaking a similar ouster would no longer have the advantage of surprise, and Cuba’s security forces are generally believed to be more loyal to their regime than Venezuela’s were to theirs.

Seven Charts on Cuba’s Economic Woes Americas Society/Council of the Americas

The Caribbean island is undergoing its worst economic period in decades while facing rising U.S. pressure. These seven charts show how the island country is facing an extraordinary economic and demographic collapse.

Cuba’s Military: The Institution Washington Cannot Ignore Americas Quarterly

For more than six decades, U.S. policy has failed to dislodge the Cuban regime, even when it appeared economically and politically vulnerable. As Washington again intensifies pressure on the island, policymakers must confront a central reality often overlooked in external debates: the decisive role of Cuba’s Revolutionary Armed Forces (FAR). More than a traditional military institution, the FAR functions as a political, economic, and administrative pillar of the state. It mediates regime continuity, oversees strategic sectors of the economy, and would shape the parameters of any eventual transition. In practice, the keys to both change and stability in Cuba are likely to rest not with opposition movements or external actors, but with key members of the FAR.

America’s Mood vs. Historic Economic Growth

Poverty and Dependency in the United States, 1939–2023 Richard V. Burkhauser & Kevin Corinth/National Bureau of Economic Research

Abstract: We compare trends in absolute poverty before (1939–1963) and after (1963–2023) the War on Poverty was declared. Our primary methodological contribution is to create a post-tax post-transfer income measure using the 1940, 1950 and 1960 Decennial Censuses through imputations of taxes and transfers as well as certain forms of market income including perquisites (Collins and Wanamaker 2022), consistent with the full income measures developed by Burkhauser et al. (2024) for subsequent years. From 1939–1963, poverty fell by 29 percentage points, with even larger declines for Black people and all children. While absolute poverty continued to fall following the War on Poverty’s declaration, the pace was no faster, even when evaluating the trends relative to a consistent initial poverty rate. Furthermore, the pre-1964 decline in poverty among working age adults and children was achieved almost completely through increases in market income, during which time only 2–3 percent of working age adults were dependent on the government for at least half of their income, compared to dependency rates of 7–15 percent from 1972–2023. In contrast to progress on absolute poverty, reductions in relative poverty were more modest from 1939–1963 and even less so since then.

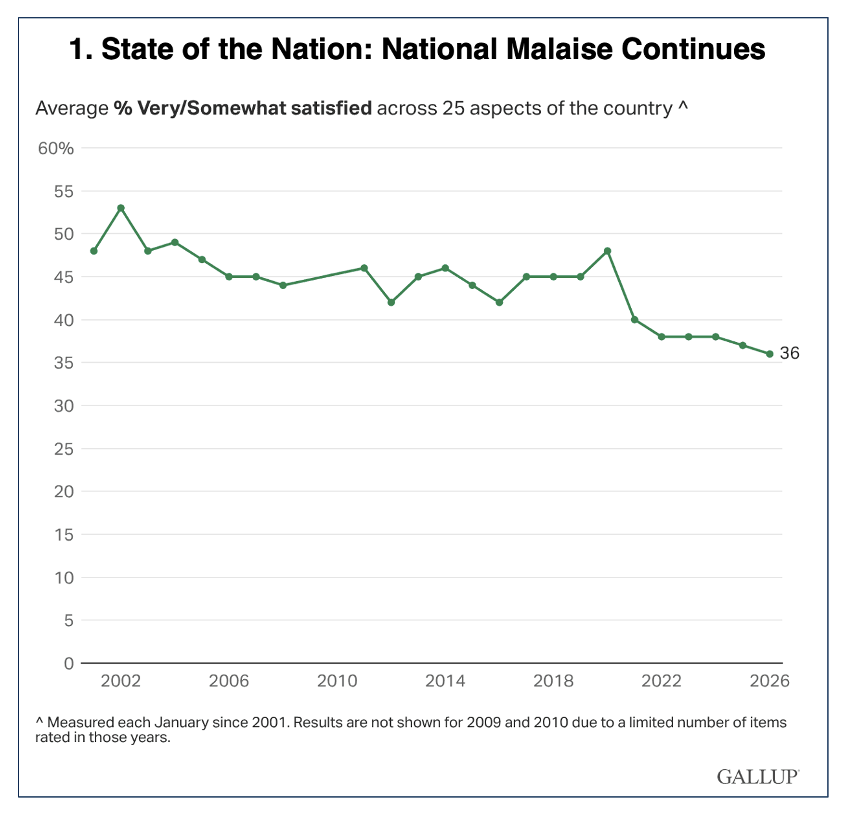

State of the Nation: National Malaise Continues Gallup

Each January, as part of its Mood of the Nation poll, Gallup asks Americans whether they are satisfied or dissatisfied with a battery of national conditions, offering a public "state of the union" measured ahead of the president's address to Congress. In January 2026, an average of 36% said they were very or somewhat satisfied across 25 aspects of the country, the numerically lowest reading in the poll's history dating back to 2001. The Trend: For two decades, average satisfaction with these national conditions stayed within a narrow band, fluctuating between 42% and 49%. It fell to 40% in January 2021 and has declined further since.

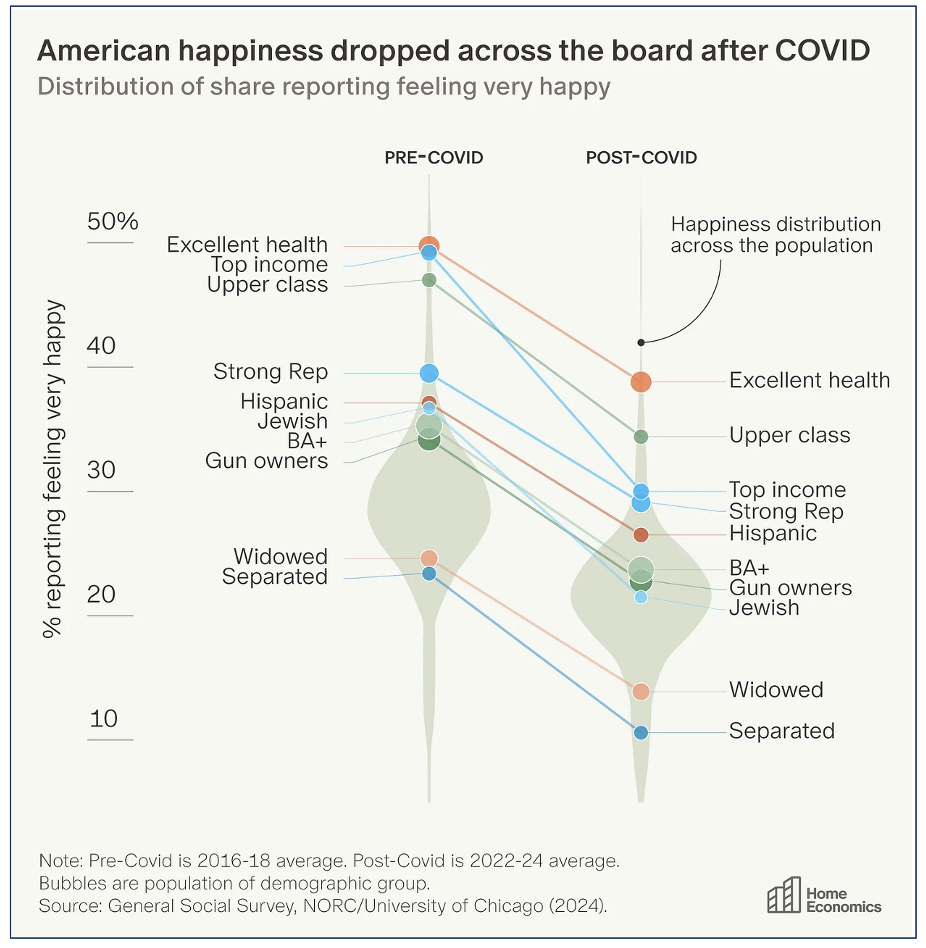

The Great Happiness Compression Home Economics

American happiness has fallen off a cliff. The General Social Survey has tracked this since 1972. Their data shows the share of Americans reporting they are "very happy" dropped from 29% before the pandemic to 22% in the most recent reading—the largest decline over any comparable span in the survey's 52-year history. The chart shows the shift in the "very happy" distribution across the population, along with the ten demographic groups that experienced the biggest happiness declines. The groups that lost the most happiness are the ones that had the most to begin with. The bottom barely budged. The groups that held up best share one trait: social connection. People who see friends often dropped just 4 points, compared to a 9-point drop among those who see friends rarely. Happiness for those who socialize with neighbors dropped less than for those who rarely do.

Recommended Weekend Reads

Germany’s China Shock, Trump’s Monroe Doctrine is Aimed at China, How The U.S. Population Has Shifted, Why China Doesn’t Want A U.S – Iran Deal, and How AI is Both Helping and Replacing Workers

February 27 - March 1, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them both interesting and useful. Have a great weekend.

The Americas

Trump's latter-day Monroe Doctrine is aimed at China Peterson Institute for International Economics

The US intervention in Venezuela, attacks on vessels in the Caribbean, financial squeeze on Cuba, and its bailout of Argentina should perhaps have come as no surprise. After all, the Trump administration has made no secret of its intentions, as laid out in the 2025 National Security Strategy (NSS) document: To "reassert and enforce the 'Monroe Doctrine' to preserve U.S. preeminence in the [Western] Hemisphere and deny outside powers control of strategic locations and assets." It would certainly appear that the administration is currently achieving the goals set out in the NSS, entrenching Latin America as the main stage for a geopolitical confrontation between the United States and China. But these actions could also introduce further turbulence into a region mired in political and economic problems. China is heavily invested in Latin America through various channels, notably its "green" Belt and Road Initiative. The framework has enabled China's public banks and state-owned enterprises to underwrite massive projects in renewable energy sources, critical minerals, and infrastructure. It is estimated that since 2010, China has invested around $35 billion in renewable energy projects alone. The figure does not include the $1.3 billion spent to finance the massive Port of Chancay in Peru, which connects South America's Pacific Coast to Shanghai.

Population drops and gains in every state FlowingData

The Census Bureau released population estimates for 2025. Most states gained population, but a few states saw more people move out than move in, with births not enough to compensate. By percentage, Puerto Rico, Hawaii, and West Virginia decreased in population the most since 2020. By total change, New York and California decreased by about 200,000 people each. The population in Louisiana, Illinois, and Mississippi also dropped. Idaho went the other direction with the largest increase over 10%. Texas and Florida populations increased the most, with total increases of 2.56 million and 1.92 million, respectively.

How Trump’s 15% Tariff Move Impacts Latin America Americas Quarterly

Latin American economies seem relatively well-positioned following the U.S. Supreme Court’s decision to invalidate last year’s tariffs on imports of goods and services and President Donald Trump’s announcement of a new 15% global tariff. Trump's previous levies were invalidated on February 20, after a majority of the U.S. Supreme Court’s justices (6-3) ruled that the president exceeded his authority to issue them, dealing the government a major setback. That day, Trump set a replacement global tariff of 10%, which was increased to 15% the next day.

Europe, China, and Iran

Germany’s China Shock Internationale Politik Quarterly

The China shock is here,” the German Economic Institute declared last July. Indeed, 2025 will go down as the year in which it could no longer be denied. Germany's trade deficit with China reached a record level of €87 billion—an increase of €20 billion compared to the previous year. And German exports to China continue to be in free fall. The United States, France, the Netherlands, Poland, and Italy have by now become more important export markets for Germany than China. At the beginning of this century, China accounted for 6 percent of global industrial production. Today, the figure stands at around 30 percent. China’s economic model is firmly geared toward global dominance in industries where Germany has been traditionally strong, such as automotive, mechanical engineering, and chemicals—as well as in future industries such as robotics and biotechnology. Beijing not only leverages the economies of scale of its vast domestic market but also makes forward-looking investments in research and development.

Why China Doesn’t Want the US and Iran to Make Peace The Diplomat

While Beijing publicly advocates restraint, sustained tensions between the U.S. and Iran serve its strategic interests. China's broader perspective on Iran is unlikely to change absent a major shock. Beijing views Tehran as a useful strategic partner in its long-term effort to counter Western – especially U.S. – dominance of the international system. As a result, China supports Iran diplomatically and economically, while also offering limited and discreet military-related assistance. This support does not typically take the form of overt arms sales, but rather the provision of dual-use components and technologies that can be used in Iranian drone and missile production. These activities allow Beijing to strengthen Iran’s resilience without incurring the costs associated with formal military alliances or large-scale weapons transfers.

What It Will Take to Change the Regime in Iran Behnam Ben taleblu/Foreign Affairs

The Islamic Republic of Iran is, quite possibly, at its weakest point since its founding in 1979. In June, Israeli and U.S. attacks destroyed its uranium enrichment capacity and many of its air defense systems. In December and January, the country experienced the most widespread domestic uprising since the birth of the Islamic Republic. Throughout, it has faced spiraling economic and environmental crises that it cannot fix. None of these events has knocked out the Islamic Republic. But there is no doubt it is down. It is easy to see why the Trump administration is prioritizing diplomacy and limited strikes. The Islamic Republic may be weak, but it is still lethal and capable of harming U.S. forces and civilian targets throughout its region. Such measures could inspire the masses of Iranians who took to the streets in December and January to do so again. Just this week, Iran witnessed smaller-scale campus protests, showing that animosity against the regime very much remains. If regular protests resume, American military power could level the playing field between the street and the state, giving the country’s demonstrators a chance to succeed.

Geoeconomics

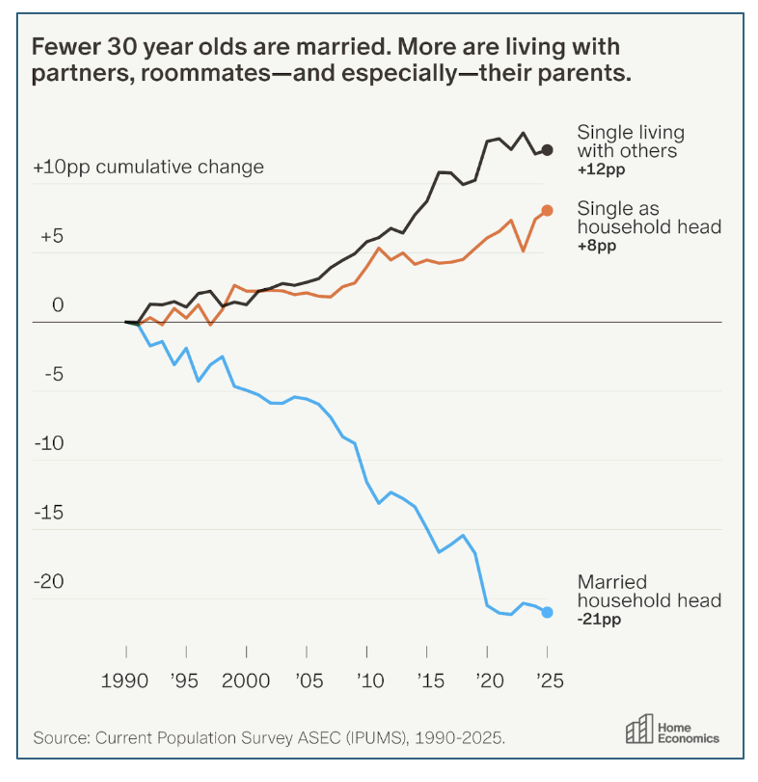

Living With Mom And Dad At 30 Aziz Sunderji Home Economics

The share of American 30-year-olds living with their parents or roommates nearly doubled btw 1990 and 2025, from 17% to 32%. Aziz Sunderji finds that this group is largely responsible for the age cohort’s 15pp decline in homeownership over that period.

The New Global Tariffs Are Also Unlawful Philip Zelikow/Hoover Institution’s Freedom Frequency

On February 20, the Supreme Court ruled that President Trump’s tariffs imposed under an emergency powers law were unlawful. After raging at the court, the president imposed a new set of global tariffs using a different statutory authority. Now, the Trump Administration has moved to use Section 122 to carry on the tariff policy. And the author – who was involved in the recently decided case – argues the use of 122 is both obsolete and illegal.

The 2028 Global Intelligence Crisis Citrini Research

In this widely-hailed essay, Alap Shah of Citrini Research models a scenario that the author writes about the potential impact of AI on society. Shah’s vision is that “In every way AI was exceeding expectations, and the market was AI. The only problem… the economy was not…. AI capabilities improved, companies needed fewer workers, white collar layoffs increased, displaced workers spent less, margin pressure pushed firms to invest more in AI, AI capabilities improved… It was a negative feedback loop with no natural brake. The human intelligence displacement spiral. White-collar workers saw their earnings power (and, rationally, their spending) structurally impaired. Their incomes were the bedrock of the $13 trillion mortgage market - forcing underwriters to reassess whether prime mortgages are still money good.”

Speed Can Reindustrialize America Austin Vernon Blog

High US wages for skilled workers constrain robot adoption in manufacturing. “Many less productive US manufacturing firms could buy a robot, but couldn’t attract the talent to program it.” The US can’t “emulate” the low-wage, high-skilled China model.

AI Is Simultaneously Aiding and Replacing Workers, Wage Data Suggest J. Scott Davis Federal Reserve Bank of Dallas

For occupations with a very low experience premium, AI exposure lowered wage growth, likely due to substitution of AI for costly experienced workers. At the top of the experience distribution, AI raised wage growth, as it complements experienced workers.

The Flawed Paper Behind Trump’s $100,000 H-1B Fee Economic Innovation Group

Abstract: Do H-1B visa holders earn more or less than Americans? There are two different ways to answer this. If we compare H-1B holders to the average native-born worker, the answer is unequivocal that the visa holder is paid more. Median H-1B pay in 2024 was $120,000 per USCIS, compared to $67,000 for the average native-born worker. However, when we compare H-1B holders to otherwise similar native-born workers, the question becomes more complex. Answering it correctly requires careful examination. Unfortunately, a recent attempt at answering this question from Harvard economist George Borjas contains major errors.

Recommended Weekend Reads

Trump’s IEEPA Tariffs Are Dead. Now What?, Iran: What Happens Next if the US Launches Attacks, How A BRICS Currency Could Happen, and the Looming Fiscal Crisis in the Western World

February 20 - 22, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them of interest and useful as well. Have a great weekend.

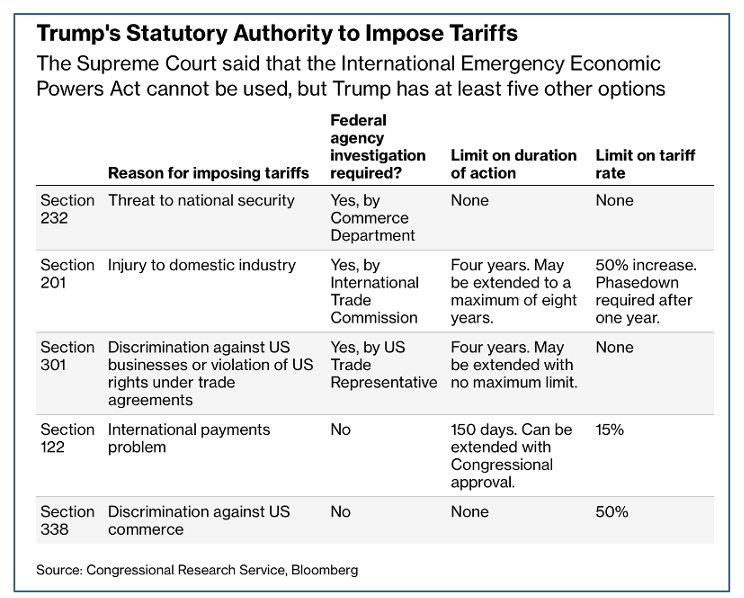

U.S. Trade Policy After the IEEPA Decision

Trump’s Options After the Supreme Court Said His Tariffs Are Illegal Bloomberg

On Friday, the U.S. Supreme Court President Trump had illegally used of the International Emergency Economic Powers Act (IEEPA) for his April 2025 “Liberation Day” calls into question what Trump will do next. Trump has at least five tools he can use to offset the IEEPA tariffs; however, none of them offer the latitude that Trump’s interpretation of IEEPA allowed. Section 338 of Smoot-Hawley, which has never been used, likely has the broadest scope.

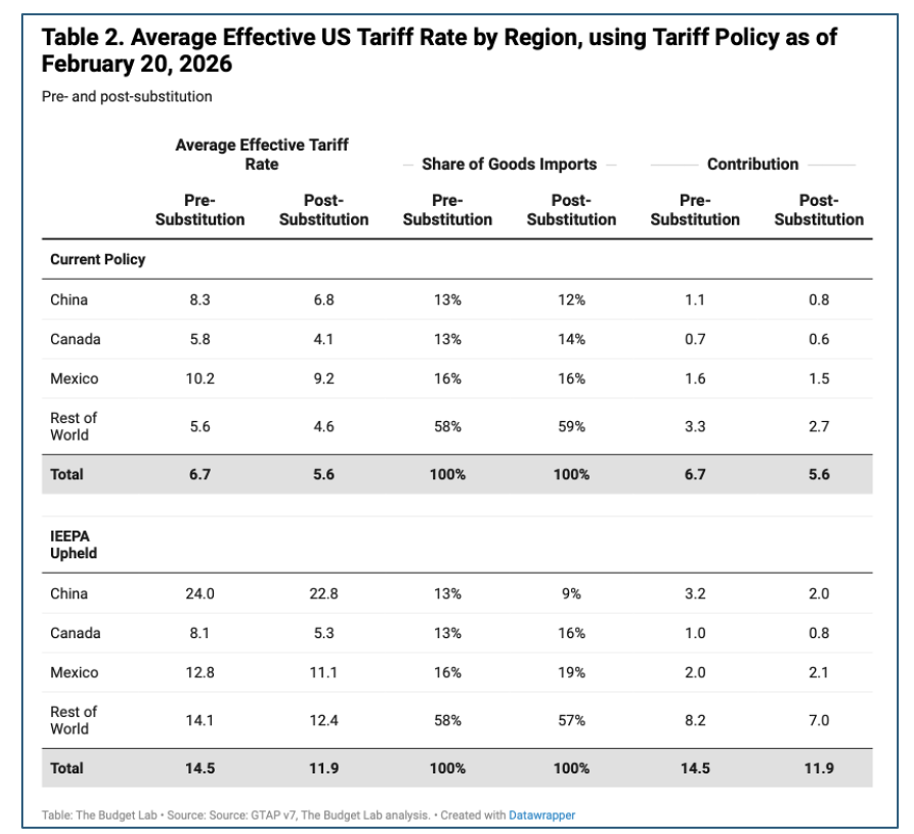

State of U.S. Tariffs: February 20, 2026 Yale University Budget Lab

The Budget Lab estimates the effects of all US tariffs and foreign retaliation implemented in 2025 after the decision by the Supreme Court of the United States that President Trump exceeded his authority to invoke the 1977 International Emergency Economic Powers Act (IEEPA) to impose reciprocal tariffs. Without IEEPA tariffs, consumers will face an overall average effective tariff rate of 9.1%, which remains the highest since 1946 excluding 2025. (If IEEPA tariffs had been allowed to stay in effect, this figure would have been 16.9%.) All tariffs to date as of February 2026 are projected to raise about $1.2 trillion over 2026-35, though slower economic growth reduces revenues and brings the net dynamic revenue to $1 trillion. (With IEEPA, these figures would be more than twice as large.) The economic implications of the SCOTUS decision are complicated by two major factors. First, in the short-term, firms will be aggressively seeking refunds on tariffs paid in 2025, which has large revenue effects and uncertain distributional effects. Second, the current Administration has stated its intent to replace IEEPA tariffs with tariffs using other authorities, but there remain timing and other questions regarding these steps.

Implications of Growing U.S. – Iran Military Tensions

The Day After Khamenei: Iran’s ‘Liberation’ Will Begin as an IRGC Power Struggle Charbel Antoun/National Interest

Many imagine the day after Ali Khamenei as a moment of sudden liberation: Iranians shaking off the mullahs and deciding their own destiny. The likelier opening act is far less romantic. The immediate aftermath will probably look less like a velvet revolution and more like the opening round of an insider power struggle—staged and refereed by the Islamic Revolutionary Guard Corps (IRGC) and its allies. The institutions that have grown strongest under Khamenei are not parliaments, parties, or independent courts, but the security state and its sprawling economic empire. Those are the actors best positioned to inherit the republic he leaves behind.

Iran’s regime is suffering from strategic vertigo. Its next misstep may be its last The Atlantic Council

Tehran appears to be suffering from a case of strategic vertigo. As Iranian leaders continue to see their major decisions backfire over the course of two and a half years, a disorienting dizzy spell may be the best way to describe the state of Iranian foreign policy. Negotiations between the United States and Iran are ongoing, with US President Donald Trump Thursday that he expects a resolution within ten to fifteen days, as he also undertakes a massive military buildup for a possible conflict. The talks provide the regime with a rare opportunity—a gift, even—to escape from yet another predicament. The question right now is whether leaders in Tehran grasp the magnitude of the moment and refrain from their old habits of obstinacy, or whether they will add another strategic error to their string of missteps—one that could be their last. With the United States preparing for strikes if negotiations fail, the question arises of how Iran reached the precipice in the first place.

What War With Iran Would Look Like Arash Reisinezhad/Foreign Policy Magazine

Washington and Tehran may be closer to military confrontation than at any point in memory, but they are not on the brink of war in any conventional sense. The most plausible outcome of the current standoff is not a U.S. invasion of Iran or a full-scale regional war. It is a limited, carefully calibrated strike designed to reshape bargaining dynamics rather than end them.

Iran: What Challenges face the country in 2026? House of Commons Library

In 2025, the US and Israel struck Iran’s nuclear program, the UN reimposed sanctions against the country and its economy continued to struggle. Iran’s regional position also worsened. Established leaders of many Iran-backed armed and proscribed terrorist groups have been eliminated, and their strength weakened in the regional conflict that has been ongoing since 2023. Some Iran-backed groups are facing renewed local and international calls to disarm. This briefing for UK Members of Parliament surveys the situation in Iran, including the challenges facing its government; the status of Iran’s nuclear program and the potential for further strikes in 2026; and pressures on Iran-backed groups in the region.

Iran Oil And Gas Market Size & Share Analysis - Growth Trends and Forecast (2026 - 2031) Mordor Intelligence

According to Mordor’s recent research, Iran’s oil and gas market size in 2026 is estimated at USD 39.18 billion, growing from 2025 value of USD 37.10 billion with 2031 projections showing USD 51.51 billion, growing at 5.62% CAGR over 2026-2031. Robust reserve availability, state-backed capital deployment, and resilient export flows underpin this trajectory even as sanctions pressure persists. The upstream sector anchors revenue, as Iran is the fourth-largest crude producer in OPEC. Meanwhile, the downstream segment is growing faster, with domestic firms adding fluid catalytic cracking and condensate-splitting capacity to increase product yields. Onshore production remains the backbone of the Iranian oil and gas market, but offshore investments at South Pars are accelerating to protect reservoir pressure and sustain natural-gas output. Asset deployment overwhelmingly favors development projects, yet exploration spending is rising because reserve replacement has become a policy imperative. High market concentration persists: The National Iranian Oil Company (NIOC) and its subsidiaries continue to dictate most decisions, although private and quasi-state contractors now win multi-billion-dollar tenders that were once the domain of foreign major oil companies.

Geoeconomics and Global Markets

Could a BRICS Currency Work? Jim O’Neill/ Project Syndicate

O’Neill – who coined the acronym “BRICS” – argues Economists have long dismissed the idea that a BRICS common currency could challenge the US dollar's role in the global economy, and for good reason. But that doesn't mean there couldn't be new common rails for settling trade between countries that want to escape the long arm of the US government.

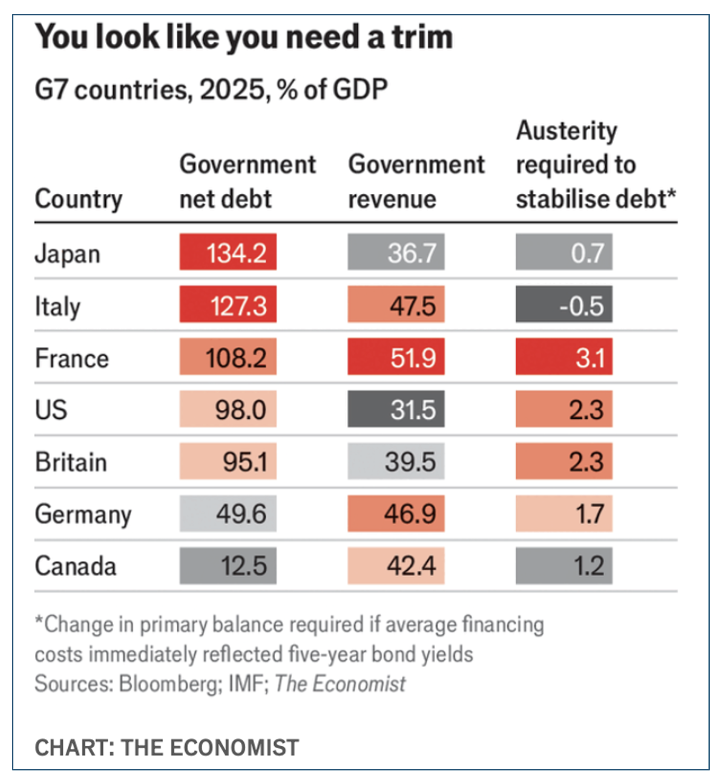

Across The Rich World, Fiscal Crises Loom The Economist

The Economist calculates that most rich countries could still run small primary deficits [deficits net of interest payments] and keep debts stable as a share of their economies, even if they had to refinance all their debt immediately at today’s rates. The largest primary surplus required to balance debts is in Britain, at just 0.3% of GDP. That is not large for countries in a pinch. In the late 1990s Italy ran primary surpluses of 3-6% of GDP to bring down debts before joining the euro. In Britain and America, deficits are large. The belt tightening needed to stabilize the debt-to-GDP ratio exceeds 2% of GDP; in France it is greater than 3% of GDP. Things look worse still when you consider the coming wave of spending on ageing populations, defense and the climate transition. And higher debt interest costs to come are not yet fully accounted for.

Are Government Bonds Safe in Times of War and Pandemic? Zhengyang Jiang, Hanno Lustig, Stijn Van Nieuwerburgh and Mindy Xiaolan National Bureau of Economic Research

Abstract: We analyze real returns on U.S. and U.K. government debt during major wars and the COVID-19 pandemic over the past three centuries. Wars are associated with sharply negative real returns on outstanding government debt, with returns falling far below economic growth, in contrast to peacetime periods when returns exceed growth. Elevated surprise inflation and financial repression account for a cumulative 31% wedge between returns and growth over four years of war, implying that bondholders bear a substantial share of wartime fiscal costs. During wartime, government bonds also systematically underperform risky assets.

When Houses Outrun Paychecks: The Lost Decades of Housing Affordability Federal Reserve Bank of St. Louis ON the Economy Blog

Abstract: In this blog post, we analyze how housing affordability has evolved over the past 20 years. For most U.S. counties, the story is remarkably similar: Home values have risen much faster than the incomes of the people living in them. From 2000 to 2024, median per-capita income has grown steadily but modestly, at around 155% in nominal terms. Over the same period, median home prices—when measured carefully and adjusted for local composition—have increased at a much faster pace, at around 207% in nominal terms. This divergence helps explain why younger households struggle to buy their first home, while longtime owners increasingly view housing as their primary source of wealth.

Recommended Weekend Reads

What Does Russia’s Inability to Support Its Allies Mean for Its Own Future?, The Massive Industrial Challenge To Modernize the U.S. Navy, Was Pandemic Fiscal Relief Effective Stimulus? And An Assessment of China’s Military Buildup

January 16 - 18, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them interesting and useful as well. Have a great weekend.

The Future of Russia

Putin’s great-power project faces the ‘end of an era’ Politico EU

Moscow was also seemingly unable to protect its closest friend in South America earlier this month when the United States captured Venezuela’s Nicolás Maduro, a leader who had dutifully made the trip to Moscow for Putin’s Victory Day Parade in May last year. Embarrassingly, Moscow wasn’t even able to fend off the unprecedented U.S. seizure of an oil tanker flying a Russian flag. Just a year ago, Putin signed a 20-year strategic partnership agreement with Tehran. Now the regime — which supplied Russia with killer Shahed drones for its fight in Ukraine — is in danger of being toppled by protesters whom Trump has indicated he could intervene militarily to defend. Russians have taken notice. “An entire era is coming to an end,” wrote a pro-war military blogger under the pen name Maxim Kalashnikov on Sunday, reflecting growing criticism of the Russian leadership.

Russia Is the World’s Worst Patron Foreign Affairs

For the last 20 years, Moscow has demonstrated an ability to inject itself as a player in regions with strong anti-American sentiment. But the Kremlin’s costly adventures have yet to show any practical benefits for enhancing Russia’s genuine security interests or boosting its economic prosperity. Involvement in places such as Venezuela serves only Putin’s vanity, a few votes of solidarity with Moscow at the UN General Assembly, and money-making opportunities for corrupt Russian officials. The result has been that from Syria to Venezuela to Iran, Putin has overpromised and underdelivered.

Why Didn’t the Ukraine War Turn Russia’s Ruling Class Against Putin? Carnegie Politka

The answer is that Russia’s ruling class is disillusioned and fragmented. And, as the writer points out, the apparent suicide of the dismissed transport minister Roman Starovoit in 2025 was a reminder of the fragility of everyone’s position. For another, the idea that had brought together much of the establishment, “autocratic modernization”—that despite the authoritarian system, a rational state, capable of learning lessons and balancing interests, could still emerge in Russia—has obviously turned out to be a failure.

The Massive Challenge to Modernizing the U.S. Navy

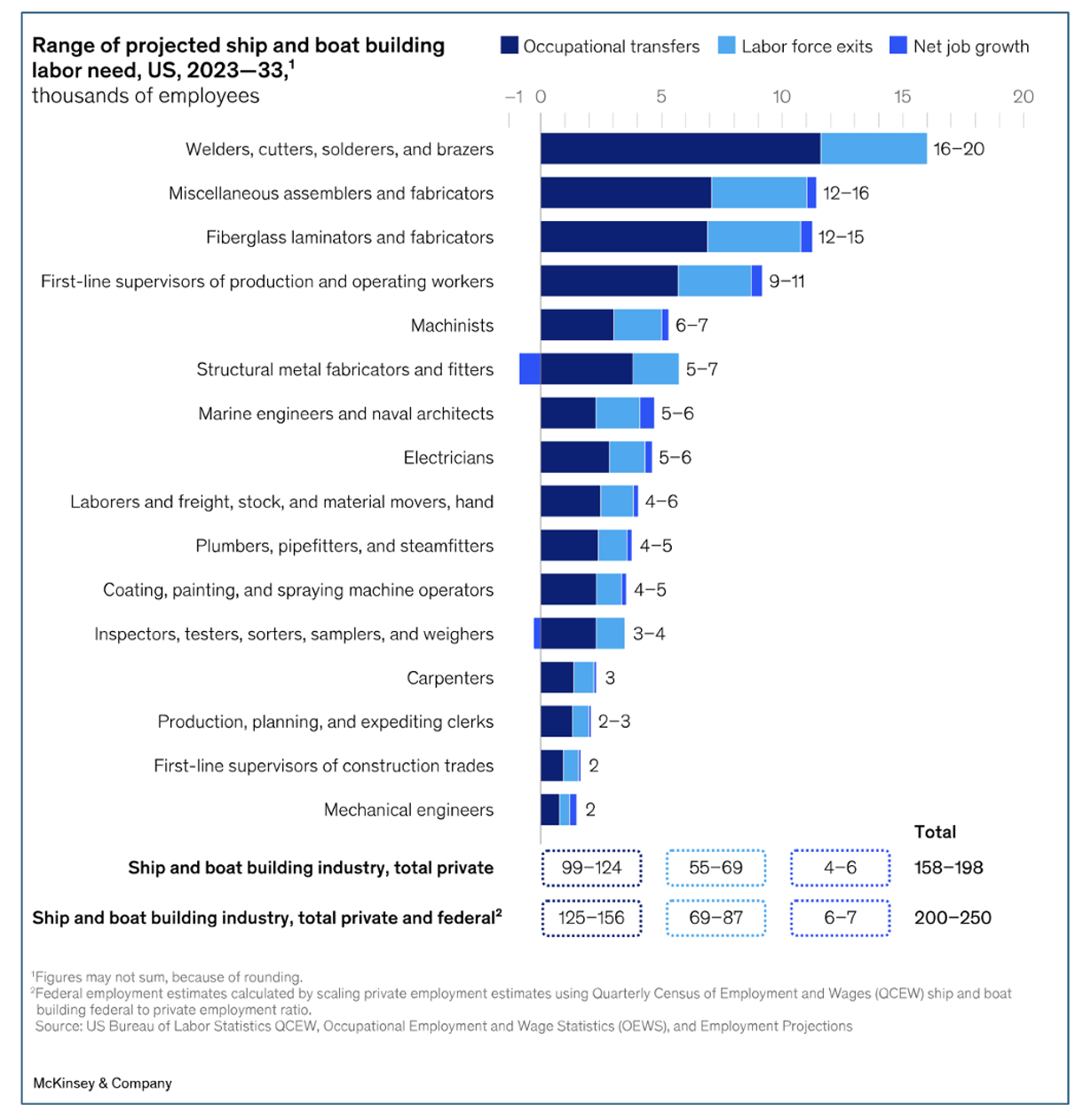

Helming A Sea Change: Building The Future Workforce For US Shipbuilding McKinsey & Company

According to the US Department of Labor, the shipbuilding industry may require about 200,000 to 250,000 additional maritime workers in critical occupations, such as welding, soldering, and front-line management, to satisfy demand over the next decade. If demand for ships increases, the labor gap will be even wider.

Outlining the Challenges to the U.S. Naval Shipbuilding Center for Strategic and International Studies

Growing the size of the Navy has been a bipartisan goal of successive administrations and Congress over the last decade. The service faces capacity limitations as it struggles to meet the demands of its current aggressive operational tempo with a fleet that is small by historical standards and faces delays in conducting maintenance. The demand to increase the Navy’s ship count has only grown as China’s navy has overtaken the U.S. fleet in terms of size, with the blistering rate of production of its own shipbuilding industry. Despite the Navy’s plans for growing the fleet and bipartisan efforts and funding from Congress, the U.S. shipbuilding enterprise—including the Navy, Department of Defense (DoD), Congress, and industry—has failed to consistently produce ships at the scale, speed, and cost demanded. These longstanding challenges stem from a series of interwoven, systemic issues within both the U.S. government and industry, as well as broader socioeconomic trends. This report outlines the challenges facing the U.S. naval shipbuilding enterprise, their underlying drivers, and some efforts the government has taken to mitigate them.

Geoeconomics and Technology

Was Pandemic Fiscal Relief an Effective Fiscal Stimulus? Evidence from Aid to State and Local Governments Journal of Macroeconomics

Abstract: We use an instrumental-variables estimator reliant on variation in congressional representation to analyze the macroeconomic effects of federal aid to state and local governments during the COVID-19 pandemic. Through December 2022, we estimate statistically insignificant impacts of federal aid on employment. Our baseline point estimate suggests that $603,000 were allocated for each state or local government job-year preserved, and the bounds on our baseline confidence interval rule out estimates smaller than $220,400. Our estimates of effects on aggregate income and output are centered on zero and imply modest, if any, spillover effects onto the broader economy.

When Trade Compresses: The Impact of Liberalization on Wage Inequality Federal Reserve Bank of Cleveland

Abstract: We study the effects of trade liberalization on the full wage distribution, exploiting Spain's 1993 entry into the European Single Market. Using employer-employee data, we identify the causal effects of trade across the entire wage distribution, using a novel shift-share instrument embedded in an unconditional quantile regression. We find that the liberalization reduced wage inequality, leading to wage compression through earnings gains at the bottom of the distribution and wage losses at the top. We trace this compression to two asymmetric channels: import competition disproportionately harmed high earners, while export opportunities benefited low earners. The key mechanism is an import-driven “skill-downgrading.” A multi-region multi-sector model shows that the key insight for understanding these empirical results is that trade's distributional effects depend on the skill intensity of a country's tradable sector, and Spain's was relatively low-skill-intensive back then.

Foreign Affairs: The Myth of the AI Race Colin Kahl/ Foreign Affairs

In July, the Trump administration released an artificial intelligence action plan titled “Winning the AI Race,” which framed global competition over AI in stark terms: whichever country achieves dominance in the technology will reap overwhelming economic, military, and geopolitical advantages. As it did during the Cold War with the space race or the nuclear buildup, the U.S. government is now treating AI as a contest with a single finish line and a single victor. But that premise is misleading. The United States and China, the world’s two AI superpowers, are not converging on the same path to AI leadership, nor are they competing across a single dimension. Instead, the AI competition is fragmenting across many domains, including the development of the most advanced large language and multimodal models; control over computing infrastructure such as data centers and top-of-the-line chips used to train and run models; influence over which technologies and standards are used throughout the world; and integration of AI into physical systems such as robots, factories, vehicles, and military platforms. Having an edge in one area does not automatically translate into an advantage in the others. As a result, it is plausible that Washington and Beijing could each emerge as leaders in different parts of the AI ecosystem rather than one side decisively outpacing the other across the board.

China’s Military Capability

Annual Report to Congress: Military and Security Developments Involving the People’s Republic of China 2025 U.S. Department of Defense

Abstract: China’s historic military buildup has made the U.S. homeland increasingly vulnerable. China maintains a large and growing arsenal of nuclear, maritime, conventional long-range strike, cyber, and space capabilities able to directly threaten Americans’ security. In 2024, Chinese cyberespionage campaigns such as Volt Typhoon burrowed into U.S. critical infrastructure, demonstrating capabilities that could disrupt the U.S. military in a conflict and harm American interests. The PLA continues to make steady progress toward its 2027 goals, whereby the PLA must be able to achieve “strategic decisive victory” over Taiwan, “strategic counterbalance” against the United States in the nuclear and other strategic domains, and “strategic deterrence and control” against other regional countries. In other words, China expects to be able to fight and win a war on Taiwan by the end of 2027.

The World Economic Forum’s Global Risk Assessment

Global Risks Reports 2026 World Economic Forum

In advance of the World Economic Forum (WEF) meetings in Davos ,Switzerland this coming week, the WEF released their 21st edition Global Risks Report 2026. The report analyses global risks through three timeframes to support decision-makers in balancing current crises and longer-term priorities. Chapter 1 presents the findings of this year’s Global Risks Perception Survey (GRPS), which captures insights from over 1,300 experts worldwide. It explores risks in the current or immediate term (in 2026), the short-to-medium term (to 2028) and in the long term (to 2036). Chapter 2 explores the range of implications of these risks and their interconnections, through six in-depth analyses of selected themes. Below are the key findings of the report, in which we compare the risk outlooks across the three-time horizons.

Recommended Weekend Reads

Is Trade Uncertainty Boosting Automation? Putin’s Fear of Economic Humiliation, American Soybean Farmers Feeling the Pain of China’s Boycott, And How Geopolitical Risk Impacts Consumer Spending

September 5 - 7, 2025

Each week, we gather up the best research and reports we have read in the past week and pass them on to you. Below is this week’s curated collection. We hope you find them interesting and informative, and that you have a great weekend.

Geoeconomics & Trade

Will Trade Uncertainty Boost Automation? Federal Reserve Bank of San Francisco

Recent surges in trade policy uncertainty highlight the fragility of global supply chains, prompting businesses to consider reshoring—moving production from abroad to domestic locations. Reshoring can be costly, creating incentives for businesses to automate. Evidence suggests that businesses facing heightened trade policy uncertainty in industries more exposed to international trade reshore more and automate more than those that are less exposed to trade. Automation appears to help mitigate the otherwise negative effects of trade policy uncertainty on production and labor productivity.

In Tariff Standoff with Trump, China Boycotts American Soybeans New York Times

China has rare earth metals. The United States and Brazil have soybeans. For all the chokeholds China maintains on global supply chains, it is overwhelmingly dependent on soybeans from other parts of the world. China imports three-fifths of all the soybeans traded on international markets. Now with China and the United States locked in a tense standoff over tariffs, soybeans have emerged as a central dispute between the trading partners. China has been boycotting purchases of U.S. soybeans since late May to show displeasure with President Trump’s imposition of tariffs on imports from China. The pain is being felt in Midwest states, especially Illinois, Iowa, Minnesota and Indiana. For the first time in many years, American farmers are preparing to harvest their crop this fall with no purchase orders from China.

Effects of Tariff Uncertainty on the Outlook of Small and Medium-sized Businesses Federal Reserve Bank of Boston

A large body of research demonstrates that uncertainty affects many dimensions of firms’ decisions, from investment and hiring to pricing and profitability. To gain a better understanding of how uncertainty induced by shifting trade policy shapes the behavior of small and medium-sized businesses (SMBs) the authors surveyed decision-makers at SMBs. Key Takeaways include:

Results from the survey indicate that uncertainty about tariffs rose markedly from the first wave to the third for all SMBs, and especially for importers.

Survey respondents with greater uncertainty about tariffs in April 2025 – and especially those that import – tended to report greater uncertainty about business operations, particularly about investment and worker head count.

The respondents indicated that a hypothetical reduction in business uncertainty would improve their expectations, but another increase in business uncertainty would not lead to further deterioration in their outlook.

The muted reaction to a hypothetical increase in business uncertainty suggests that by April 2025, the effect of increased uncertainty on SMBs’ expectations may have already peaked and/or that financial conditions had not tightened enough to notably amplify any negative real effects of further increases in uncertainty.

The Fiscal Impact of Immigration: An Update AEI Economic Perspectives

Immigrants have an overall positive fiscal impact on the US—an effect driven by high-skilled

immigrants. Low-skilled immigrants, like their US-born counterparts, impose a net fiscal cost.

However, recent studies show that the indirect fiscal effects of low-skilled immigration are positive,

partly offsetting the negative direct fiscal impact. Moreover, immigrants will help bear the cost

of future policy changes required to address the growing national debt. Smaller immigration

inflows might reduce fiscal pressure on state and local governments, but would increase fiscal

pressure on the federal government and slow economic growth.

The Impact of Geopolitical Risk on Consumer Expectations and Spending Yuriy Gorodnichenko, Dimitris Georgarakos, Geoff Kenny, and Olivier Coibion / NBER

Abstract: Using novel scenario-based survey questions that randomize the expected duration of the Russian invasion of Ukraine and Middle East conflict, we examine the causal impact of geopolitical risk on consumers’ beliefs about aggregate economic conditions and their own financial outlook. Expecting a longer conflict leads European households to anticipate a worsening of the aggregate economy, with higher inflation, lower economic growth, and lower stock prices. They also perceive negative fiscal implications, anticipating higher government debt and higher taxes. Ultimately, households view the geopolitical conflict as making them worse off financially and it leads them to reduce their consumption.

Russia’s Struggling Economy

Can Russia Weather a Fuel Crisis Caused by Ukrainian Drone Attacks? Carnegie Politika

Once again, Russia is in the grips of a gasoline crisis. Prices at the pump are rising, and some gas stations have run dry. This isn’t the first time Russia has experienced such shortages, but this time around they could be more serious because of the ongoing war in Ukraine. There were gasoline crises in Russia both before the full-scale invasion (in 2011,2018, and 2021), and afterward (in 2023). Despite a 2024 Ukrainian drone campaign targeting Russian refineries, the fuel market remained relatively calm. Back then, each refinery was only hit by a single drone, reducing plant capacity but leaving it operational. The damage was dealt with in a matter of weeks, consecutive attacks, were rare and often deflected, and neighboring plants continued to operate without interruption. Ultimately, the 2024 drone attacks caused inconvenience and expense for the Russian oil industry, but did not present a major problem. This time could be quite different.

Putin’s Fear of a Humiliating Economic Crisis Foreign Policy

Russian President Vladimir Putin has every reason to seek a lifeline for the Russian economy. In recent weeks, a flurry of signs has shown Russia’s war-drained, sanctions-constrained economy to be at an inflection point. For the first time since the start of the war, nonmilitary economic activity has been contracting, bankers are making plans to weather a financial crisis, and energy firms are worrying about losing their largest customer for seaborne oil exports. Putin’s intensifying economic troubles have important implications for Western policymakers as they begin negotiating with Moscow about the future of Ukraine. Unlike the impression the Russian leader tries to make, time is far from being on his side. In fact, economic pressure remains the best leverage that Ukraine’s supporters have over the Kremlin. It remains to be seen whether Europe and the United States will choose to play the economic ace they still have up their sleeves.

The Global Race for Critical Minerals

Why Is Renewing AGOA Strategic for U.S.-Africa Minerals Diplomacy? Center for Strategic and International Studies

The African Growth and Opportunity Act (AGOA), first signed into law by President Bill Clinton in 2000, is a unilateral U.S. trade preference program set to expire in September 2025. Its pending reauthorization has sparked debate over whether—and how—it should be extended and reformed. A failure to extend AGOA could have larger ramifications at a time when the United States is doubling down on its commercial diplomacy—and more specifically, its mineral diplomacy efforts—with Africa.

Europe’s Strategic Access to Battery Minerals in a Changing Geoeconomic Landscape The Hague Centre for Strategic Studies

Europe’s transition to a low-carbon economy hinges on the rapid deployment of battery technologies. Batteries are essential for stabilizing electricity grids powered by renewables and for enabling the shift from internal combustion engine (ICE) cars to electric vehicles (EV), especially after the European Union’s (EU) 2035 ban on new ICE cars. The successful deployment of batteries in Europe depends on secure supply chains, which are heavily concentrated. China plays a dominant role across the entire battery supply chain. It produces most of the world’s batteries and controls large shares of battery material mining and processing capacity, including graphite, lithium, manganese and phosphate. The Chinese government can use its control over battery supply chains to exert geopolitical pressure on other countries. To reduce its vulnerability, Europe could choose to look into types of batteries that rely less on raw materials whose supply chain is dominated by China.

Recommended Weekend Reads

Latin America Can De-Risk Semiconductor Supply Chains, Why Russian-Indian Relations Have Remained Steady, and Why Tariffs Led to More Demand for Stablecoins Went Up and Less for the Dollar

August 29 - 31, 2025

Here are our recommended reads from reports and articles we read in the last week. We hope you find these useful and that you have a relaxing weekend. And let us know if you or someone you know wants to be added to our distribution list.

Americas

Latin America’s Role in De-Risking Semiconductor Supply Chains Center for Strategic & International Studies

While the semiconductor supply chain currently spans several continents, China has made efforts to develop a self-sufficient semiconductor manufacturing ecosystem through industrial policies such as “Made in China 2025,” which presents a direct strategic and economic challenge to the United States. De-risking the semiconductor supply chain, particularly that of “legacy chips,” is of paramount importance, particularly at a time in which the Trump administration considers imposing additional sectoral tariffs on semiconductors. Latin America sits at the juncture of possibility and opportunity at a critical time for the expansion of semiconductor manufacturing, providing some of the key elements and capabilities that allow for semiconductor assembly, testing, and packaging as well as final integration into electronics. For companies relying on semiconductor manufacturing, diversifying production sources is key to reducing the risks associated with supply chain disruptions and great power competition.

Latin America’s Opportunity in the AI Race Americas Quarterly

In recent weeks, two starkly different visions of the future of the digital world emerged from the globe’s AI superpowers. These competing philosophies have put Latin America in an uncomfortable position between them. The region now faces a digital dependency trap that could determine its technological fate for decades. Last month, the Trump administration released “Winning the Race: America’s AI Action Plan,” a comprehensive national AI strategy that frames artificial intelligence as a zero-sum competition where the U.S. must achieve “unquestioned and unchallenged global technological dominance. China then unveiled its “Action Plan on Global Governance of Artificial Intelligence.” For Latin American policymakers, these manifestos present what appears to be a binary choice. Choosing wrong could mean decades of technological dependency, limited sovereignty, and diminished prospects for indigenous innovation. The tension between the two paths, however, could offer the region an opportunity for growth.

On the Ground With a Top Mexican Cartel New York Times

For the last year, Paulina Villegas, an investigative journalist for The New York Times, had the daunting task of meeting repeatedly with members of the Sinaloa Cartel. The assignment had obvious risks: The Sinaloa Cartel is a U.S.-designated terrorist group. But the meetings, Ms. Villegas said, were vital to her quest to provide readers a clearer understanding of how powerful criminal groups operate, documenting the practices and root causes that both the Mexican and American governments are trying to address.

The Indo-Pacific

Why Russian-India Relations Have Been Steady in the Storm War on the Rocks

Russia has more friends than Western analysts like to admit, even three years into the Russo-Ukrainian War. While many have paid close attention to Russia’s beneficial partnership with Iran, the introduction of North Korea’s legions into the Ukrainian battlespace, or persistent materiel support from China, Russia’s other rising-power relationship is often underdiscussed — that of India. The Russian-Indian relationship is both of longer duration and deeper history than those Russia has with its other key partners. It is also sometimes ignored as it does not extend to shared adversarial relations with the greater West. This is a mistake, as India is one of Russia’s self-identified civilizational friends. Furthermore, despite various ups and downs, the partnership has proven quite resistant to third-party pressures, including recently from the anti-Russian Western coalition.

What’s New About Involution? Carnegie China

In recent months “neijuan” (内卷), or “involution,” has become one of the most important buzzwords in Chinese policymaking circles. It has come to describe a disruptive process of relentless competition and price cutting among Chinese businesses, and has been increasingly criticized by policymakers, from President Xi Jinping down, for leading to a zero-sum race to the bottom, marked by vicious price wars, large-scale losses, homogenous products, and improper business practices. An August 2 article in Caixin explains: China’s top economic planner vowed on Friday to intensify its crackdown on “involution,” pledging to curb disorderly corporate competition, rein in wasteful investment and standardize local governments’ business attraction practices to protect fair market order. The article is referring to the July 30 Politburo meeting that set out Beijing’s priorities for the second half of 2025. Of the three main priorities, two—the need to boost domestic consumption and the promise to support the real estate market—have been proposed regularly in the past three to four years. Much of the focus, however, was on the newest priority, which is to battle deflationary pressures by reducing “disorderly” price competition and overcapacity in manufacturing—measures, in other words, aimed at reining in involution.

Xi Unleashes China’s Biggest Purge of Military Leaders Since Mao Bloomberg

China’s leader has ousted almost a fifth of the generals whom he personally appointed while running the country, something his predecessors never did, according to a Bloomberg News analysis of TV footage, parliamentary gazettes, and other public records. Moreover, Xi’s purge has left the CMC with only four total members, down from seven when his third term started. That’s the fewest in the post-Mao era, the Bloomberg analysis shows. As more and more of China’s top military leaders fall, it leaves those trying to understand the nation grappling with a near-impossible question, given the opaque nature of the Communist Party: Is this all a sign of Xi’s political strength, or of his weakness? The implications reach around the world and across the global economy.

Geoeconomics